There are two methods that can be used to allocate costs in a process costing system. They are weighted average or FIFO (First In First Out). Accountants and business owners can decide which method to use based on their preference for simplicity or accuracy. Of course, there are differences between the two methods. But, they also share similarities…

The FIFO and weighted-average methods each always use these same inputs:

- Ending WIP units

- Percentage complete for materials & conversion

- Amount spent on materials & conversion

Here’s a look at some of the differences between the weighted-average and FIFO methods (by step):

| Unit Reconciliation | Cost/Equivalent Unit | Cost Allocation |

|---|---|---|

| Weighted-average method | ||

| Considers begin WIP 0% complete | Allocates the value of begin WIP | Begin WIP + Monthly expenses = Amt completed & transferred + End WIP |

| FIFO method | ||

| Considers begin WIP partially complete | Allocates expenses incurred | Monthly expenses = Amt to complete begin WIP + Amt started & completed + End WIP |

Both methods are, generally speaking, similar. Which you should use depends in large part on preference. It also depends on your ability to conceptualize what is taking place.

A process costing system is primarily used by manufacturing companies that mass-produce a bunch of the same product. A process costing system can be contrasted with a job order costing system. A job order costing system would be used by companies that offer custom products and/or services.

Download the example workbook

Looking for a spreadsheet to build an entire process costing system (weighted-average method)? Read this post:

DEFINITION AND FEATURES OF A PROCESS COSTING SYSTEM

Complete the form below and click Submit.

Upon email confirmation, the workbook will open in a new tab.

Process costing – FIFO vs weighted-average

Need more help with your accounting homework? Read this:

WORKSHEET POSTS

The weighted-average method might be considered simpler. But, the FIFO method might be considered more accurate. That being said, once the groundwork is laid for a FIFO process costing system, calculations should be made automatically and require a minimum of effort on your part. That is…if everything’s set up correctly.

Below, I’ll compare the calculations from the weighted average and FIFO methods. Each will refer to the same inputs – Item1, Dept A, from the Process Costing workbook. That way, you’ll be able to compare the two methods side-by-side, apples-to-apples, and decide which makes the most sense for your company. Then, you can move on to more pressing matters.

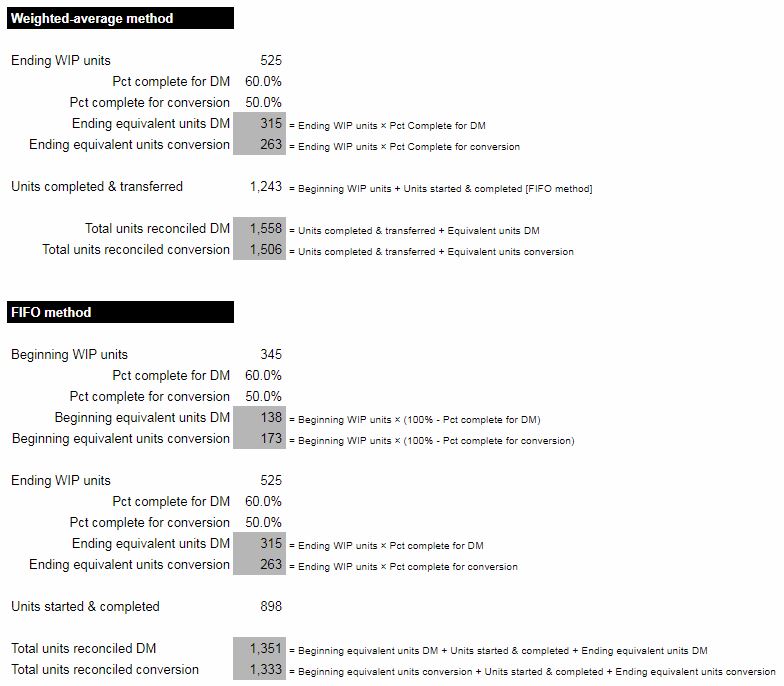

Unit reconciliation

Have more questions about the FIFO method of costing? Read this post:

FIFO METHOD – WHAT IT IS, WHY & HOW TO USE IT

The purpose of unit reconciliation is to determine the total number of units to allocate costs across in a given month.

Obviously, those units that were completed will be included. But, also factored in, are “equivalent units.”

Equivalent units

Equivalent units = WIP units × Pct complete

These units are calculated for direct materials (DM), direct labor, and overhead individually. Why? Because these value-added costs are not applied uniformly.

For simplicity’s sake, overhead is assumed to be applied on the basis of direct labor hours. These two costs are, therefore, combined in this example and called conversion (costs).

Pct complete examples

For example, a particular product might have all its materials added immediately when it enters a department. The labor and overhead, however, might be added at a slower pace as those materials are assembled, mixed, machined, or whatever… In this case, the percentage (Pct) complete might be high for DM, but low for conversion.

Conversely, the most costly direct materials might be added during the last operation in a department. Since a lot of conversion costs have been applied, but the most expensive DM are not added until the end, the Pct complete might be high for conversion, but low for DM.

Hopefully, that makes sense. Reread it if you need to.

It all depends on the product being produced and the nature of the value-added in a given department.

Beginning WIP units

You’ll notice that Beginning WIP units aren’t factored into the unit reconciliation calculation for the weighted-average method. With the weighted-average method, Beginning WIP is considered to be started & completed in the current month.

No matter if last month’s Ending WIP units were 99% complete for DM and conversion costs. This month, Beginning WIP units are considered 0% complete. Under the weighted-average method, that is.

With the FIFO method, Beginning WIP units are included in Total units reconciled. Specifically, the equivalent units that weren’t included in last month’s calculation. For example, suppose last month’s Ending WIP units were considered 30% complete. Then, this month 70% of the Beginning WIP units will be used in the Total units reconciled calculation this month.

In fact, if you change the Pct complete for DM and conversion to 0% for the FIFO method, you’ll see that the Total units reconciled are the exact same amount for both methods.

DIFFERENCE 1: THE WEIGHTED-AVERAGE METHOD CONSIDERS BEGINNING WIP TO BE 0% COMPLETE. THE FIFO METHOD DOES NOT.

Completed & transferred vs started & completed

This subtle difference in verbiage makes a big difference in calculations between the weighted average and FIFO methods.

As mentioned above, Beginning WIP is always considered to be 0% complete with the weighted-average method. Ending equivalent units are added to Units completed & transferred to determine the Total units reconciled with the weighted-average method.

With the FIFO method, that is not the case. Since Beginning WIP units are already considered partially complete, Units started & completed are quantified separately. As the title implies – these are units that were both started and finished in a given month.

Total units reconciled

The weighted-average method adds the Ending WIP equivalent units to the Units completed & transferred to arrive a quantity for units reconciled.

The FIFO method does something similar. Ending WIP equivalent units are added to Units started & completed. Beginning WIP equivalent units (1 – Pct complete) are then also added to that quantity.

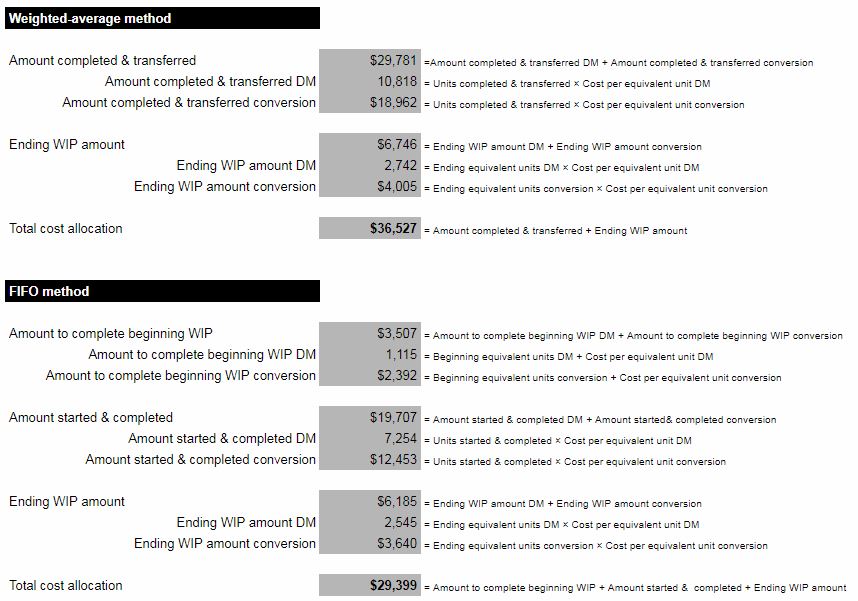

Cost per equivalent unit

Unit reconciliation only focuses on units. No costs were considered. Now, it’s time to tally costs for the month and to calculate a Cost per equivalent unit.

Cost per equivalent unit = costs to be allocated ÷ Total units reconciled

Comparing total costs between months, years, or even days doesn’t give you the whole picture. In order to have the whole picture, total costs must be compared using some sort of common denominator

Hence the need to break costs down on an equivalent unit basis. Equivalent units take into consideration how many units were started, completed, transferred, and left in WIP at the end of the month. Every unit and every dollar is accounted for. So that accurate comparisons can be made.

Total costs to be allocated with the weighted-average method includes the value of Beginning WIP + Monthly expenses incurred. So, since Beginning WIP units were considered 0% complete and added to the Total units reconciled, the Beginning WIP amount (last month’s Ending WIP amount) is also included in the numerator to offset these units.

DIFFERENCE 2: THE WEIGHTED-AVERAGE METHOD ALLOCATES THE VALUE OF BEGINNING (LAST MONTH’S ENDING) WIP. THE FIFO METHOD ONLY ALLOCATES EXPENSES INCURRED THIS MONTH.

Total costs to be allocated under the FIFO method only includes the Monthly expenses incurred. Only costs from this month are used to calculate Cost per equivalent unit.

Because the weighted-average method includes the value of Beginning WIP and the FIFO method does not, the weighted-average method will always have higher Total costs to be allocated. Whether that translates into a higher Cost per equivalent unit depends on the Beginning WIP units and the Units started & completed.

Cost allocation

Whereas the Total costs to be allocated include costs that the company started the month with (weighted-average method) and those that were added. The Total cost allocation includes costs that were passed to the next department (or finished goods) and those that the company ended the month with.

The Total costs to be allocated should always equal the Total cost allocation. Costs can’t just disappear into thin air.

In the weighted-average method, the equation balances as follows:

Beginning WIP amount + Monthly expenses = Amount completed and transferred + Ending WIP amount

In the FIFO method, the equation balances as follows:

Monthly expenses = Amount to complete beginning WIP + Amount started and completed + Ending WIP amount

Weighted-average or FIFO for process costing?

Conventional wisdom says that the weighted average method is simpler than the FIFO method. I suppose this is said because Amount to complete beginning WIP need not be calculated for the weighted-average method.

Do you have homework questions about a job order costing system too? Read this post:

JOB ORDER COSTING SYSTEM – EXAMPLE, TEMPLATE, & HOW-TO

But, since you will be determining the Pct complete for DM and conversion costs for Ending WIP units (which will become your quantities for next month’s Beginning WIP units) it shouldn’t matter. The calculation is already made.

Learn more about cost minimization here.

Better to go with the method that produces a more accurate Cost per equivalent unit. Rather than one that blurs the lines between what was done last month and what was done this month. Particularly if you are in a super-competitive environment where accurate costs are needed to price appropriately.

Yes, I know that the Spreadsheets for Business Process Costing example workbook uses the weighted-average method. Confession: it wasn’t until I wrote this post that I really explored the difference between the two methods. If it ever makes sense to redo the process costing example workbook, I will use the FIFO method.

What do you think? Are there any circumstances where the weighted-average method makes more sense?

Is there something I missed? Or, do you have any questions?