As millions of Americans struggle financially as a result of the coronavirus outbreak, now is an excellent moment to look for any additional income.

We’re not talking about looking under the couch cushions for spare change or expecting to discover $20 in your coat pocket. Looking online might help you locate money you’ve forgotten about. There’s a good chance there’s some cash with your name on it.

According to the National Association of Unclaimed Property Administrators, 1 out of every 10 Americans has unclaimed property or money floating about someplace (NAUPA).

This money is derived from monies discovered in banks, financial institutions, or businesses that have not been in communication with the owner for more than a year and have been given over to the state. It’s usually a neglected bank or savings account, an uncashed paycheck, stocks, security deposits, customer overpayments, unredeemed gift cards, or an IRS tax return.

Select delves deeper into ways to recover money owing to you and how to cash in on money you’ve earned but may have forgotten about.

How to Find Your Lost Money

During this period, a neglected savings account or a missing salary might be a lifeline for many individuals. Fortunately, there are reliable websites that may assist you in your hunt for these financial windfalls.

To begin, go to NAUPA’s website Unclaimed.org, which is a national network that collects information from all 50 states. There are connections to each state’s official unclaimed property program from there. Because these are all vetted government resources, it’s critical that you use NAUPA-provided websites rather than a general search engine.

Clicking on a state will take you to its official webpage. If you officially changed your last name, look for your unclaimed money using both your current and maiden names. You might also wish to try various search queries, such as using your first initial plus your complete last name.

Because unclaimed property is reported to the state in where the firm or organization is situated, it is typical to have lost money in more than one location, particularly if you have relocated between states. NAUPA suggests utilizing MissingMoney.com, a free website they recommend, to search numerous states at once. Check every state in which you have resided or done business.

How to claim unclaimed money: Each state has its own process when you’re ready to claim your lost money, but it should be pretty straightforward. You need to be prepared to show proof of ownership of whatever you are claiming such as a pay stub, utility bill or your Social Security number. You will also need to have proof of identity, like a copy of your driver’s license or passport. Processing times vary by state but some can take less than 30 days, the NAUPA website says.

Well, that’s it. Now it’s time for you to go check and see if you have any free Money waiting for you to claim. After all, it’s YOUR money!

It is reasonable to wonder why there is a need to get credit cards for your small business. Well, It is not only necessary but extremely vital – especially during the early stages of the business. Essentially, a credit card, or several, is the asset you need to streamline daily expenses while acquiring numerous benefits, including purchase protection and beneficial rewards.

Benefits of Credit Cards to Small Businesses

In a nutshell, here are the primary benefits of credit cards to a small business

Simplified Cash flow and finance purchases

Most startup businesses do not have the luxury of making purchases via cash. Therefore, the ‘spend money to earn money ‘ idea may be limited to some. A credit card comes in handy in the line of cash flow by facilitating purchases for stock or equipment, thus empowering businesses to deliver service or any other orders.

Access to account management tools

The primary benefit of using business credit cards compared to cash is that every cent is usually accounted for. Most companies offer periodical summaries and access accounting programs like Quickbooks, which help them follow their transactions and track their spending.

Streamlined employee expenses

A business credit card is also a smart way to centralize the company expenses and limit them to a single bill. Additionally, it saves business owners the hassle of reimbursing employees whenever they spend on their personal bills and allows them to regulate employee spending.

Redeemable rewards

Typically, purchases made on credit cards earn rewards, redeemable in various ways. Therefore, business owners can compare reward programs while shopping for a business credit card and go for the most sensible ones.

Travel and purchase protections

Business credit cards, like personal cards, also offer exciting travel and purchase protections such as cell phone protection, zero foreign transaction fees, auto rental damage collision waivers, Trip cancellation, interruption insurance, etc. Also, depending on the nature of your business, some credit cards may offer better deals than others.

The 7 Best Credit Cards For Small Businesses

A good business card offers higher spending limits, several rewards, an insurance benefit, and perhaps some cash back. Now that you understand the importance of having a credit card for your small business, here is a round-up of some of the best options for various situations.

Capital One Spark Miles is an excellent choice for business owners chasing after generous cashback as it has a welcome offer of up to a $1000 cashback bonus. The bonus is broken down into two- $500 on the first $5000 spent within the first three months and the other half upon spending at least $ 50,000 within the first six months.

The card also has something for frequent travelers, whereby users get rewards in miles rather than cash or points. A Capital One Spark Miles Card earns you 2X unlimited miles on each purchase made for the business and an additional 5X on rental cars and hotels booked through their affiliate service, Capital One travel.

Other benefits include:

Zero foreign transaction fees

Free employee cards

Low credit score permits- applicants with limited fair credit may qualify

The American Express Business Gold is ideal for the big spenders as it has a relatively high annual fee. Regardless, users stand to earn massive rewards thanks to the 4X reward rate in two categories from the following options:

Shipping

Gas Stations

Advertising Purchases

Technology

Restaurants

Airfare

The 4X points are redeemable for the first $150,000 spent annually and any top two categories, and a point per dollar earned after that. The Amex Business Gold Card also offers customers robust travel benefits and flexible redemption and point transfer options.

Chase Ink Business Cash is the ultimate go-to for many business needs. They reward you for things you are sure to spend your money on, such as business phone services, Internet and cable purchases, gas stations, and restaurants. They offer 2% to 5% cash back on the first $25,000 spent on these essential services and guarantee a 1% cash back on all other purchases.

With a Chase card, you can save on collision insurance, usually offered by rental car companies, and allow you to protect valuables from theft or damage for 120 days on $10,000 per claim and $50,000 per account. It certainly does not end there, as the benefits extend to manufacturer warranties on purchases made within an additional year.

This card offers zero annual fees and 2% cash back for $50000-worth of purchases made within a year, followed by 1% cash back on other purchases. The Blue Business Cash Amex also empowers its users to spend above their credit limit through an expanded buying power program.

Other considerable benefits include the following:

Automatic crediting of rewards to your statement

Zero charges for employee cards

Account management tools, including an end-year summary and expense report

The Chase Ink Business Unlimited credit card is an excellent addition to the Chase Ink credit card line-up. It has numerous similarities to a personal credit card, offering 1.5 % unlimited cashback on purchases across all categories. It also provides employee cards at no additional costs and a zero annual fee.

Similar to the Ink Business Cash Card, the Unlimited version has a $900 cash-back sign-up bonus for newcomers for $6,000 spent within the first month. However, Chase Ink Business Unlimited earns customers the highest base rate, which could benefit businesses that spend huge amounts on expenses.

The major selling point of the Business Platinum Card is the welcome offers that usher new users to 120,000 Amex Membership rewards after spending $15000 within the first three months. Other considerable benefits include the following:

5X points earned on booking flights and making hotel reservations through the Amex platform

Statement Credits for purchases with Dell and a CLEAR membership

1.5x points on purchases from various categories

A free pass to Global Lounge Collection

The premium card may have a $695 annual fee. Regardless, the perks definitely outweigh this hefty price.

The CitiBusiness Advantage Platinum credit card is a great option for small business owners looking for a standard rewards program with some benefits, including:

Introductory APR for purchases and balance transfers

No annual fee

A chance to earn 1 point per dollar on purchases and 2 points per dollar on travel and dining purchases

The chance to earn 5 points per dollar spent on qualifying business expenses, including business cards and business checking accounts

Small businesses around New Jersey have continued to emerge, creating a great environment for investment. Business insurance plays an essential role in the development and establishment of your enterprise by covering costs associated with liability claims and property damages. As a business owner, especially small enterprises in New Jersey, insurance should be the first option you look into to protect your assets.

Over the years, NJ insurance companies’ growth and diversity have greatly influenced the better performance in creating accommodative and efficient services that even cover small businesses. In this article, we are going to discuss the importance of insurance in NJ.

What types of insurances would a NJ small business need?

There are various types of insurance involved in businesses. They are mostly determined by the type of business you have, a risk profile, products or services offered, and employees and clients, among other possible improvements that may be put in. Some of the insurance packages that you can consider in New Jersey include:

General liability insurance in NJ. This covers damage costs and potential lawsuit claims if someone accuses your business of property damage, bodily injury, or slander.

Professional liability insurance. Also known as errors and omissions (E&O) insurance, professional liability insurance partially pays for any damage and lawsuit costs made on work mistakes, missed deadlines, and incomplete projects.

Business income insurance. Also known as business interruption insurance, this type of insurance aims at helping you recover your lost income, which may be very efficient, especially for a small business, before it becomes completely stable. This coverage can help you pay ongoing expenses such as rent, payroll, and utility bills.

Commercial auto insurance. It covers accident damages that may happen when driving for work. This helps protect you and your employees, especially while using company-owned vehicles for business. This can help cover for property damage and bodily injuries.

Workers compensation insurance. It aims to compensate employees who may suffer work-related injuries in covering for their medical bills, funeral costs if an employee loses their life due to work-related injury, and compensation for their lost wages.

Flood insurance in NJ. Flood insurance is only necessary if you are located in a flood zone. To find out check out this website NJFloodMapper where they show flood zones in NJ

Business insurance mainly depends on the policy limits set in other states. Insurance policies are set to promote stronger and more effective services to businesses and thus require equal treatment for all businesses. Public policies also help your business get approved for coverage, especially concerning the state policies that regulate insurance operations and business.

Process of getting an insurance

In New Jersey, to obtain an insurance license, you must follow a series of steps that make your business viable for insurance coverage. These steps include:

Assess your risks. This can be easily determined by understanding and defining your work, the kind of accidents that may occur, and the lawsuits that may face your business. These can help you know what kind of package is necessary.

Identify the type of insurance best suitable for your business. Considering small businesses, you must choose an efficient package that will adequately cover you in case of any damage. Also, familiarize yourself with the types of insurance policies required in New Jersey that can help determine the license you need. It is important to understand what insurance should also include to help you have better control over the choices you will make.

Perform an online search on insurance providers highlighting their services and reliability. Small businesses can easily be tricked into engaging with fraud and inconvenient coverage that may affect your business. A reputable licensed agent must put your best interests and serve as they were their own. Commercial insurance agents can also help identify policies that match your business needs.

Background check. This is essential in insurance covers that also help you ensure that the coverage is in line with the New Jersey state policies and is fulfilled effectively.

Shop around. Compare the different rates and terms of work and service from different agents that can help you have a different opinion or view before making a final decision. Compare significant benefits and prices that can be efficient for your business.

Re-assessment. Your business continues to grow, and thus your liabilities. Perform a thorough assessment of your business after a certain period. New developments and operations affect your coverage. Thus, discussing this with your insurance cover is important to ensure convenient coverage.

Small business insurance providers in New Jersey

Techinsurance specifically deals with small business insurance for technology businesses. They are aligned with state requirements and policies and thus can adequately protect your business.

Hortica insurance. They are involved with horticultural products, including greenhouse growers, nurseries, and florists.

Other insurance providers like Plymouth rock assurance, Insureon, are also involved in creating solutions for your small business through efficient coverage with reasonable packages. However, it would be best to research the different rates and their reliability or effectiveness. This is an essential part that may affect your business very dearly. Thus, take your time to ensure you have the right partner.

Gary’s Insurance Agency LLC – with over 775 review on Google, Gary’s Insurance Agency in Linden, NJ is a solid option for your insurance needs.

Dollar A Day Insurance – with 14 reviews and an average rating of 3.3, Dollar a day insurance isn’t the top of the list of recommended insurance provers. However, they are an option for you to explore.

Final thoughts

Setting up your business in New Jersey is a viable option, especially due to the policies on insurance coverage. You must ensure that your coverage is effective and convenient. Learn as much as you can about the insurance providers and the policies they use, especially if they align with state regulation.

In order to estimate how much in sales your startup can hope for, you’re going to have to estimate the market size for your product/service(s). This is critical for your startup because it will give you an idea of your business’ potential. It will also help you plan for capacity-related issues.

2 approaches to estimating the market size for a business plan

I cover this topic more in-depth in a post on market size and growth rate on my sister site, InvestSomeMoney.com.

The context there is focused on investing your money in a publicly-traded company. Though that’s a little different than what we are doing here, the fundamental principles remain the same.

The goal is to determine how many potential customers there are for a business and how much they are willing to spend. In order to do that, we can employ two general methods. These methods are a top-down analysis and a bottom-up approach to understand market size and growth.

One way to think about this is that a bottom-up approach uses multiplication and a top-down analysis uses division to arrive at an estimated market size.

After writing on this subject several times, I’ve come up with another way to think about these methods. I think a bottom-up approach should look internally, at things like unit size and capacity. A top-down analysis should look externally at things like demographics and market research.

Looking at this from these two different perspectives opens the door for further analysis. When you’re done, you should know whether you can expect to be capacity constrained or demand constrained. You’ll also start to flesh out some ideas that will help you further into your business plan.

If you do an analysis with both approaches, you can compare the results. For instance, if your bottom-up approach is higher, you’ll know that you could have excess capacity issues. You need to consider scaling that back or otherwise expanding your product/service offering to drum up additional demand.

Conversely, if your top-down analysis reveals that demand is in excess of capacity, then you are leaving money on the table. Time to start thinking about what you can do to scale up and capture as much of the market as possible.

Let’s start by taking a look at a bottom-up approach to estimating the market size for a business plan.

Bottom-up approach example

On my sister site, InvestSomeMoney.com, I researched three real-life examples of a bottom up market sizing approach. In those examples, you’ll see that they sometimes mix in a little top-down analysis with their bottom-up approach and vice versa. There’s no rule against doing that, but I would rather look at things from two totally different perspectives.

When using a bottom-up approach, try to start with the most simplistic piece of firm information you can get your hands on. Then, start to build on it with other information, or the best guess you can muster.

You can think of a bottom-up approach as one that focuses on how much and how often customers will buy.

This information might be something you have internally. Or, it might be from the information you found by researching online. Start with a single “serving size” of your product/service. Then, think about how often a customer would buy. Work your way up from there.

There’s still a lot to consider regarding packaging volume and dosage. That will require more thought. But, for the time being, I’m going to estimate the volume of a one month’s supply and the daily dosage to be the same as Rogaine. If that changes as I progress with my business plan, I can easily circle back to this and plug in different numbers.

With Rogaine as my benchmark, I know that a dosage of my product would be 1 mL. The product would be used twice a day. My product would come in 2 oz (60 ml) bottles. Each bottle would be one month’s supply, as I said.

Thinking about capacity

Okay. Now that I have a grasp on the package size – what about blending and packaging? If this idea were to come to fruition, I don’t picture myself blending batches in my bathtub and filling bottles with a ladle and a funnel. I would need access to some sort of industrial equipment.

Fortunately, a quick internet search shows that there is no shortage of contract blenders and packagers out there. Especially for food and supplements. What it costs, remains to be seen. That’s an issue for another time. For now, I just want to get an idea of how much I could manufacture.

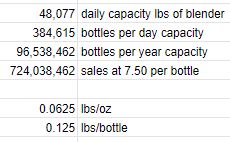

This company claims it can blend 1.25 million pounds per workday. We’ll assume, for now, this represents the average contract blender/packager. What does that translate into in terms of 2 oz bottles?

First of all, I wouldn’t need all 26 of their kettles. Only one, tops, especially at startup. So, if we divide the 1.25 million pounds by 26, we get a per kettle capacity of about 48,000 lbs per day.

Pounds are a weight unit of measure (UOM) and ounces are a volume UOM. To make the conversion, we’re going to have to do some more estimating.

Water weighs a little over 8 lbs/gallon. We’ll assume my product has roughly the same density.

8 lbs ÷ 128 oz (per gallon) = .0625 lbs/oz. With each bottle containing 2 oz, we know that it’ll weigh approximately .125 lbs/bottle.

This means that with one of this company’s kettles, I could blend 384,615 bottles worth of product per day. 96.5 million bottles per year. At an approximate sales price of $7.50 per bottle, that translates into nearly $725 million in revenue per year.

Okay, I’ve looked at things from a bottom-up, capacity-focused approach. Let’s now consider a top-down, demographic-focused analysis.

Top-down analysis

Not surprisingly, I also wrote a post on InvestSomeMoney.com with examples of a top-down analysis to determine market size for a business plan. When you read through it, you might notice that some of the examples use Census data (or something similar). They take big chunks of information and start narrowing down their market from there.

Which brings us to three important terms for performing a top-down analysis. These are:

Total addressable market (TAM) Serviceable available market (SAM) and Serviceable obtainable market (SOM)

A SOM is a fraction of the SAM. In turn, a SAM is part of the TAM.

The TAM can be thought of as every potential customer that you can reach geographically. The SAM is what’s left when you niche down a little into the population that is a good fit for your unique selling proposition. Finally, the SOM represents the percentage of the SAM you can realistically expect to take.

It’s unlikely that you will ever capture 100% of the SAM. Even in a specific niche, you can’t be everything to everyone. That’s alright, though. The goal of this exercise is to make realistic estimates so that you have a sound business plan to work from.

When doing a top-down analysis, start with a large population or an overall industry size. From there, narrow down your customer until you arrive at your SOM. It helps to have a “customer avatar” in mind before starting a top-down analysis so you know where to niche down to.

I would suggest you perform a business plan demand analysis first to get a crystal clear picture of what that avatar is. You might think you know it intuitively. But you might be surprised at what you find – like I was!

A top-down analysis for my business plan

I know that not every person in the U.S. (much less the world) is going to want or need an all-natural topical supplement for hair loss. Who might though???

I’ll refer back to my handy-dandy business plan demand analysis (linked above) to see what I can find.

Here, I’m reminded of the ages that men and women first started experiencing hair loss. I’m reminded of the percentage that has sought any sort of treatment. Finally, I’m given an idea of what types of treatment they have tried.

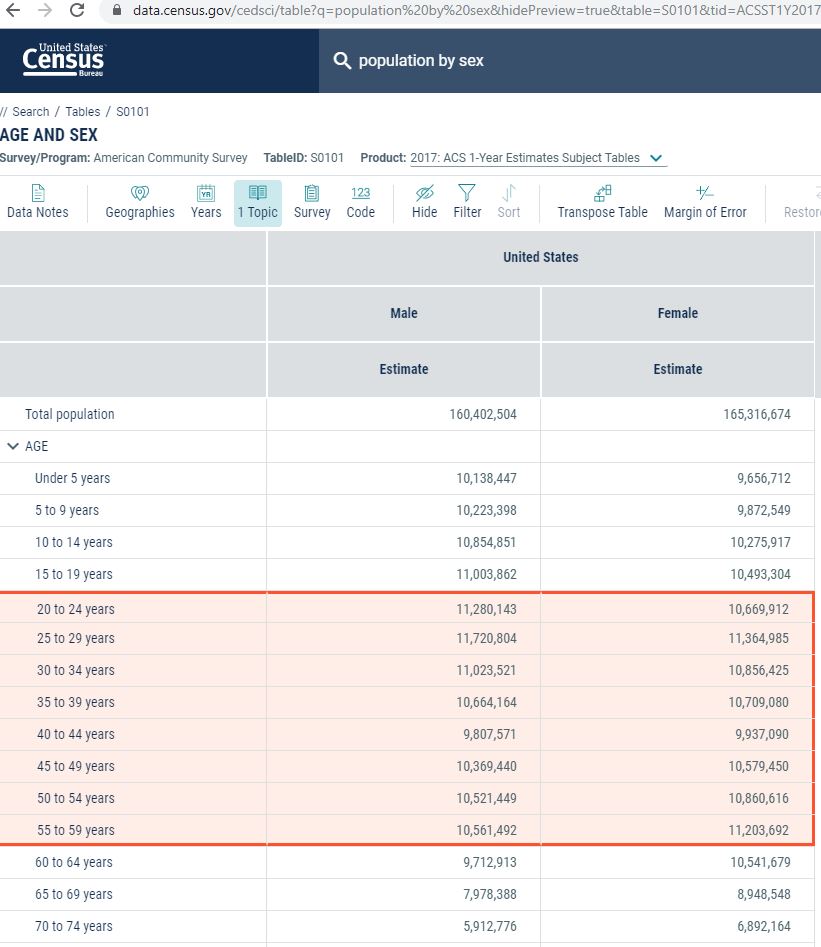

A quick visit to Data.Census.Gov and I find table S0101, which gives me the U.S. population by age and sex. I customize and filter the table real quick. Then, I copy and paste the data I need into my spreadsheet.

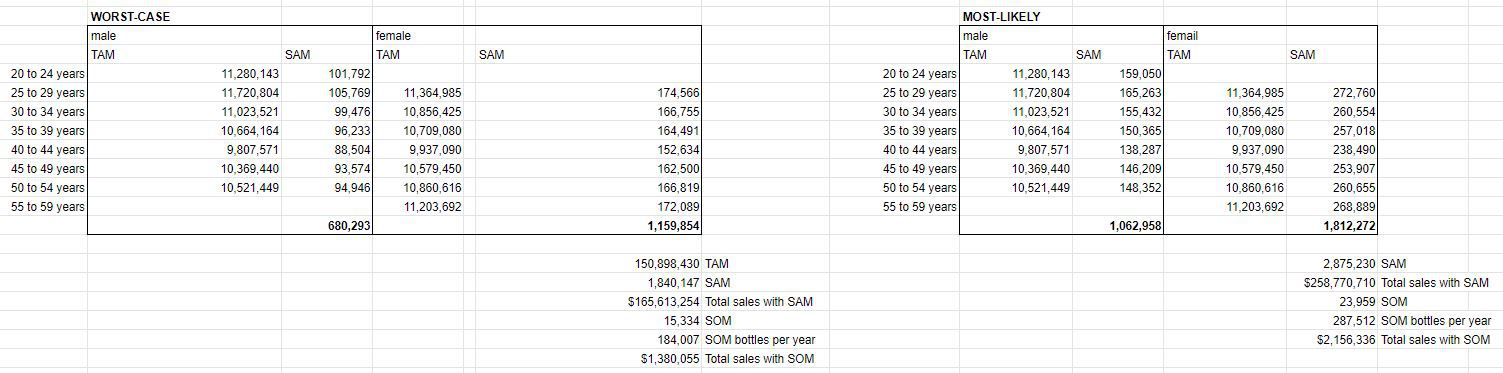

Next step is to narrow these numbers down. I’ll use the “regular” numbers and the pessimistic numbers from sensitivity analysis from my business plan demand workbook.

I want to know the percentage of men who have had hair loss and tried any sort of treatment. Then, I want to go deeper and estimate the number that has found supplements to be effective. I’ll do this for both the most-likely and the worst-case scenarios. On the women’s side, I’ll do, more or less, the same thing.

TAM and SAM

You’ll see that I didn’t use the same age ranges for men and women. I assumed that males would start experiencing hair loss earlier, but would also stop caring about it earlier too.

The age range for males in my TAM was 20 – 54. For females, it was 25 – 59. This translates into a TAM of 151 million people in the U.S.

For the SAM, my worst-case scenario estimated that .9% of the male population in the target age ranges would be part of my market. 1.54% of females in the target age ranges were also assumed to be part of my market. This translated into a worst-case SAM of 1.8 million people.

As for my most-likely SAM, I estimated that 1.41% of males and 2.4% of females in the target age ranges were potential customers. This resulted in a SAM of 2.88 million people. Over a million more potential customers.

SOM

SOM is tricky.

Who’s to say what percentage of the SAM my company could capture? Obviously, it would start at 0% and work its way up from there. Where would it stop though?

It will depend, in part, on the number of companies vying for this niche. As I often do, I will refer to the Pareto principle. The Pareto principle states that 20% of the inputs will be responsible for 80% of the outputs. Put another way, 20% of the companies will have roughly 80% of the market share.

I’ll refer back, again, to my post on business plan demand. In it, I found three direct substitutions for my topical hair loss product. I won’t include Minoxidil (Rogaine) in that group, because of its unnatural chemistry.

Again, without getting too mired in math, I estimate that there are approximately thirty companies in the topical hair loss supplement space. This was a quick and dirty estimate based on the results of an internet search.

Six of those thirty companies probably control 80% of the market. That leaves 4.2% (1 ÷ 24) of the remaining 20% as my short-term SOM. Obviously, if my product were to take off, that amount could grow considerably and could approach the SAM.

What that means as far as the market size is 15K people worst-case and 24K people most-likely. At 12 bottles purchased per year, this translates into 184K and 287.5K bottles per year respectively.

Here’s a look at the spreadsheet breaking that all down:

Click to enlarge

Comparing a bottom-up and top-down analysis when determining market size for a business plan

Obviously, a couple hundred thousand bottles (top-down) is a far cry from 96.5 million (bottom-up). So, it would appear I will not be capacity constrained in the near future. In fact, as this startup moves forward, I need to make sure I’m not over-buying capacity. Those huge fixed costs could kill my business before it has a chance to get off the ground.

Speaking of fixed costs, the information from this analysis has given me good data to build my pro forma financials – when that time comes.

Now, at some point in the future, selling my product internationally could be an option. However, in this tiny niche, it is unlikely that I’ll ever need that much capacity for this one product.

Market size for a business plan

What were there factors I didn’t consider (but should have) when estimating my potential market size?