What is considered inventory for a restaurant? Video summary

Inventory information is only useful if it contains critical data. Having access to your restaurant’s most important information will help you make smart decisions for your restaurant.

Actual inventory levels must be consistently physically counted and compared to amounts listed in the software. Corrections in the software must be made if there is a discrepancy.

Many restaurant software tools will help to keep track of inventory. However, if they don’t, you can’t neglect this task. Even if they do, periodic inventory counts are still necessary.

What should a restaurant inventory list look like?

There are five fields that are critical for a restaurant inventory list.

These fields are:

Item

The name of what’s being counted

Unit of measure (UOM)

A consistent quantity that will be used for counting and costing

Quantity on hand (QOH)

How many UOM the restaurant currently owns

Item cost

Don’t count in one UOM and cost in another

Extended cost

QOH × Item cost

The total value of the inventory

Additionally, you can include other fields in your restaurant inventory list if appropriate. For example:

Category

Meat, vegetables, raw, prepared, etc.

Location

If you have more than one

Any other classification that helps you manage inventory

The restaurant inventory list

Fill out the critical fields for every item you own. If you must, it is okay to use multiple lines for the same item. The pivot table functionality of the spreadsheet can handle it.

Your restaurant’s POS (and other types of) software might be able to help with inventory management. It depends on the software functionality. Some software will track inventory usage. Your accounting software might track purchases too and may keep running inventory levels.

Not every piece of software will keep track of waste, spoilage, and other losses, however. Therefore…

Cycle counting of restaurant inventory will still always be necessary. This ensures that your inventory counts are accurate and you can meet demand and avoid waste.

Employees play an important part in inventory management. Consider giving them an incentive for accurate inventory counts. Explain to them the importance of accuracy.

When cycle counting – maintain a consistent schedule and stick to it! Inventory items with high turnover should be counted more frequently.

Finally, remember to track waste and food loss. Particularly if your software does not. During the hustle bustle of the workday, it may not be possible to accurately measure wasted quantities. Do your best to estimate them. Inventory amounts will be accurately adjusted next cycle count.

Utilize the Food Waste spreadsheet on the Why Spreadsheets Are Your Restaurant’s Best Friend workbook (download above). Also, take advantage of the other spreadsheets in the workbook including:

Scheduling template

Vendor order sheet

Daily prep list

Inventory control

Food/recipe costing

Food waste

Sales per day

More considerations regarding your restaurant inventory list

Only consumable items that you use to prepare food should be included in your inventory. Not every asset should be included here. Things such as flatware, cookware, glassware, etc. are not inventory.

It’s important to keep accurate records for these assets, but they are not inventory. Inventory is what you sell to your customers.

Again, make sure you’re using a consistent UOM for your inventory items. Use whatever is easiest to track. Whether it be Lbs, Gal, Oz, Cans, Cases, Flats, whatever – just stay consistent. Doing so will ensure that costly errors in counts and valuation aren’t made.

Food costs are rapidly changing. So what cost should you use?

Your POS or accounting system might track costs for you. If so, great. If not, it might make sense to assign a standard (expected) or average cost to inventory items.

No matter what inventory cost you use, make sure you’re relieving inventory on a First In, First Out (FIFO) basis. E.g. use your oldest inventory first, assuming it’s fit for consumption, of course. No other industry has to wrestle with the issue of spoilage more than the restaurant industry. So, do what you can to avoid needless waste of inventory and dollars.

Again, at the risk of beating a dead horse, make sure your costs reflect your UOM.

Finally, one of the primary benefits of managing your restaurant inventory is that you can measure inventory days on hand. In order to do so, you must keep track of inventory usage on a daily basis.

Inventory days on hand = inventory on hand ÷ average daily usage. Assuming that you are meeting all of your customer’s demand (not running out of stock) then the lower your inventory days on hand, the better.

Questions about How Do I Make a Restaurant Inventory List?

What challenges do restaurants have with managing inventory?

Spoilage is one inventory problem that the restaurant industry is particularly prone to. Many inventory items, by necessity, have an extremely short shelf life.

Accountability is another. With so many different individuals handling and recording inventory, it can be difficult to ensure that QOH in your software matches reality.

Finally, running out of inventory can hurt customer service for a restaurant more than it can other industries. While other businesses can put an item on backorder for a customer – restaurants can not.

These are just a few. There are many more unique challenges that restaurants face in managing inventory.

How does one manage quality control and inventory control smartly in a restaurant for an owner who lives in another city?

Most importantly, it is critical to find employees that can be trusted to manage inventory smartly. Also, while you want every employee to use best practices when it comes to inventory management, you’ll probably want to have one trusted individual who will have ultimate accountability.

Which is the best software for inventory control in a restaurant?

There are a lot of options out there. However, a piece of software called Restaurant 365 seems to be pretty well regarded. I’ve never used it myself. So, I can’t attest to its quality. In my brief searching, though, I never saw any negative feedback. Pricing will run from $250 to more than $450 per month per location.

Spreadsheets are also often recommended. They take some work to get set up, but one major benefit is the ability to customize them to your needs. Feel free to download the inventory control spreadsheet above and check out the Why Spreadsheets Are Your Restaurant’s Best Friend post and video.

How do I make an inventory list and other spreadsheets for my restaurant?

Spreadsheets serve as a great complement to, or replacement for, the other software a restaurant might rely upon. Spreadsheets can handle nearly any task you require of them. They are very versatile. Small restaurants, with a limited software budget, might find them particularly useful.

The author states that a computer is “Second only to a good set of knives”. And spreadsheets are “the cat’s meow.” They can help a restaurant with organization.

Spreadsheets can intimidate some people. But, they are only as complicated as you make them. It is suggested that you take a course if you must. Particularly if you want to take advantage of the power of formulas.

Spreadsheets will make your life as a restaurant manager easier. Once you take a little bit of time to climb the learning curve.

Spreadsheets can fill in gaps in functionality for pieces of software. Many POS systems and most accounting software will export to .csv format – which can then be imported into a spreadsheet.

Some of the things a restaurant can use spreadsheets for

Staff scheduling

Drop in pre-made shifts for each employee

Order sheets

Purchase orders for ingredients

Automatically calculate tax and totals

Vendor lists

A master list of all vendors with name, address, phone, and email

Keeping good documentation will help with financing. Good documentation provides detail about how and why your startup restaurant will be successful. Spreadsheets are an excellent tool for providing documentation.

The financial projections section of your business plan is where you forecast your sales, expenses, cash flow, and capital projects for the first five years of your small business’s existence.

This is a critical section for readers of your business plan. It tells them:

How you expect your startup to perform financially

When you expect your new business to be profitable

How profitable you expect it to be

These are things you’d want to know as an investor, right? It’s up to the reader to decide whether they think your forecast is feasible.

Additionally, as an entrepreneur, it forces you to consider, thoroughly, what the first five years of business might look like. This will give you a good plan to work off of, will help you to be proactive, and will increase your likelihood of success.

Finally, the financial projections are the foundation of your funding request. Of course, your funding request, after all, is the primary purpose of your business plan.

Without knowing how much cash you need to launch and operate early-on, you won’t know how much you need to ask for. The funding request relies heavily upon financial projections, particularly the capital budget.

An example of a funding request, for this same business, will be posted separately.

This example of financial projections is built off of two previous posts:

Download the restaurant financial projections spreadsheet

If you’d like to download the spreadsheets I used to make these financial projections for a restaurant that can be done below. Keep in mind that these were (hastily) built off of budgets for a manufacturing company and tweaked for the restaurant industry. However, they should serve as a good starting point.

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

Startup restaurant financial projections

The financial projections for Diner, LLC provide a well-thought-out, cohesive, and comprehensive forecast of the restaurant’s performance from initial funding through the fifth year of operation. These forecasts will validate the feasibility of the concept and the appeal of an investment in this venture.

The financial projections for Diner, LLC include an initial capital budget for all of the fixed assets and other costs necessary to launch the restaurant.

Additionally, five years of pro forma income statements are included. These pro forma income statements are built off of a detailed five-year operating budget.

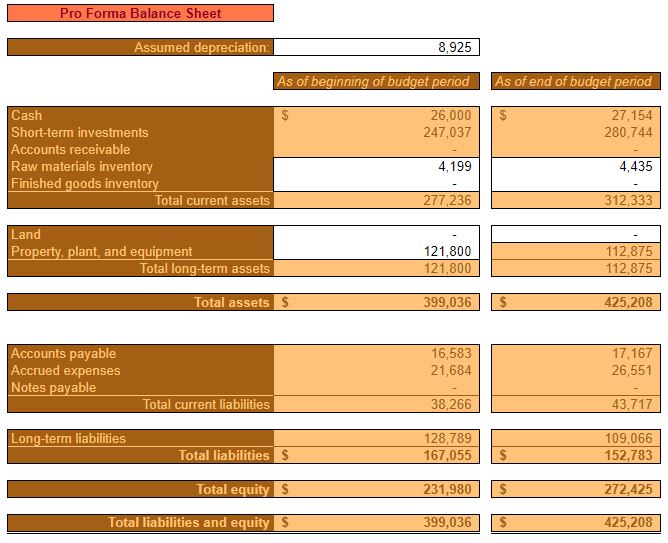

Furthermore, five years of pro forma balance sheets are also included. These pro forma balance sheets are built on five years of detailed cash flow analysis.

For the purpose of brevity, not every detailed budget is included in this business plan. However, all are available for decision support, upon request.

Items in italics represent those directly referenced in the financial projections.

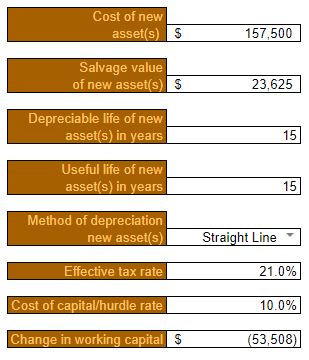

Startup restaurant capital budget

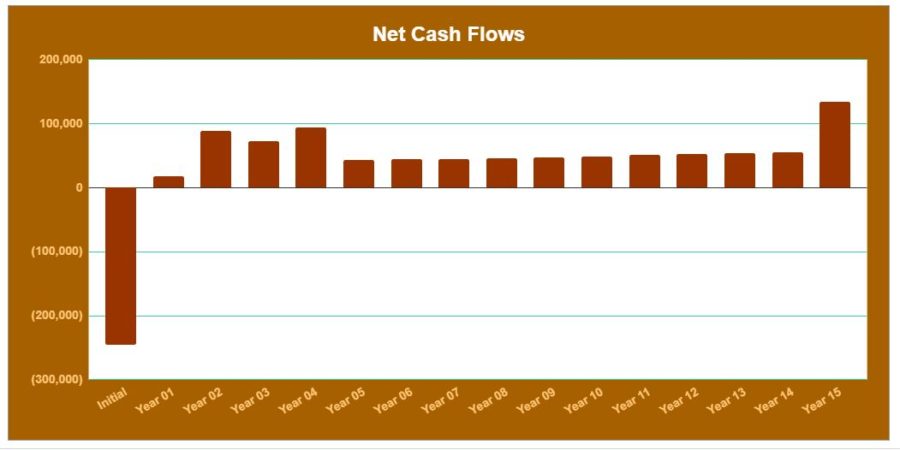

The capital budget summarizes Diner, LLC.’s forecasted operational and cash flow results over the next fifteen years. It takes into account:

Fixed assets needed to operate the restaurant

Launch costs necessary to begin operations

Cash-on-hand needed to launch the restaurant

To cover unanticipated expenses

Fixed assets necessary to operate Diner, LLC. are estimated to cost $157,500.

The salvage value after fifteen years is estimated at $23,625.

On average, all assets are assumed to have a depreciable (and useful life) of fifteen years.

Fixed assets will be depreciated using the straight-line method.

The effective tax rate, for purposes of calculating a depreciation tax shield, is estimated at 21% throughout the capital budget.

A discount rate of 10% is used to calculate NPV and other capital budgeting metrics. This discount rate considers the cost of borrowing (6%) and adds an additional risk premium of 4%. 6% is the estimated interest rate for an SBA 7(a) Small Loan and is calculated by adding 2.75% to the current Prime Rate (3.25%).

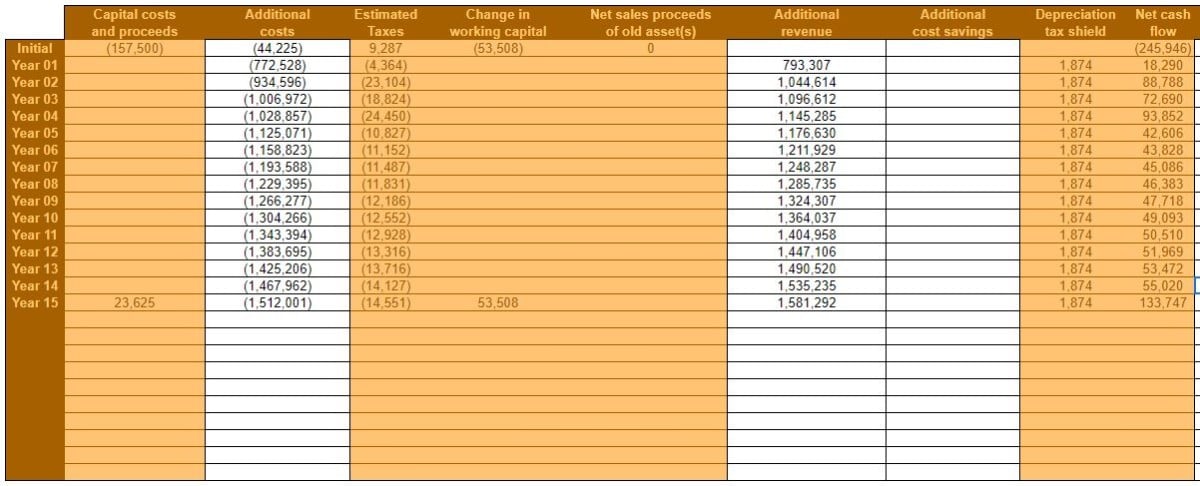

Click to enlarge

Initial Additional costs include launch costs that can’t be depreciated. E.g. professional services, organization & development costs, and other pre-opening costs.

Additional costs for Year 01 through Year 05 are pulled directly from the operating budget. Additional costs for Year 06 through Year 15 are assumed to grow at a rate of 3% per year after Year 05.

Additional revenue for Year 01 through Year 05 is also pulled directly from the operating budget. Additional revenue for Year 06 through Year 15 is assumed to grow at 3% per year after Year 05.

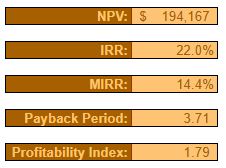

Over the course of fifteen years, the Summary of the capital budget shows:

Net present value (NPV) of $194,167

Internal rate of return (IRR) of 22%

Modified internal rate of return (MIRR) of 14.4%

Payback period of 3.71 years

Profitability index of 1.79

It’s worth noting that if the restaurant were to be sold at the end of fifteen years, the NPV would be considerably higher – accounting for the proceeds from a sale.

Startup restaurant operating budget

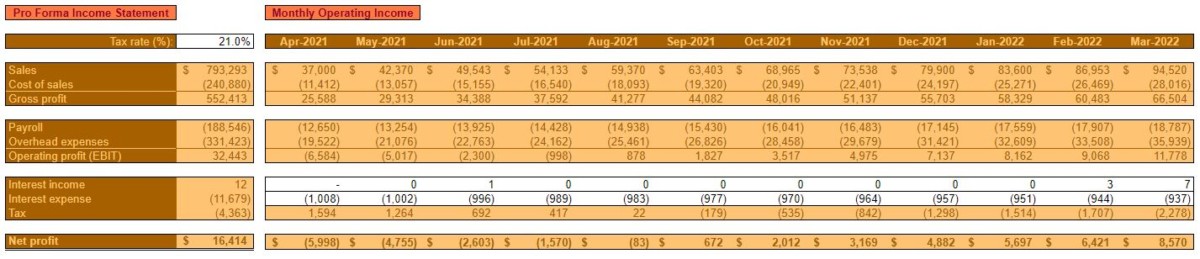

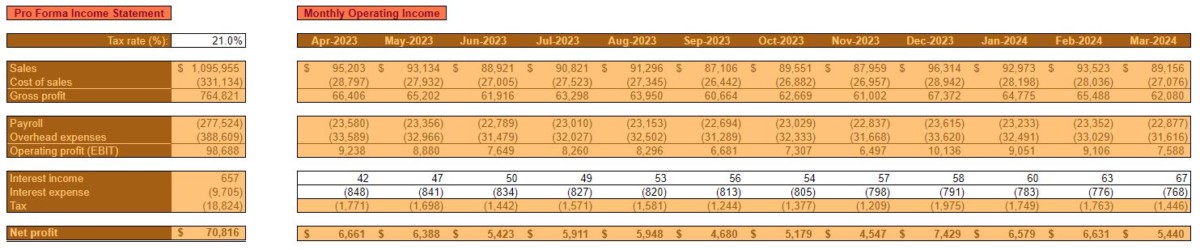

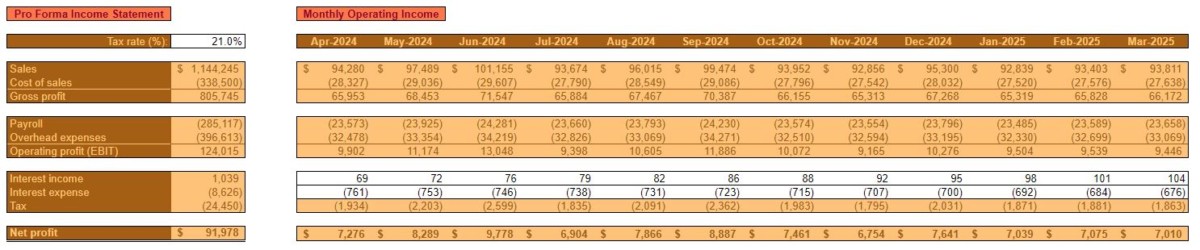

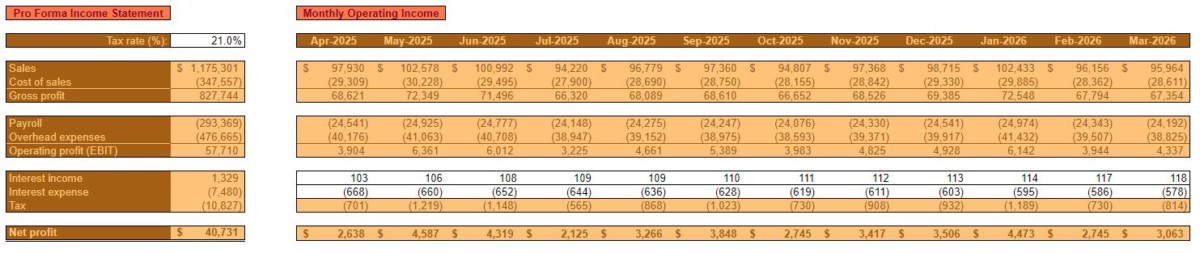

In the operating budget, Diner, LLC.’s sales, ingredients (cost of sales) payroll, and other overhead expenses are forecasted by month. Additionally, annual amounts are shown in a Pro Forma Income Statement. Each individual component of the budget is analyzed and forecasted separately in an attempt to be as comprehensive and realistic as possible.

Restaurant operating budget Year 1

Click to enlarge

Year one of operations is characterized by low initial sales that grow quickly throughout the first 12 months of business. The first month of profitability is estimated to be Month six – September 2021.

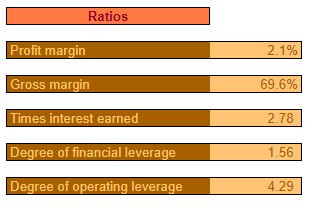

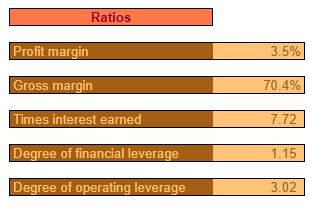

As such, the Profit margin is very low for the year overall but, it is expected that the year will be profitable.

Click to enlarge

The Sales Budget breaks down the expected Unit volume and Dollar Sales for each category of products sold. These categories are:

Entrées

Appetizers

Desserts

Non-alcoholic beverages

Alcoholic beverages

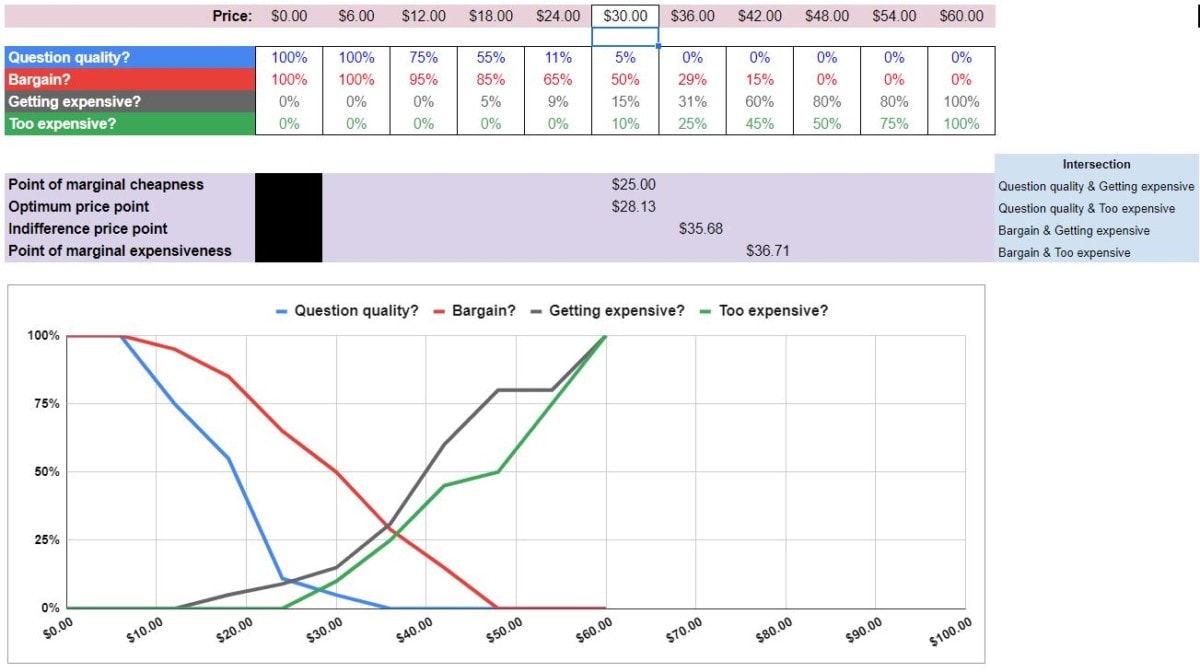

Each individual product in a category will have a different price, of course. However, for the sake of simplicity, items were grouped by category and an average Sales Price is estimated.

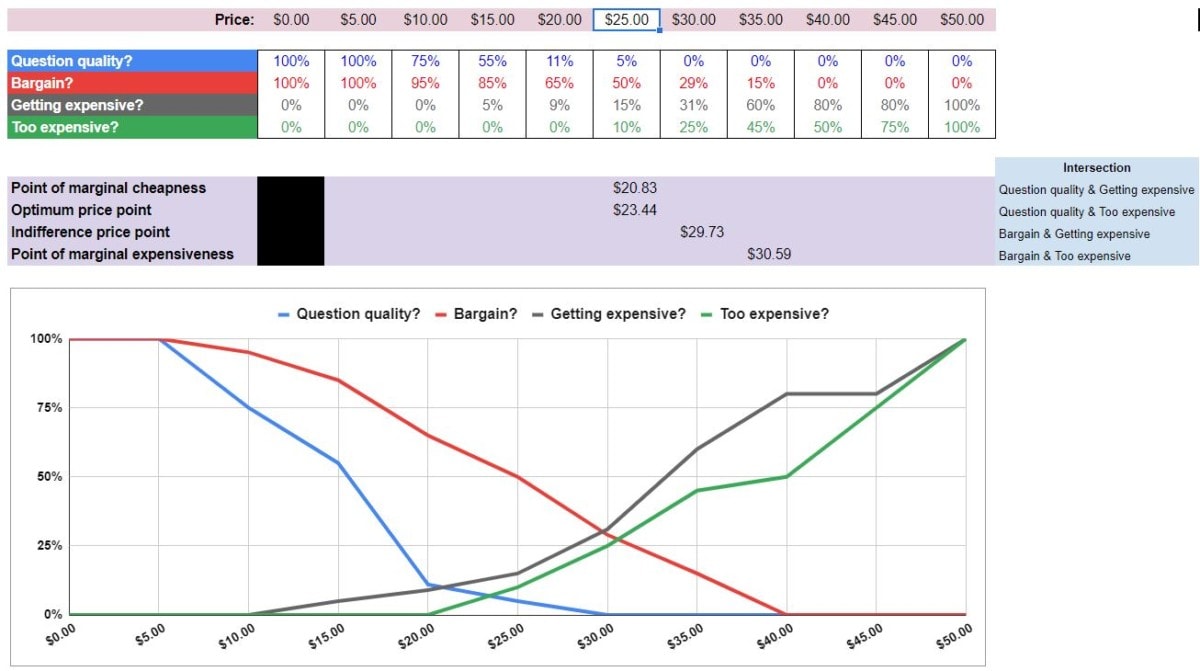

Sales prices will initially be set higher than average. At or near the “indifference price point.” At this price point, the number of customers that consider the price a bargain should be close to the number that feel it’s starting to get expensive.

This is done with the hopes that the Diner, LLC.’s novelty, image, and quality will still provide a perceived value for customers. Additionally, pricing as high as practical will help to offset the low initial Unit Sales after launch.

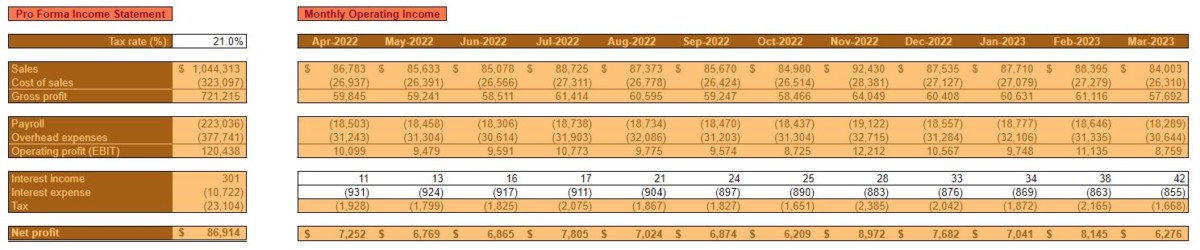

Restaurant operating budget year 2

Click to enlarge

Year two of operations is characterized by a leveling off of Unit Sales after reaching near practical capacity at the end of year one.

Additionally, it’s anticipated that Sales Prices will remain the same throughout the year after being on the high side in year one.

However, in spite of rising costs, overall sales are expected to increase significantly due to consistent demand throughout year two.

Click to enlarge

As mentioned, most costs, including ingredients, are expected to increase by an average of 3% in the second year.

As with sales categories, for the sake of simplicity, ingredients are grouped together into categories. Their costs represent an average of all the ingredients contained in a category.

Restaurant operating budget Year 3

Click to enlarge

In year three, unit sales are expected to continue to remain level. Sales Prices are anticipated to increase by approximately 5% to offset increased costs. Diner, LLC. is expected to have its highest year of profitability yet.

Click to enlarge

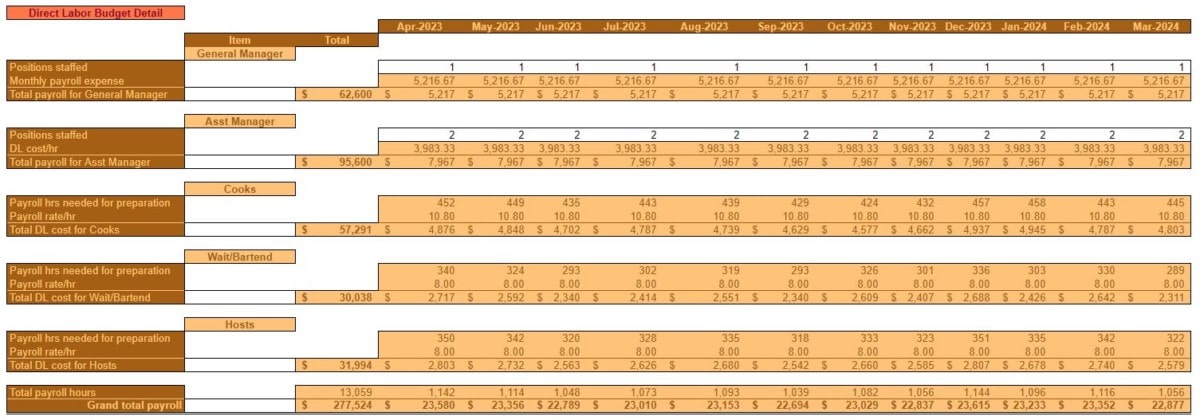

As was the case in year two, payroll is again expected to increase. This is due to an increase in wages and salaries of roughly 3%. It is Diner, LLC.’s intent to incentivize customer service and quality through above-average employee compensation.

In years one and two, the staff is expected to consist of:

One General Manager and one Assistant Manager, along with Cooks, Waitresses/Bartenders, and Hosts as needed, part-time, depending on sales volume. The General Manager and Assistant Manager are expected to cover any staffing shortcomings.

In year three, however, it is budgeted to add a second Assistant Manager position to relieve some of the responsibilities of the other managers.

Restaurant operating budget Year 4

Click to enlarge

With Unit Sales, for all practical reasons, expected to be maxed out, Sales Prices would need to be increased in year four in order to achieve meaningful revenue growth.

As is typical, all costs are expected to increase by 3%, on average, in year four.

One exception is the Rent/Occupancy expense. When operations are initiated, Diner, LLC. is expected to enter into a three-year lease. At the beginning of year four, the lease will have expired and a new lease will need to be signed. A 10% increase in Rent/Occupancy expense is anticipated.

Restaurant operating budget Year 5

Click to enlarge

By the end of year five, Diner, LLC. is expected to remain profitable. That is, as long as Sales Prices are kept adequately above costs without sacrificing demand.

In order for the Diner, LLC. to grow from this point, the opening of a new location or another type of expansion would need to take place.

Click to enlarge

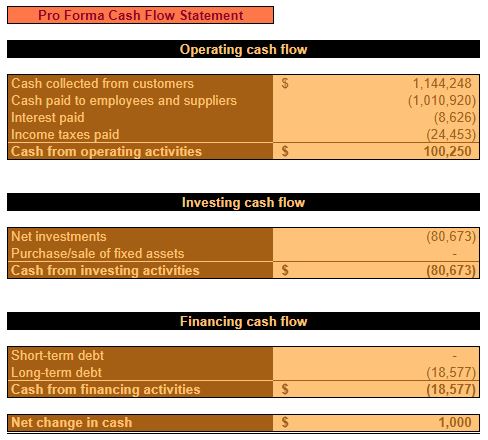

Startup restaurant cash budget

The cash budget forecasts the timing of cash collections and cash disbursements. This is done in an effort to ensure that Diner, LLC. remains solvent.

Obviously, the nature of the restaurants’ business model is such that cash collections are always made at the time of sale. So, no Accounts receivable are ever anticipated to be on the books.

However, ingredients, payroll, and overhead are not necessarily paid for in the same month but those expenses are incurred. Therefore, the timing of cash flow out will not necessarily correspond with expenses on the operating budget.

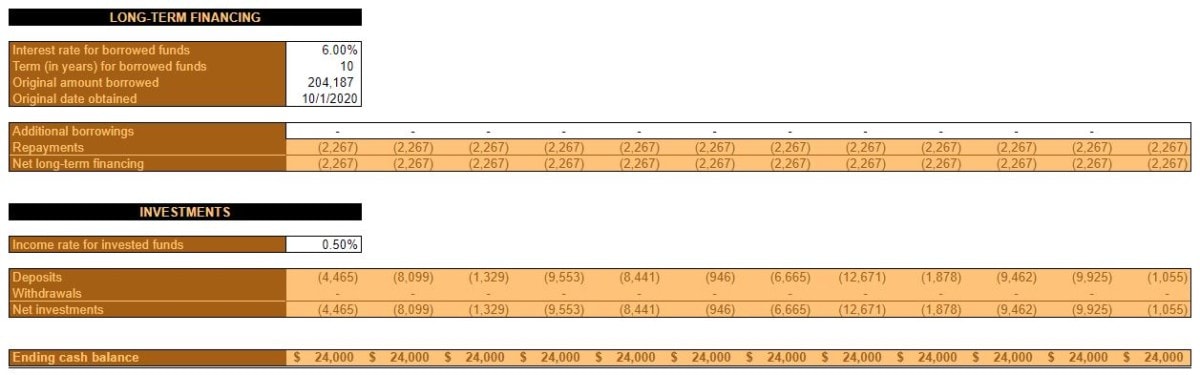

The cash budget is where a Desired ending cash balance is specified. Additionally, details on any financing (long-term and/or short-term) and savings account balances are also addressed.

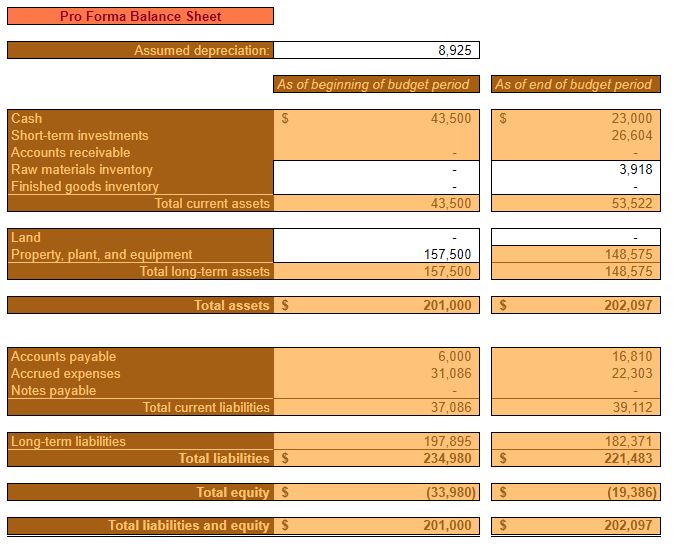

Restaurant cash budget Year 1

In the time leading up to the first month of operation, a considerable amount of money will need to be borrowed by Diner, LLC. to pay for pre-opening expenses. The Beginning cash balance is set at $43,500 in order to offset low initial sales.

Click to enlarge

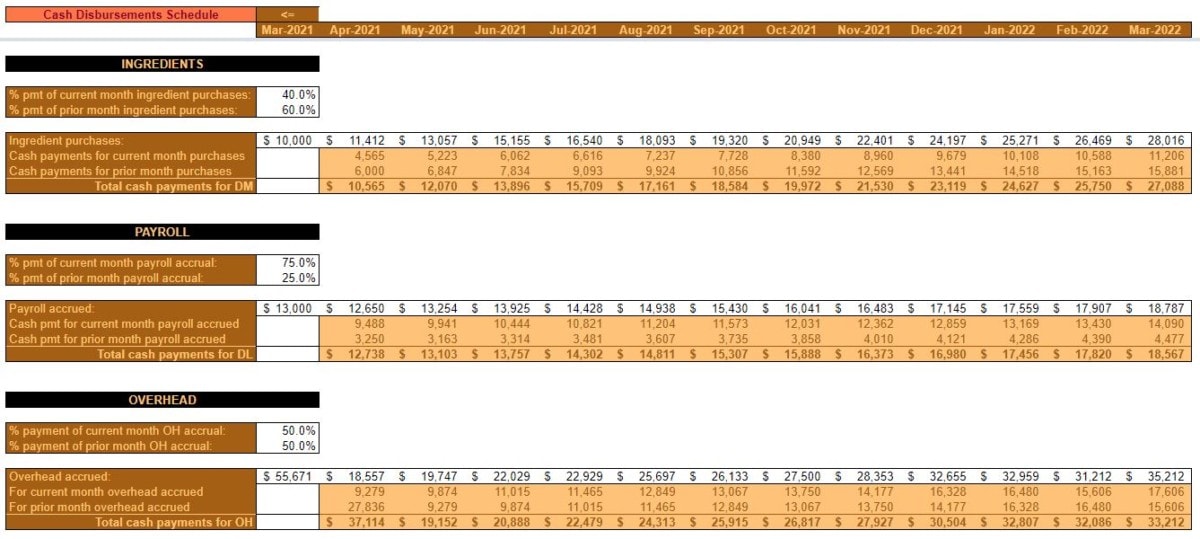

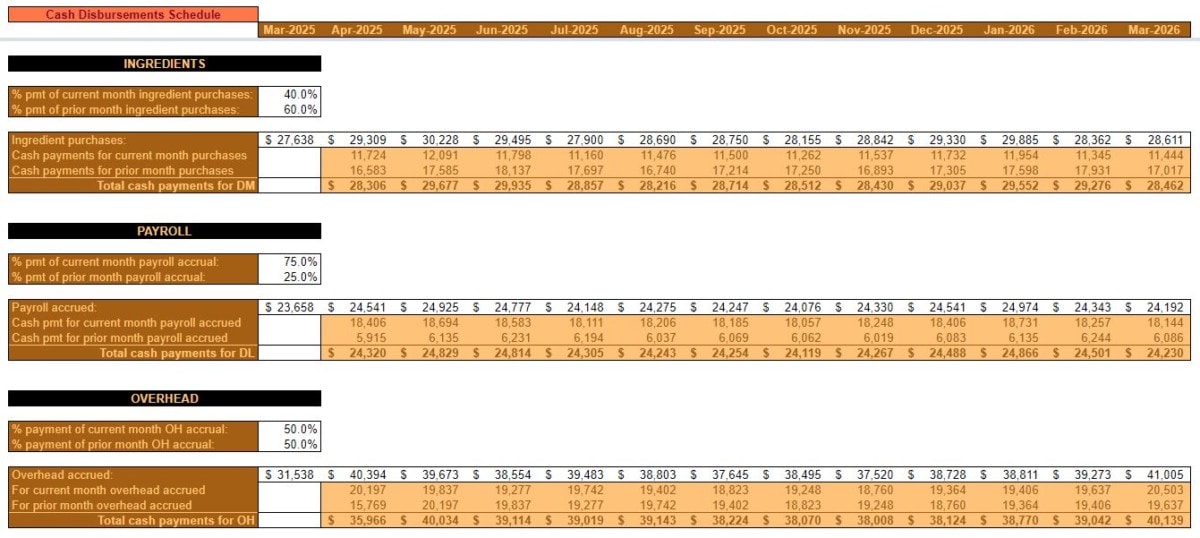

Pre-opening ingredient purchases, payroll, and overhead expenses are estimated and accounted for.

The timing of cash payments is estimated by assigning a % pmt of current (& prior) month for each expense type.

Restaurant cash budget Year 2

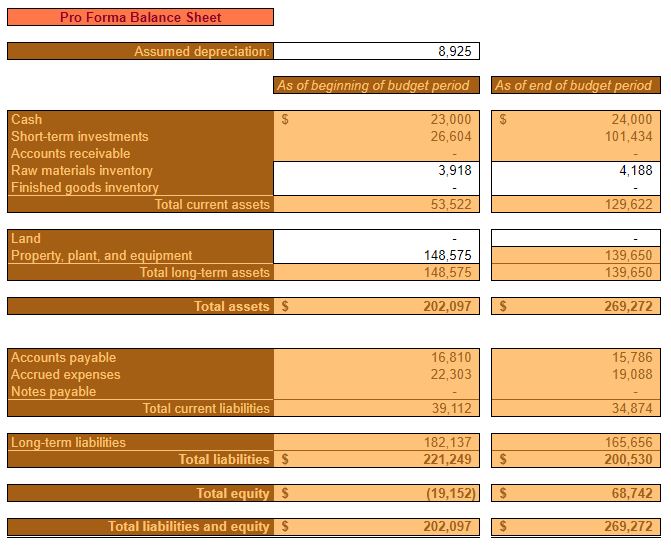

The increase in Unit Sales for year two is expected to help turn negative equity positive. Additionally, prudent cash management is expected to contribute to the security and solvency of Diner, LLC.

Click to enlarge

Maintaining an Ending cash balance of $24,000 every month puts the restaurant in a position where it doesn’t need to rely on any short-term or long-term financing. It also facilitates the ability to put excess cash into a liquid investment account. This investment account is available to offset negative, unforeseen, events. Or, to put towards future growth and expansion.

Restaurant cash budget Year 3

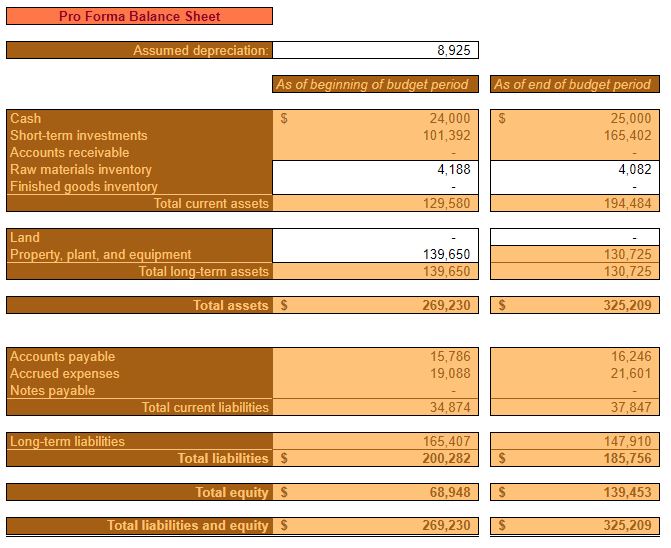

Year three is expected to see the continued reduction of debt and a subsequent increase in assets and equity. Certain balance sheet items like inventory, Accounts payable, and Accrued expenses are expected to increase in line with increasing costs as outlined in the operating budget.

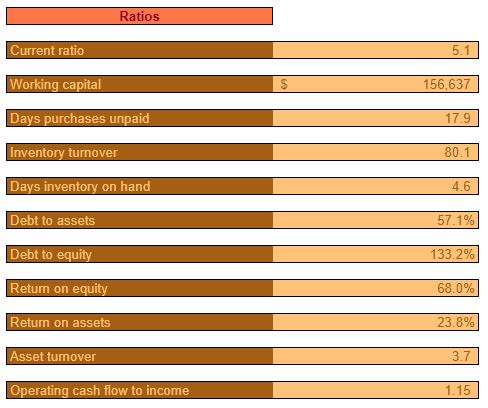

All ratios at the end of year three are expected to be relatively healthy. At this point, Diner, LLC. is expected to still have a relatively high Debt to equity ratio. This ratio is expected to continue to decrease, however.

Restaurant cash budget Year 4

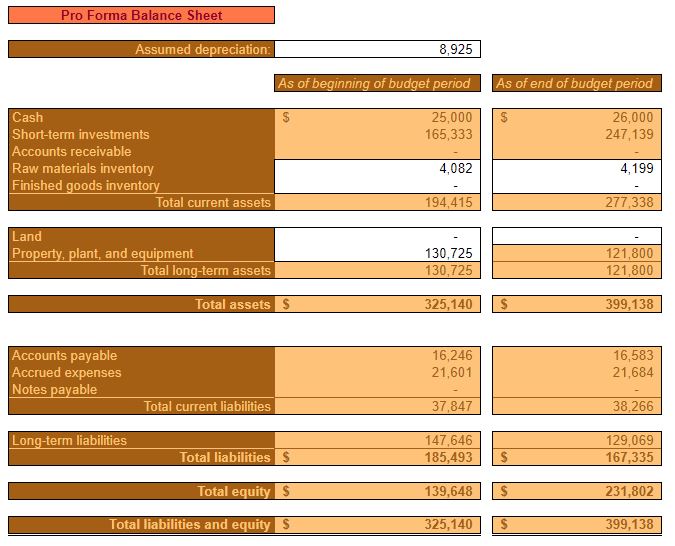

Throughout year four, assets and equity will continue to grow.

Cash and short-term investments begin to make up a considerable portion of assets.

The year four pro forma cash flow statement offers a different perspective than the income statement and balance sheet. It shows how it’s anticipated to be cash positive from operating activities and how the majority of that cash will be used to pay down debt and put into a short-term investment account.

Restaurant cash budget Year 5

By the completion of the fifth year of operation, equity is estimated to be between $250,000 and $300,000. Cash balances continue to grow at approximately $1,000 per year, in order to account for increasing expenses.

Barring unforeseen events, Diner, LLC. should be expected to adequately cover expenses and to deposit a considerable amount of cash receipts into short-term investments.

This growing investment account will serve as a margin of safety for unforeseen circumstances and/or will allow for expansion or other projects – should that course of action be chosen.

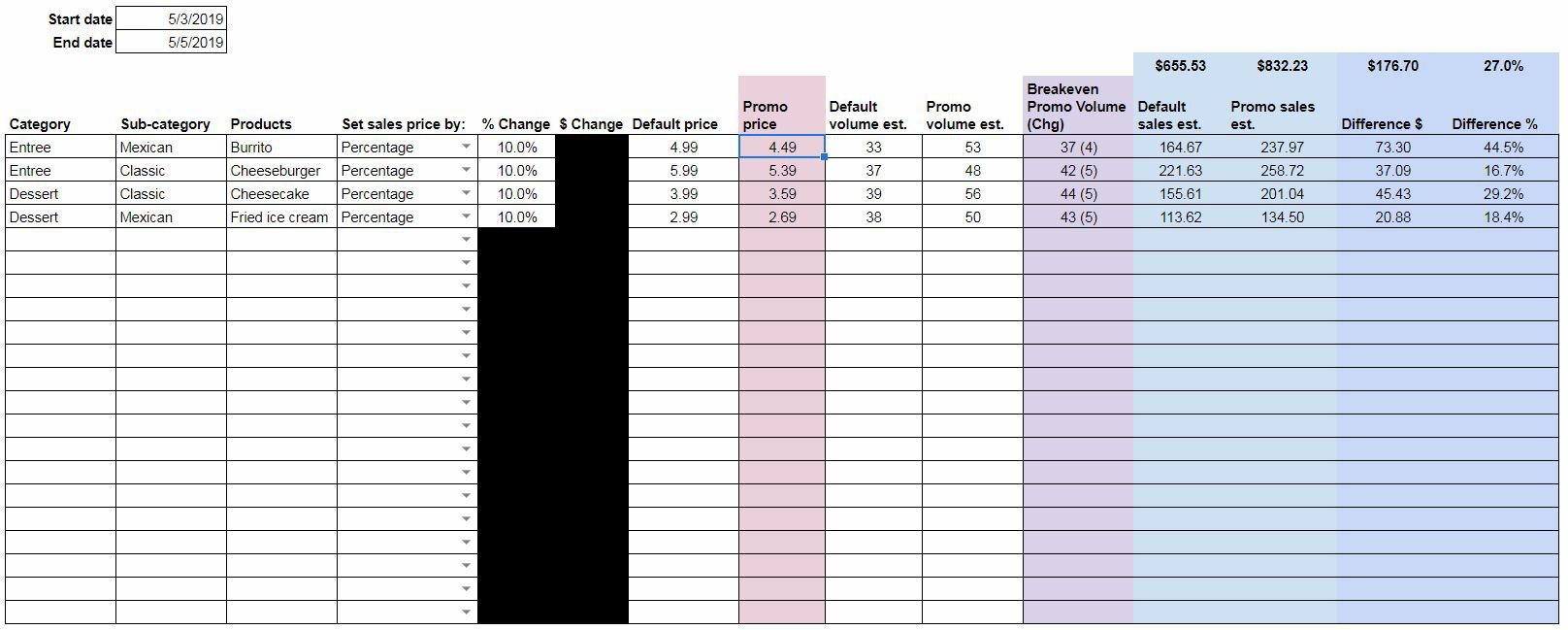

*pricing strategy example at the bottom of this post

Download the Price Sensitivity Meter

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

Video transcript