Current assets (cash, AR, inventory) are assets that can be converted to cash within one year. Conversely, current liabilities (AP, short-term debt) are liabilities that will be settled with cash within one year.

Current assets and liabilities, like most other aspects of business, are within management’s control. As a rule-of-thumb, a small business should have enough in current assets to cover current liabilities. However, it’s very possible that more current assets might be needed. Resources exist to help small business owners manage current assets and liabilities efficiently.

What are the current assets and current liabilities?

As you probably noticed, current assets and current liabilities share a common prefix – the word “current.“ Current, in this context, means that it will be converted to cash (assets) or paid with cash (liabilities) within one year.

Contrast this with long-term assets and liabilities. These assets and liabilities affect cash balances over a horizon that’s greater than one year.

On a properly formatted balance sheet, you’ll see that current assets are grouped together. As are current liabilities. They should also be listed in descending order in terms of their liquidity (assets) and maturity (liabilities).

Looking for more spreadsheet templates?

Examples of current assets and liabilities

Current assets include the following:

- Cash (and equivalents) – This one is pretty self-explanatory. We all know what cash is. Cash equivalents are assets with such high liquidity and short maturity that they might as well be considered cash.

- Short term investments – This can include marketable securities (stocks and other investments). CDs, savings accounts, and other investments that will mature within a year.

- Inventory – This is the value of the materials used to create products. It can include raw materials, work in process (WIP), or finished goods. The value of inventory depends upon the companies cost accounting methodology.

- Accounts receivable (AR) – This is the cash owed by the company’s customers. If amounts are not expected to be paid, then they should be taken out of this balance.

Current liabilities include the following:

- Accounts payable (AP) – This is cash owed to suppliers. Ideally, accounts receivable would be collected first, before accounts payable are paid.

- Short term debt – This is money that was borrowed with the intent of being repaid within a year.

- Current portion of long-term debt – Yes, long-term debt is a long-term liability, of course. But, a certain portion of the long-term debt will have to be paid with cash over the coming year. This makes it short-term.

- Income taxes – Normally, income taxes are due every year. This short-term liability represents the expected amount owed, in cash.

Of course, there are other, less common, current assets and liabilities that you’ll come across. Just remember the rule-of-thumb – if it’s an asset that can be converted to cash within a year, it is a current asset. If it is a liability that will have to be paid with cash over the next year, then it is a current liability.

How current assets and current liabilities affect each other

In general, current assets are used to pay current liabilities.

There are a couple of simple financial ratios that can illustrate a company‘s ability to cover its current liabilities.

The current ratio is the simplest of these ratios. It is calculated by taking current assets and dividing them by current liabilities. Usually, you would want this ratio to be greater than 1.0. That means, of course, that a company has the ability (currently) to satisfy all of its current liabilities. However, knowing that every industry is different, you can use competitors or an industry average as a benchmark.

The quick ratio measures solvency in much the same way as the current ratio. It’s a bit more conservative, though. The quick ratio subtracts inventory from current assets before dividing by current liabilities. The reason for this is that while inventory should be very liquid. That’s not always the case. The liquidity of inventory depends on the business’ savvy when it comes to understanding its customers’ demands and appropriate stocking levels.

Finally, there’s the cash ratio. As you might expect, this ratio is even more conservative. The cash ratio divides cash and equivalents by current liabilities. Doing so illustrates the company‘s ability to satisfy its current liabilities without any of the uncertainty surrounding inventory or accounts receivable.

Optimize current assets and liabilities with this worksheet

Complete the form below and click Submit.

Upon email confirmation, the workbook will open in a new tab.

Managing current assets and current liabilities

Now that you know what comprises current assets and current liabilities, you might be interested to learn a couple of tips on how to manage them effectively.

The downloadable worksheet gives you the opportunity to enter some fundamental data in order to better manage cash, inventory, accounts payable (AP), and accounts receivable (AR).

An in-depth explanation of all the terminology is provided in the worksheet.

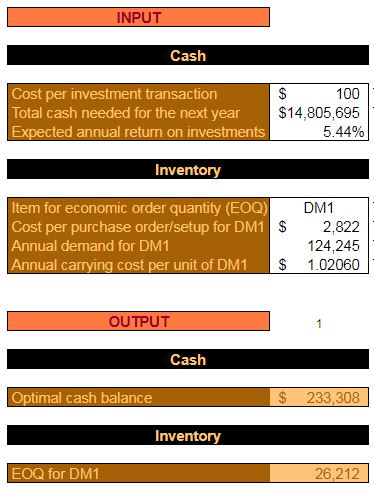

Optimal cash balance

The optimal cash balance measures how much should be kept in your checking account versus an investment account. Specifically, an investment account that will earn a return – even if that return is negligible.

Economic order quantities (EOQ) for raw materials

By entering the required information here, you can pinpoint the exact quantity you should order for each of your raw materials.

Doing so allows you to ensure that you can meet demand, yet not stock too much inventory.

Having too much inventory, as I always say, it’s like taking a stack of money and sticking it on the shelf in your warehouse.

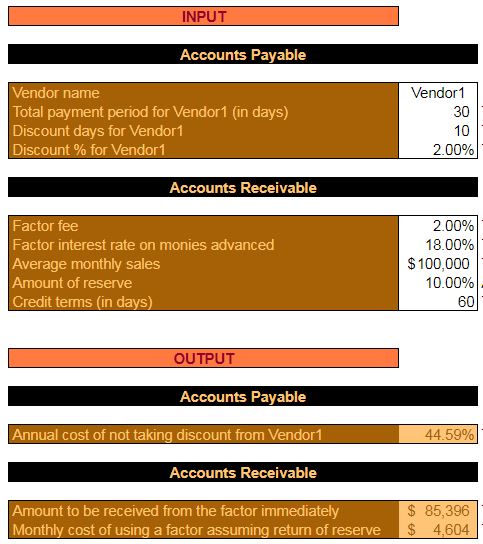

Vendor discounts

Many vendors will offer favorable terms for paying an invoice well before the date that it’s past due. Here, you can calculate what the annual cost of not taking the discount would be.

Depending on your vendors’ terms, it might be that taking the discount isn’t even advantageous.

Factoring accounts receivables

Factoring accounts receivables is when you sell them to a third-party at a discount. The third-party then handles the collection of the AR.

This simple calculator will outline how much in AR you will be sacrificing through factoring. It will also tell you the monthly cost of using a factor. If collecting isn’t your cup of tea, you might consider inputting your information to see if factoring is a viable alternative for your small business.