“Can I get an SBA loan with no credit?” Unfortunately, you cannot. But, there are other options available to start a business with no credit. Not every option is practical for every entrepreneur. Plus, each has its pros and cons. However, if you want to start a business and have no credit history, you should read further about your options.

To be clear, what follows is options for starting a business with no credit.

There are more options available for businesses that are already operating. Those are covered at the end of the post.

Here’s a summary of the options for getting a startup loan with no credit. Each is covered in more detail below.

“No-credit” loan option

Pros

Cons

Small business grants

Don’t require repayment

Limited availability

Microloans

Quick approval

Typically only available for “underprivileged” groups

Friends & family

Lenders who know you well

Potential to damage relationships

Get a co-signor

Can help establish credit

Co-signor is responsible if you don’t pay

Business credit cards

Easy to obtain

Need personal credit history

Crowdfunding

No repayment necessary

Typically only available for B2C businesses

Small Business Grants

Grants can come from anywhere, so requirements can vary widely. However, credit history is not typically a requirement.

Another benefit of grants, of course, is that they do not require repayment.

No credit history and no repayment? Sounds like a hell of a deal, right? Well, the catch is that grants are typically stringent in their requirements. Plus, there’s typically a lot of competition.

However, free money to start your business is a great thing. So, it doesn’t hurt to spend a little time researching grants that your business might be eligible for.

Microloans are often made by nonprofit organizations. Therefore, they are not as concerned with credit history or worthiness as a traditional financial institution.

So, what’s the catch? Microloans are typically only given to “disadvantaged” borrowers. Certain races, genders, etc. Therefore, if you’re a white male, you’re likely excluded from eligibility for most microloans.

Friends and Family

Friends and family are a potential source of financing to start your business if you have no credit history.

Friends and family know your character. Therefore, assuming your character is good, the chore is to convince them of the viability of your startup. To do this, you’ll need a good business plan.

Blood and money don’t mix. That’s how the saying goes. The reason is that it can damage relationships with your friends and family. That might be too high of a price to pay. So, move forward carefully.

Find a Cosigner

If your time horizon is long enough, you can build credit by taking out a loan and asking someone to cosign with you. A cosigner increases the likelihood of approval.

Consistent, on-time repayment of the loan will help build your credit. Solid credit history will help you get a loan to start a business – someday.

In fact, depending on the nature of your business, you could technically use a cosigner to get a loan to start your business right now.

For instance, if you are buying a piece of equipment, or vehicle, or some other asset that serves as the foundation of your business. Something that makes for good collateral. It’s possible, with a cosigner, that you could take out a loan for that equipment – and then be in business.

Business Credit Cards

I hesitated to include this option because I don’t want it to come off as deceptive. It’s splitting hairs and a matter of interpretation. It depends on whether you or your business, have no credit history.

You can fund your business with a business credit card. If your business has no credit history.

However, you will almost certainly need a personal credit history in order to get a business credit card.

Crowdfunding

Most crowdfunding isn’t a loan. But, it can be a different means to the same end.

Indiegogo, Kickstarter, and GoFundMe are examples of crowdfunding.

Generally, business-to-consumer (B2C) companies have more success with crowdfunding than business-to-business (B2B) with crowdfunding.

Typically, repayment isn’t required for crowdfunding. There are three types of crowdfunding that do not require repayment. These are:

Donation-based

Donation-based crowdfunding is where supporters give money without any expectation. Typically, this is reserved for people in need.

Therefore if you want to pursue this avenue, your business had better serve a critical need for society.

Equity-based

Equity-based crowdfunding is a situation where people who contribute to your company also become owners. Their expectation is to earn a return on their contribution. Just as a shareholder in a publicly traded company would.

Rewards-based

With rewards-based crowdfunding, you promise supporters a product or service in return for their contribution.

No-credit options for established businesses

Below, are some other frequently-cited options for getting a business loan with no credit. However, they are only going to be available for existing businesses. These are not loans you can get to start a business.

Nevertheless, I include them because they could be viable options for financing in the future, as your business grows.

PayPal Working Capital

As you might’ve guessed, this is only an option if you process payments via PayPal.

You must have a 90-day history with and a PayPal Business or Premier account. Additionally, you must process up to $20,000 annually through PayPal.

A PayPal Working Capital loan is paid back by PayPal taking a little bit of each subsequent sale that you make through PayPal.

Invoice factoring

Fundbox and Bluevine are examples of invoice factoring.

Invoice factoring is also known as factoring accounts receivable (AR). Invoice factoring is where you use your AR as collateral for a loan. So, obviously, you have to be in business, making sales, in order to have accounts receivable.

“Do you need to get a business loan for your startup?” No. But many startups will choose to secure a loan to start their business. Why? Primarily because most entrepreneurs don’t have the means to finance 100% of their startup. Also, equity financing is typically only available for high-growth businesses.

Debt vs equity financing for startups

Most startups need financial help from outside sources. These sources of financing fall into two general categories:

Debt

Equity

Debt financing

Debt is borrowed money that must be repaid according to an agreed-upon schedule and at an agreed-upon cost (interest rate).

One of the advantages of debt is that you don’t give up any ownership of your business. All the lender is concerned about is receiving regular repayment plus interest.

Once the loan is paid off the relationship with the lender ends.

Additionally, interest is tax-deductible. It is subtracted from operating profit before taxes are calculated.

Finally, debt repayment is predictable. It’s an easy expense to forecast.

That’s also one of the disadvantages, though. Debt is a fixed cost.

If the proceeds from debt aren’t used in a manner that earns a good return on investment (in terms of revenue or reduced costs) then that fixed expense drags the business down. Whether times are good or bad the cost of debt stays the same.

Another downside of debt for startup financing is that you may have to personally guarantee repayment of the loan with your own personal assets.

Equity financing

Equity is ownership of the business. Unless you give someone else equity in your business, you will always have 100% ownership.

If you finance with equity, you give up a certain percentage of ownership of your business. I.e. profits and sales proceeds.

Equity has its advantages.

For starters, you are not obligated to repay equity financing. The outside investor should understand that risk

One disadvantage of equity is that your investors may not agree with your business decisions. Since they are owners, you’ll have to take their opinions on managing the business into consideration.

Investors can be bought out, but that can be expensive.

Types of loans for startup businesses

Not all startup business loans are the same. If you decide to secure a loan to start your business, you have several options.

Equipment financing loans

Loans for startup businesses have strict standards that must be met. If you call the loan by a different name, those standards might loosen.

Equipment financing loans are for buying equipment, machinery, and other fixed assets.

The equipment you purchase serves as collateral for the loan. Repayment is typically made in installments.

Business credit cards

In addition to providing financing, business credit cards can establish credit for your business.

It’s likely that you will have to “cosign” with your business (personally guarantee) before getting a business credit card.

Business credit cards also, often, come with generous rewards programs.

SBA loans

The Small Business Administration doesn’t lend to your business directly. They guarantee the loan to incentivize the lender.

SBA loans are, typically, more “paperwork-intensive” than other options.

SBA loans can also be made for larger amounts than some other alternatives.

Microlender loans

Microlenders are non-profit organizations that provide debt financing to startups who might not qualify with traditional lenders.

These loans are typically “smaller” than those made by a traditional financial institution.

P2P loans or crowdfunding

Peer-to-peer loans, currently, are only made to individuals. Not businesses.

P2P loans are also, typically, small. But, approval and funding are quick.

Loan crowdfunding, unlike other types of crowdfunding (donation, exchange, and equity), requires payback. It’s not dissimilar to P2P loans.

Friends and family loans

Borrowing from a friend or family member might be easier. But, it can come with other complications.

Make sure the terms of the friend/family loan are clear.

Obtaining a startup business loan

If you’ve decided to secure a loan for your startup, these are, more or less, the steps you’ll follow to get funding:

Keep in mind the fixed assets you’ll need to launch.

Also, money that will need to be spent before operations commence.

Additionally, your small business will need cash-on-hand at launch

Work in an additional amount for unanticipated expenses you might incur before your business becomes self-sufficient.

2) Decide what type(s) of startup business loan you want

Review Types of loans for startup businesses, above, and choose one or more that suits your business’s needs.

3) Compare loan providers

Several different providers should be available for whatever type of loan you seek for your startup.

Compare costs, terms, credit requirements, collateral required, documentation, business requirements, and other variables between providers. A table with the providers in the left column and the variables along the top might help you compare.

Look up and compare reviews for providers, too.

APR

Loan term

Credit req

Collat needed

Docs needed

Biz req

Reviews

Provider 1

Provider 2

Provider 3

4) Assemble the needed documentation

Every type of startup business loan will require at least some type of documentation.

Common types include a business plan, historical financial statements, personal & business bank statements, personal & business tax returns, legal documents (leases, contracts, etc). Be prepared to provide more documentation. This should get the ball rolling, though.

5) Complete the application process

Each type of startup business loan will have its own unique application process.

You can apply with more than one provider at a time. This could help you secure a loan quicker. Beware of the effect of multiple inquiries on your credit score, though.

What factors can get your startup business loan application declined?

Not every loan gets approved. In fact, a lot of startup business loan applications get declined. Don’t despair.

If you do get rejected for a loan try to get an authentic reason why. Rejection sucks. But, understanding your shortcomings can help make it clear what you need to work on.

Here are some areas to address, before you apply, to minimize your chances of rejection.

Low credit score

Lenders aren’t visionaries. They rely heavily on the mysterious algorithm known as a credit score.

If your (or your business’s) credit score is too low, you’ll be systematically dismissed. Work to get your credit score to the minimum needed for the type of loan you’re seeking.

Lack of credit history

This can affect your credit score.

If you have no credit history, then, in most lender’s eyes, you have bad credit.

Fortunately, it doesn’t take too long to build a credit history. If you do so with on-time payments, a lot of your credit issues should disappear.

A high-risk industry

Lenders want to minimize risks.

If they deem your industry (or business model) high-risk, they will likely decline your loan application. If they don’t understand your industry (or business model), they’ll probably deem it high-risk and decline your loan application.

If you find yourself in this position more thorough market research might help. Plus, you might search for a lender that specializes in your particular industry.

Character issues

A criminal history and/or a bad reputation can result in a declined loan application.

Conviction of a crime involving “moral turpitude” is likely an instant rejection. If you’re unsure, you can speak with a representative of the lender to gauge their stance on your crime.

Infamy as a particularly immoral person, even if not criminal, isn’t going to help your cause either. In instances like this, you’ll likely have to apply somewhere your reputation doesn’t proceed you.

Lack of collateral

Collateral lowers risk for lenders. If things go bad, they can sell the collateral and recoup some of their losses.

However, if you’re securing a startup loan to pay for things like labor, marketing, or research, then there is nothing tangible for them to sell if you default on the loan. Therefore, they’ll see the loan as riskier and the likelihood of your business getting declined increases.

Capacity to repay

Low margins, a poor location, and many other factors can make your financial projections suspect in a lender’s eyes.

Even if you can show that it is possible for you to pay back the loan, that possibility might be based on so many shaky assumptions that the risk is too high to make a startup loan to your small business.

A poor business plan

A well-researched and thought-out business plan sends a strong message. It shows that you have carefully considered the present and future environment of your startup.

Beyond that, if it’s done right, it also serves as a marketing tool for the funding your startup needs to be successful. Every section of your business plan should make a case for loaning your small business the money it needs.

Lack of quality advice

Business is complicated.

It could be that your business is a good credit risk, but, you’re just not able to convey that to lenders. If that’s the case, check with your local SCORE chapter. There may be volunteers with that organization that can help you put your best foot forward.

Giving up

You’ll get declined for every loan you don’t apply for. Rejection can be discouraging, but try to take a lesson from it and make improvements where needed. Don’t keep banging your head against a wall.

Also, if you’re going to pitch your business, show some enthusiasm. Business revolves around selling and your startup’s potential is the first thing you have to sell. If you’re not pumped about your startup’s potential, then go back to the drawing board and refine it until you are.

Do you need to get a business loan for your startup?

It technically isn’t necessary to secure a loan to start a business. But, if you want to start a business, there’s a pretty high likelihood that you’ll need one.

Understanding your options and the loan process will help you decide what kind of debt financing is right for you. It will also help you to be prepared and increase the chances of your approval.

Intuit, the creator of QBO, offers an extensive catalog of lessons on the use of their software. There are also plenty of free resources available in video and print from 3rd parties.

If you’d like a more intensive/personalized experience, courses and classes are an option. But, they are not typically free.

You’ll notice that I tried to gather some simple stats regarding each training option. Some information to help you decide what’s best for you. The navigation rating is my opinion on how easy it is to search the training topics in order to find what you’re looking for.

No guarantee is made regarding stats on QuickBooks training. It’s all subject to change. However, the information is reasonably accurate as of October 2020.

I’ve created some QuickBooks Online training myself. With it, I always strived to be comprehensive yet to the point. If you’d like to check that out, you can do so here:

Cost: $0 Format(s): Video Number of lessons: approx 135 Typical format length: 17:45 Navigation: 3.0/5.0

Hector’s videos are very helpful and comprehensive. I’ve referred to them several times in the past.

Because they’re comprehensive, they’re a little on the longer side. The shortest is about 6:30 and the longest is nearly 30 minutes.

Since his videos are on YouTube, it can be a little tough to find what you’re looking for. His Playlists are not terribly descriptive.

He has 102K subscribers and his videos are very well-reviewed. You’ll typically find Hector in the top five results for any subject you search related to QuickBooks Online.

Cost: $0 Format(s): Video Number of lessons: approx 36 Typical format length: 5:15 Navigation: 3.0/5.0

I’m not as familiar with BookkeepingMaster. He has, however, 70K subscribers.

His videos are shorter and he doesn’t cover the breadth of topics some of the other YouTubers do. Videos typically run from 3:30 to a little over 7 minutes.

I believe he is British. Which gives him an air of dignity.

It also means that he uses the British version of QuickBooks Online. I don’t know for sure, but there could be discrepancies in the technical accounting. The currency is obviously different. Other than that, the fundamentals should be the same.

Cost: $0 Format(s): Print Number of tutorials: approx 50 Typical format length: 900 words Navigation: 1.0/5.0

This is not a great option, in my opinion.

Many of the results from searching for “QuickBooks Online” are for QuickBooks Desktop with the word “online” worked into the post somewhere. To be fair, it’s a distinction that Google hasn’t been able to make yet.

Also, you can’t skip pages to find what you need; you just need to keep pressing “Older” or “Newer.”

Dummies does have a unique take on some topics that I didn’t see with any of the other options.

Yes. Early this year, Intuit announced that outdated versions of QuickBooks Desktop were to be discontinued.

Come June 1, 2021; the company ended all access to add-on services on its Windows 2018 desktop edition. It included older versions of the accounting program, such as Pro, Premier, and Enterprise Solutions of QuickBooks Desktop 2018.

Right after May 31, 2021, users no longer had access to certain features of QuickBooks Desktop 2018, such as Payroll, Live Support, Online Banking, Online Backup, and other services. And, as of June 1, 2021, they no longer received essential security updates.

Concurrently, on May 31, 2021, certain products were also effectively phased out:

2018 QuickBooks Desktop Pro

QuickBooks Premier Desktop 2018

Premier Accountant Edition 2018

Enterprise Solutions for QuickBooks 2018

Right after, on February 2, 2021, other products were also phased out.

Payments services in QuickBooks Desktop Point of Sale 12.0

What happens to my software and data, do I need to upgrade?

If you were not subscribed to any QuickBooks Desktop 2018 add-on services, your software should continue to function normally. However, you will no longer have access to live technical support or other Intuit services that work with QuickBooks Desktop.

It’s highly recommended to upgrade to the most recent version of the QuickBooks Desktop to receive all of the product’s features and support. Alternatively, you can also convert to QuickBooks Online.

What happens when I upgrade?

You’ll be prompted to convert your company file so that it will function properly with your new QuickBooks. QB takes great care to protect your information during this procedure. And most importantly, before they do anything, they verify the integrity of your data file and create a backup.

List of other products that are fully operational and available for users:

2021, 2020, 2019 QuickBooks Desktop Pro and Premier

How long does it take before the upgrade is completed?

Usually, It takes less than an hour, but the larger your file is, the longer it’ll take. You’ll be required to activate QuickBooks Desktop 2021 or QuickBooks for Mac 2021 when you install it.

The funding request section of the business plan is where you bring together everything else you laid out in the previous sections.

Those other sections stated why your business will be successful and how successful it will be. But, the funding request section is where you communicate how much help you’ll need to be successful. Beyond that, it shows why your burgeoning small business is a good investment.

The funding request section relies heavily on the startup’s financial projections. Therefore, in this funding request example, I will refer to the same hypothetical business as I did in the example financial projections – a restaurant startup called Diner, LLC.

As a reminder, in the financial projections example, forecasted a capital budget, five years of operating budgets, and five years of financial budgets to lay the groundwork for this funding request. Therefore, I won’t include the actual financial projections in this example so as to not be redundant.

This example funding request, like the example financial projections, is built off of these two previous posts:

As outlined in the financial projections section, Diner LLC. is expected to achieve profitability quickly – within its first year of operation. Furthermore, it’s expected to continue to increase in financial health for the foreseeable future. Diner, LLC. respresents a prudent investment for small business lenders.

In order to realize it’s potential, outside funding is required.

Total pre-launch cash expenditures are estimated at $255,233.

Mr. Restaurantmanager, the sole-member of Diner, LLC. is committing $51,047 (20%) of the total launch costs.

This leaves $204,187 (80%) in funding needed to launch this venture.

Funding details for startup restaurant costs.

Funding is requested in the form of debt financing only.

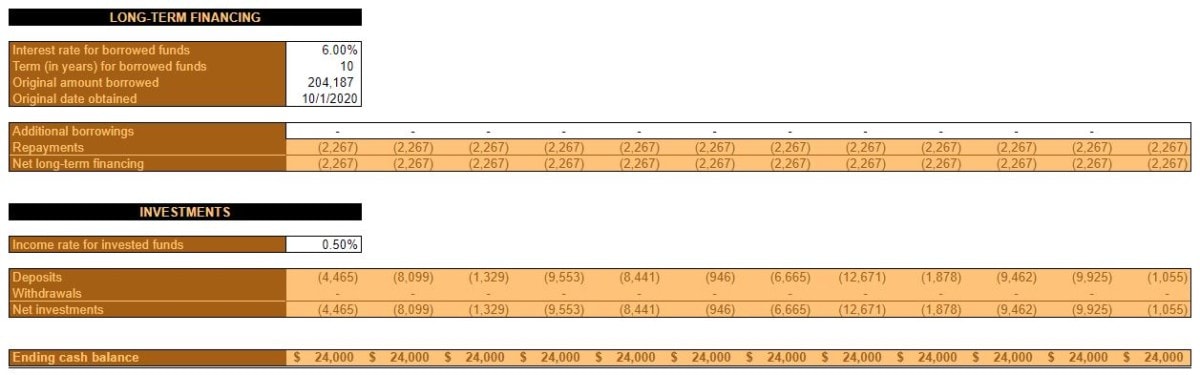

Ideally, these funds would be lent through the SBA 7(a) Small Loan program at or near a rate of 6.00% APR. This is representative of the current terms of the prime rate (3.25%) + 2.75%.

The term of the debt financing is expected to be 10 years and to be repaid in 120 monthly installments of approximately $2,266.89.

No outside equity financing is being sought at this time. Mr. Restaurantmanager would remain the sole-member of Diner, LLC.

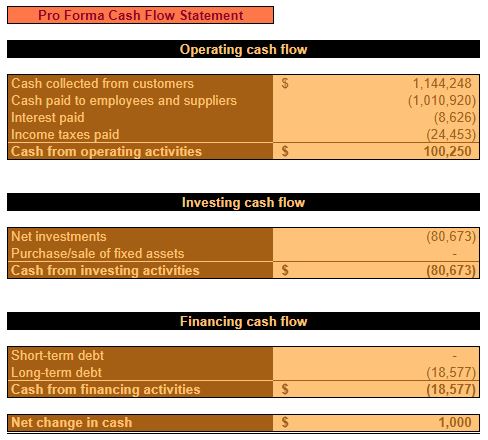

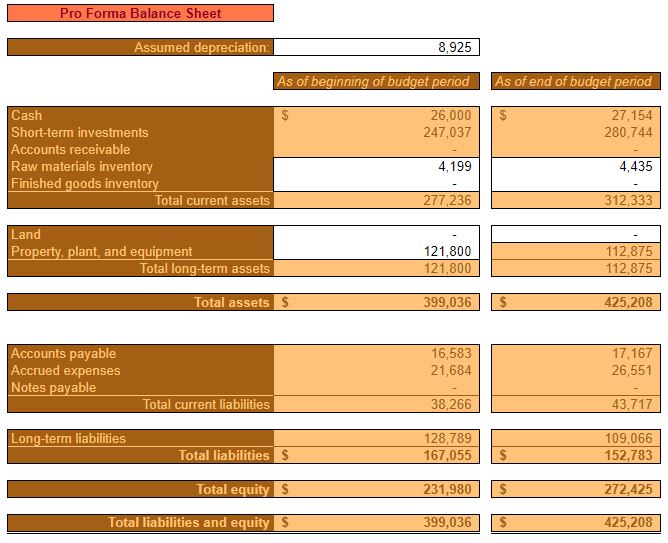

At the conclusion of the five-year financial projections, it is anticipated that the debt financing will be paid down to an approximate principal balance of $109,066.

At which point, it is undecided whether the business will be sold, expanded, or maintained as-is. With cash and other current assets anticipated to be valued at approximately $312,333, enough liquid capital will be available to pay the debt financing in its entirety – regardless of what course of action is chosen.

The financial projections section of your business plan is where you forecast your sales, expenses, cash flow, and capital projects for the first five years of your small business’s existence.

This is a critical section for readers of your business plan. It tells them:

How you expect your startup to perform financially

When you expect your new business to be profitable

How profitable you expect it to be

These are things you’d want to know as an investor, right? It’s up to the reader to decide whether they think your forecast is feasible.

Additionally, as an entrepreneur, it forces you to consider, thoroughly, what the first five years of business might look like. This will give you a good plan to work off of, will help you to be proactive, and will increase your likelihood of success.

Finally, the financial projections are the foundation of your funding request. Of course, your funding request, after all, is the primary purpose of your business plan.

Without knowing how much cash you need to launch and operate early-on, you won’t know how much you need to ask for. The funding request relies heavily upon financial projections, particularly the capital budget.

An example of a funding request, for this same business, will be posted separately.

This example of financial projections is built off of two previous posts:

Download the restaurant financial projections spreadsheet

If you’d like to download the spreadsheets I used to make these financial projections for a restaurant that can be done below. Keep in mind that these were (hastily) built off of budgets for a manufacturing company and tweaked for the restaurant industry. However, they should serve as a good starting point.

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

Startup restaurant financial projections

The financial projections for Diner, LLC provide a well-thought-out, cohesive, and comprehensive forecast of the restaurant’s performance from initial funding through the fifth year of operation. These forecasts will validate the feasibility of the concept and the appeal of an investment in this venture.

The financial projections for Diner, LLC include an initial capital budget for all of the fixed assets and other costs necessary to launch the restaurant.

Additionally, five years of pro forma income statements are included. These pro forma income statements are built off of a detailed five-year operating budget.

Furthermore, five years of pro forma balance sheets are also included. These pro forma balance sheets are built on five years of detailed cash flow analysis.

For the purpose of brevity, not every detailed budget is included in this business plan. However, all are available for decision support, upon request.

Items in italics represent those directly referenced in the financial projections.

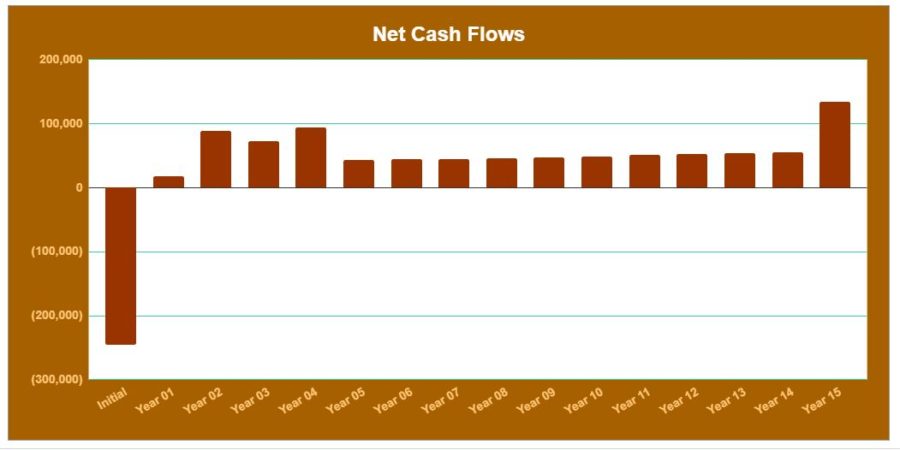

Startup restaurant capital budget

The capital budget summarizes Diner, LLC.’s forecasted operational and cash flow results over the next fifteen years. It takes into account:

Fixed assets needed to operate the restaurant

Launch costs necessary to begin operations

Cash-on-hand needed to launch the restaurant

To cover unanticipated expenses

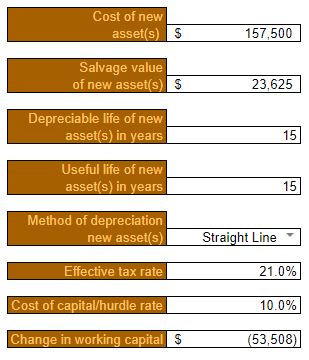

Fixed assets necessary to operate Diner, LLC. are estimated to cost $157,500.

The salvage value after fifteen years is estimated at $23,625.

On average, all assets are assumed to have a depreciable (and useful life) of fifteen years.

Fixed assets will be depreciated using the straight-line method.

The effective tax rate, for purposes of calculating a depreciation tax shield, is estimated at 21% throughout the capital budget.

A discount rate of 10% is used to calculate NPV and other capital budgeting metrics. This discount rate considers the cost of borrowing (6%) and adds an additional risk premium of 4%. 6% is the estimated interest rate for an SBA 7(a) Small Loan and is calculated by adding 2.75% to the current Prime Rate (3.25%).

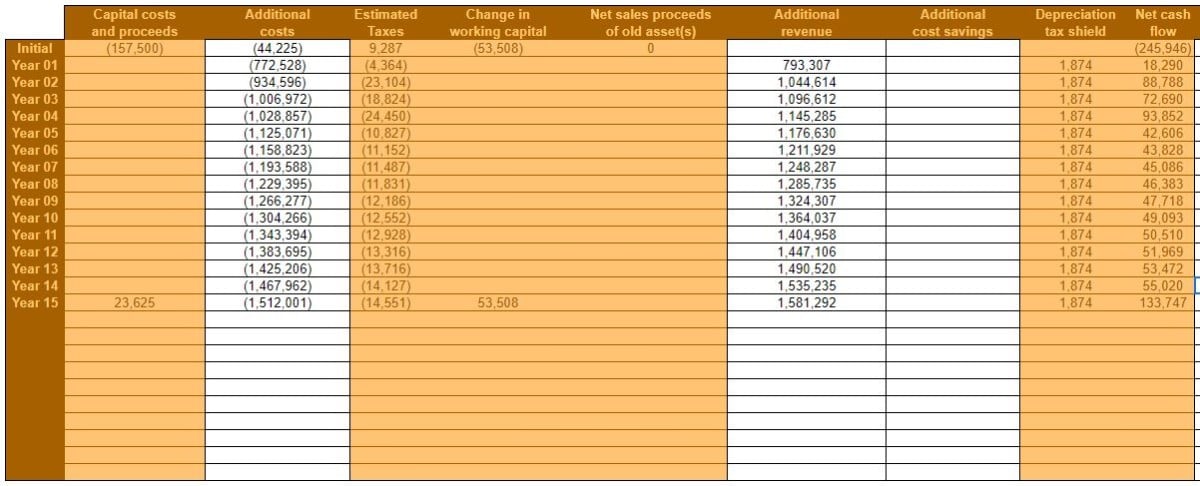

Click to enlarge

Initial Additional costs include launch costs that can’t be depreciated. E.g. professional services, organization & development costs, and other pre-opening costs.

Additional costs for Year 01 through Year 05 are pulled directly from the operating budget. Additional costs for Year 06 through Year 15 are assumed to grow at a rate of 3% per year after Year 05.

Additional revenue for Year 01 through Year 05 is also pulled directly from the operating budget. Additional revenue for Year 06 through Year 15 is assumed to grow at 3% per year after Year 05.

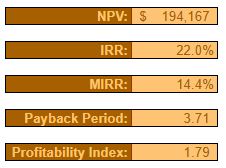

Over the course of fifteen years, the Summary of the capital budget shows:

Net present value (NPV) of $194,167

Internal rate of return (IRR) of 22%

Modified internal rate of return (MIRR) of 14.4%

Payback period of 3.71 years

Profitability index of 1.79

It’s worth noting that if the restaurant were to be sold at the end of fifteen years, the NPV would be considerably higher – accounting for the proceeds from a sale.

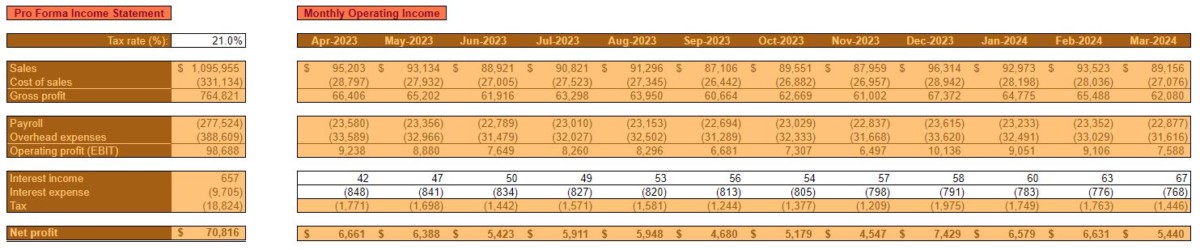

Startup restaurant operating budget

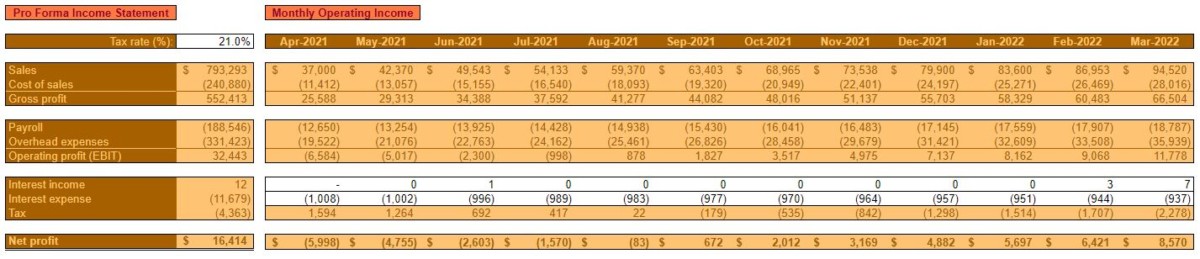

In the operating budget, Diner, LLC.’s sales, ingredients (cost of sales) payroll, and other overhead expenses are forecasted by month. Additionally, annual amounts are shown in a Pro Forma Income Statement. Each individual component of the budget is analyzed and forecasted separately in an attempt to be as comprehensive and realistic as possible.

Restaurant operating budget Year 1

Click to enlarge

Year one of operations is characterized by low initial sales that grow quickly throughout the first 12 months of business. The first month of profitability is estimated to be Month six – September 2021.

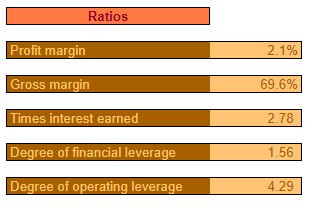

As such, the Profit margin is very low for the year overall but, it is expected that the year will be profitable.

Click to enlarge

The Sales Budget breaks down the expected Unit volume and Dollar Sales for each category of products sold. These categories are:

Entrées

Appetizers

Desserts

Non-alcoholic beverages

Alcoholic beverages

Each individual product in a category will have a different price, of course. However, for the sake of simplicity, items were grouped by category and an average Sales Price is estimated.

Sales prices will initially be set higher than average. At or near the “indifference price point.” At this price point, the number of customers that consider the price a bargain should be close to the number that feel it’s starting to get expensive.

This is done with the hopes that the Diner, LLC.’s novelty, image, and quality will still provide a perceived value for customers. Additionally, pricing as high as practical will help to offset the low initial Unit Sales after launch.

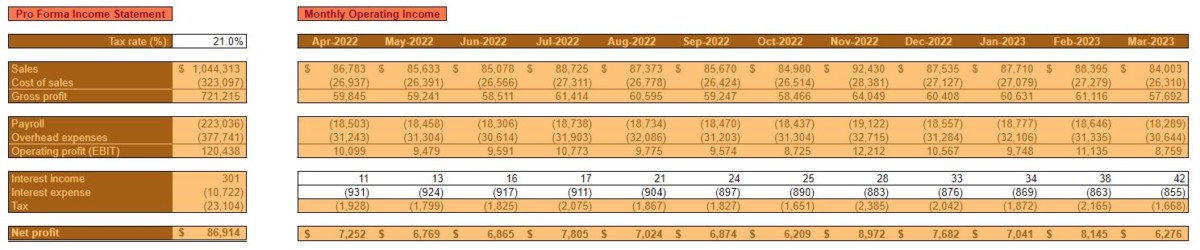

Restaurant operating budget year 2

Click to enlarge

Year two of operations is characterized by a leveling off of Unit Sales after reaching near practical capacity at the end of year one.

Additionally, it’s anticipated that Sales Prices will remain the same throughout the year after being on the high side in year one.

However, in spite of rising costs, overall sales are expected to increase significantly due to consistent demand throughout year two.

Click to enlarge

As mentioned, most costs, including ingredients, are expected to increase by an average of 3% in the second year.

As with sales categories, for the sake of simplicity, ingredients are grouped together into categories. Their costs represent an average of all the ingredients contained in a category.

Restaurant operating budget Year 3

Click to enlarge

In year three, unit sales are expected to continue to remain level. Sales Prices are anticipated to increase by approximately 5% to offset increased costs. Diner, LLC. is expected to have its highest year of profitability yet.

Click to enlarge

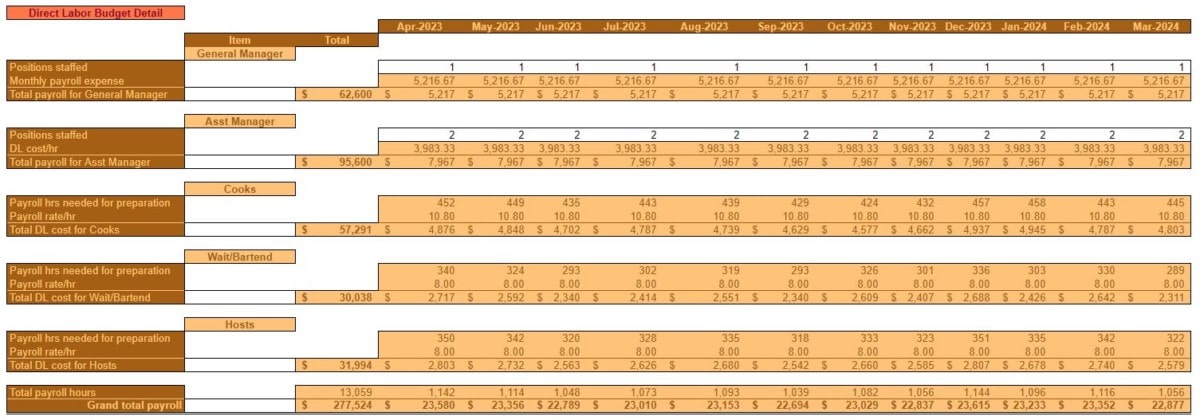

As was the case in year two, payroll is again expected to increase. This is due to an increase in wages and salaries of roughly 3%. It is Diner, LLC.’s intent to incentivize customer service and quality through above-average employee compensation.

In years one and two, the staff is expected to consist of:

One General Manager and one Assistant Manager, along with Cooks, Waitresses/Bartenders, and Hosts as needed, part-time, depending on sales volume. The General Manager and Assistant Manager are expected to cover any staffing shortcomings.

In year three, however, it is budgeted to add a second Assistant Manager position to relieve some of the responsibilities of the other managers.

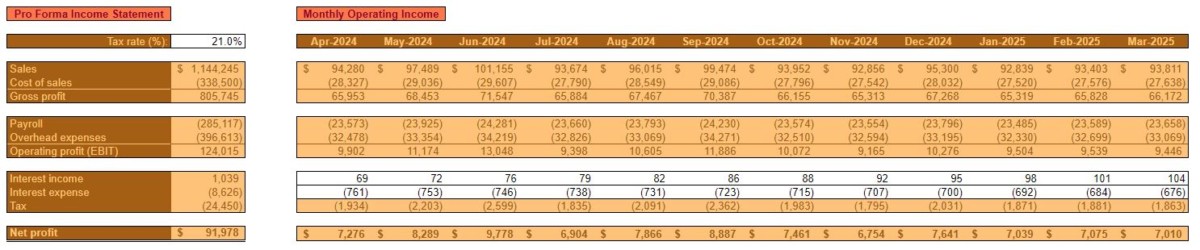

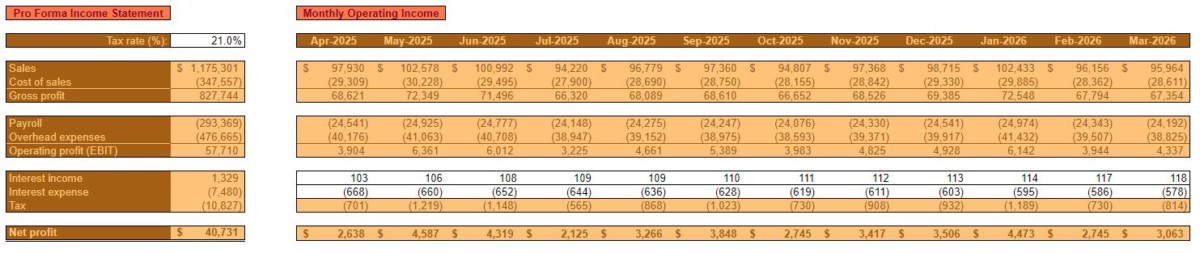

Restaurant operating budget Year 4

Click to enlarge

With Unit Sales, for all practical reasons, expected to be maxed out, Sales Prices would need to be increased in year four in order to achieve meaningful revenue growth.

As is typical, all costs are expected to increase by 3%, on average, in year four.

One exception is the Rent/Occupancy expense. When operations are initiated, Diner, LLC. is expected to enter into a three-year lease. At the beginning of year four, the lease will have expired and a new lease will need to be signed. A 10% increase in Rent/Occupancy expense is anticipated.

Restaurant operating budget Year 5

Click to enlarge

By the end of year five, Diner, LLC. is expected to remain profitable. That is, as long as Sales Prices are kept adequately above costs without sacrificing demand.

In order for the Diner, LLC. to grow from this point, the opening of a new location or another type of expansion would need to take place.

Click to enlarge

Startup restaurant cash budget

The cash budget forecasts the timing of cash collections and cash disbursements. This is done in an effort to ensure that Diner, LLC. remains solvent.

Obviously, the nature of the restaurants’ business model is such that cash collections are always made at the time of sale. So, no Accounts receivable are ever anticipated to be on the books.

However, ingredients, payroll, and overhead are not necessarily paid for in the same month but those expenses are incurred. Therefore, the timing of cash flow out will not necessarily correspond with expenses on the operating budget.

The cash budget is where a Desired ending cash balance is specified. Additionally, details on any financing (long-term and/or short-term) and savings account balances are also addressed.

Restaurant cash budget Year 1

In the time leading up to the first month of operation, a considerable amount of money will need to be borrowed by Diner, LLC. to pay for pre-opening expenses. The Beginning cash balance is set at $43,500 in order to offset low initial sales.

Click to enlarge

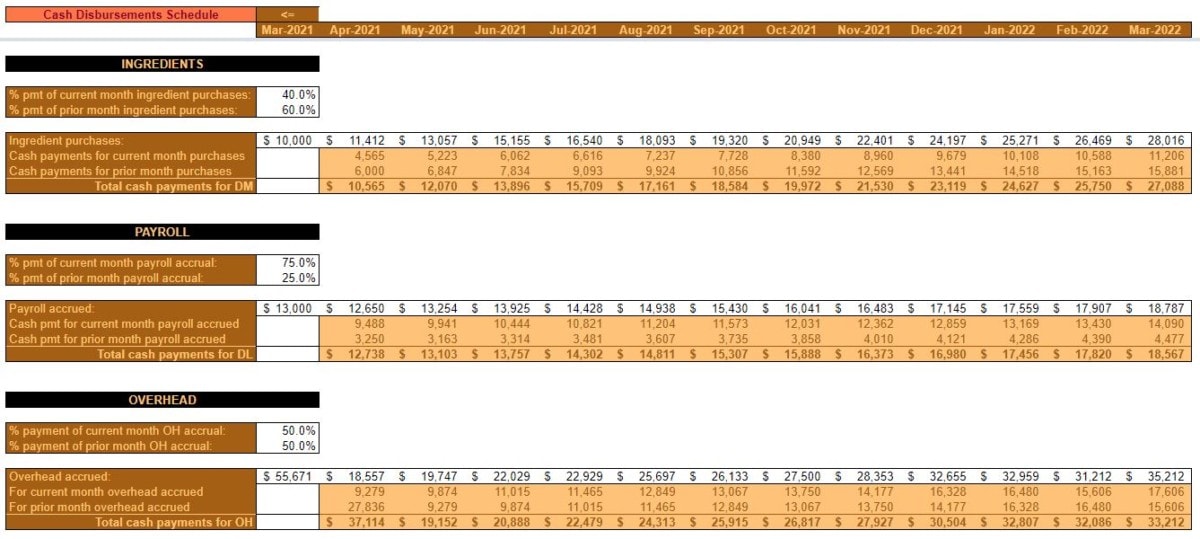

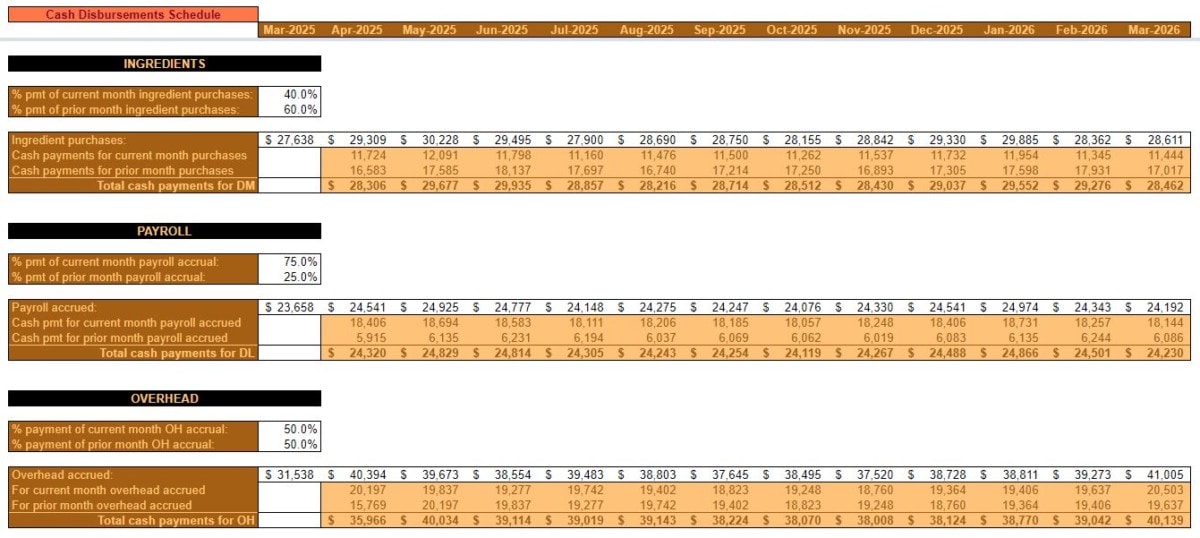

Pre-opening ingredient purchases, payroll, and overhead expenses are estimated and accounted for.

The timing of cash payments is estimated by assigning a % pmt of current (& prior) month for each expense type.

Restaurant cash budget Year 2

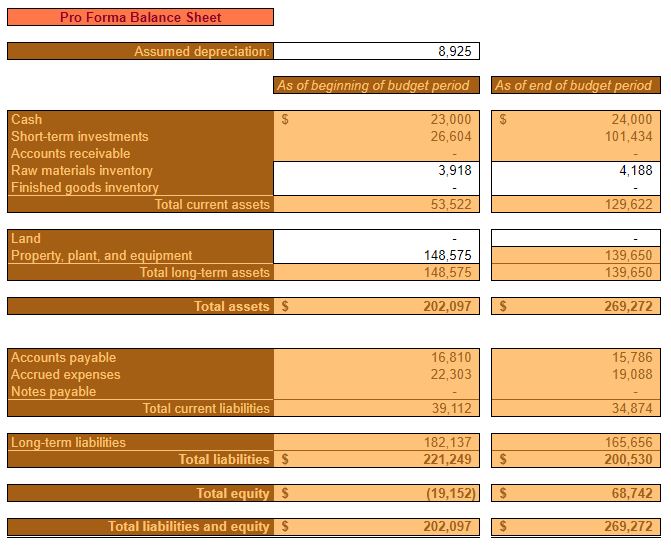

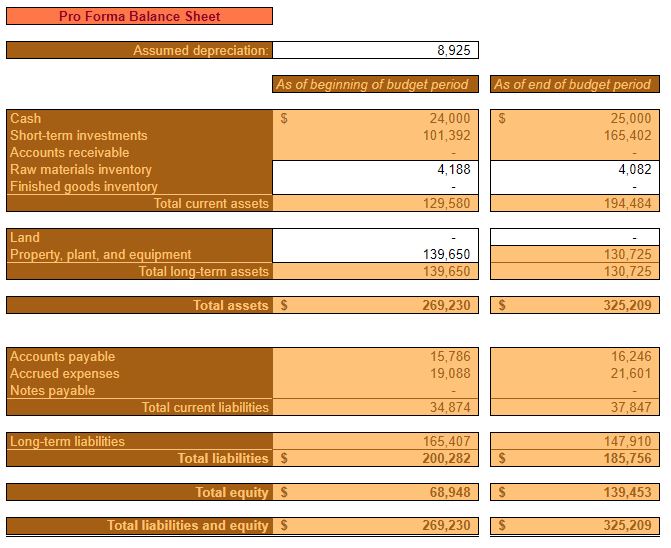

The increase in Unit Sales for year two is expected to help turn negative equity positive. Additionally, prudent cash management is expected to contribute to the security and solvency of Diner, LLC.

Click to enlarge

Maintaining an Ending cash balance of $24,000 every month puts the restaurant in a position where it doesn’t need to rely on any short-term or long-term financing. It also facilitates the ability to put excess cash into a liquid investment account. This investment account is available to offset negative, unforeseen, events. Or, to put towards future growth and expansion.

Restaurant cash budget Year 3

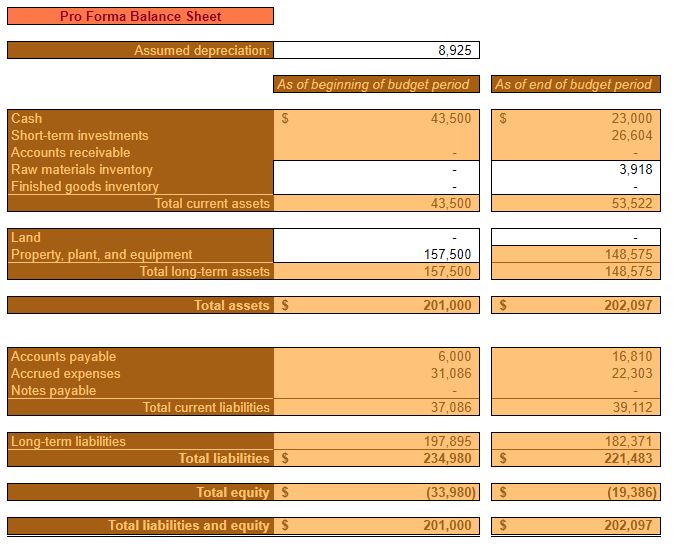

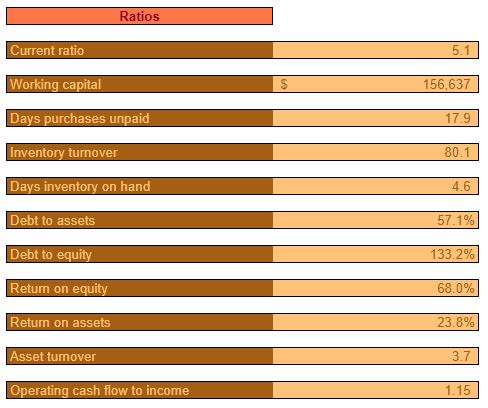

Year three is expected to see the continued reduction of debt and a subsequent increase in assets and equity. Certain balance sheet items like inventory, Accounts payable, and Accrued expenses are expected to increase in line with increasing costs as outlined in the operating budget.

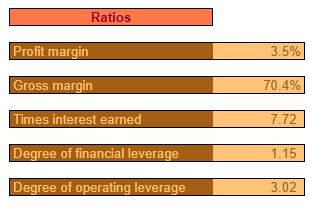

All ratios at the end of year three are expected to be relatively healthy. At this point, Diner, LLC. is expected to still have a relatively high Debt to equity ratio. This ratio is expected to continue to decrease, however.

Restaurant cash budget Year 4

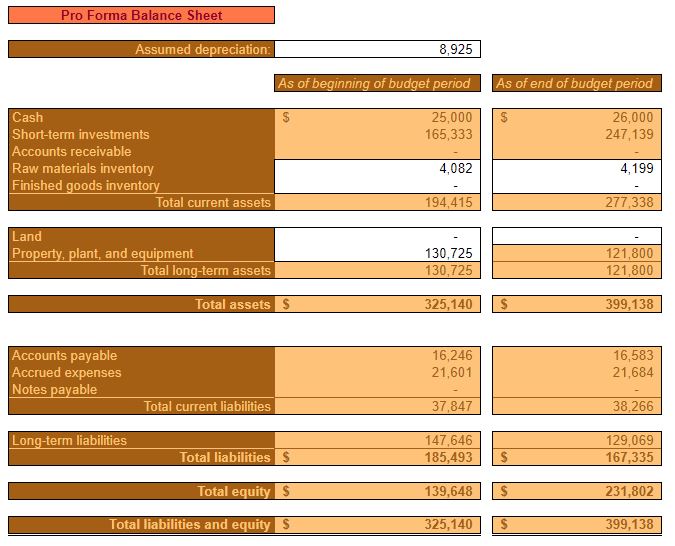

Throughout year four, assets and equity will continue to grow.

Cash and short-term investments begin to make up a considerable portion of assets.

The year four pro forma cash flow statement offers a different perspective than the income statement and balance sheet. It shows how it’s anticipated to be cash positive from operating activities and how the majority of that cash will be used to pay down debt and put into a short-term investment account.

Restaurant cash budget Year 5

By the completion of the fifth year of operation, equity is estimated to be between $250,000 and $300,000. Cash balances continue to grow at approximately $1,000 per year, in order to account for increasing expenses.

Barring unforeseen events, Diner, LLC. should be expected to adequately cover expenses and to deposit a considerable amount of cash receipts into short-term investments.

This growing investment account will serve as a margin of safety for unforeseen circumstances and/or will allow for expansion or other projects – should that course of action be chosen.

“How do startups get financial projections?” Financial projections for a business plan start with forecasting an operating budget and then a cash budget for the first five years of business. With these budgets, pro forma income statements and balance sheets can be created. Coupled with the inclusion of capital budget(s), an all-around picture of your startup’s financial future will come into focus.

The financial projections section of your business plan is the foundation for the funding request section. It’s also, in part, where you quantify the viability of your business idea. Lenders and investors will be very interested in this particular section. There are three primary components of the financial projection section.

A capital budget for these types of big cost/reward ventures can help you with the timing and amounts of revenue, expenses, and cash flow in the budgets that follow.

The reader of your business plan will appreciate the supporting information Plus, the extra analysis will help ensure that you are spending your funding wisely.

Start with sales

As emphasized in the operating budget template for small biz post, most financial projections start with forecasting sales. Why? Because of the volume of sales you (expect) to make, will drive how much you spend.

In the calculating funding requirements post, the point was made that you should project your financials out for five years. Yes, it’s nearly impossible to accurately predict your monthly revenue several years from now. However, the reader of your business plan will want to know that you’ve at least thought that far out.

Keep in mind that month 1 of your forecast probably won’t be the first month you expect to make sales. Rather, it will be the first month after you receive your funding requirements.

Your first month of sales might come well after that.

Spending money to make money

Now, knowing how much you expect to sell, you’ll have a better idea of what you’ll have to spend to make those sales.

It’s here that it’ll become obvious why you started forecasting after you received your funding requirements. Because, depending on the industry your business is in, you might have to spend a significant amount of your funding just getting set up. For instance, you might need to spend money on things such as:

Licenses, permits, and registration fees

Beginning inventory

Deposits

Down payments on fixed assets

Utilities

Other startup expenses

Plug these expenses into the appropriate months following the receipt of your funding requirements.

Once your pre-launch expenses are forecast, then you can focus on your operating expenses – the ones that will correspond with earning revenue. Different industries will have different costs in different proportions. But, here are some categories of costs to consider as you complete your forecasted operating budget:

Materials

Labor

Overhead (utilities, depreciation, real estate)

Marketing and sales

Administration (accounting, human resources, IT)

Match these costs up with your forecasted revenue and subtract them from that revenue. You should now have monthly estimates of your operating profit for the next five years.

Interest and tax expenses will be deducted from operating profit to arrive at the forecasted monthly net profit.

Remember your capital budget? Don’t forget to account for the revenues and expenses related to your projects and capital expenditures. A capital budget is built on cash flows in and out. So, you might have to adjust the timing of corresponding sales and expenses.

Pro forma income statement

With your revenue, cost of revenue, selling general and administrative expenses, interest expense, and income tax expense estimated, you can now put together yearly pro forma (expected) income statements.

This pro forma income statement will serve as a snapshot of your (hopefully increasing) profitability over the next five years.

Cash budgeting

The cash budget, not to be confused with the cash flow statement, specifies when cash will actually come into and leave your business.

The operating budget stated when you’ll make the sales, but not when you’ll actually collect cash. Some businesses collect cash more or less immediately. Restaurants and retail, for example. Others issue invoices and have to wait to collect cash. Some might even have customers who never pay.

Forecasting sales for the reader of your business plan is important. But, beyond that, they’re going to want to know when you’ll actually collect on the sales. That’s the point of the cash budget.

Why make a cash budget if it’s so similar to the operating budget?

A cash budget tells the reader of your business plan that you take cash flow seriously. That you understand cash must come in quickly and leave slowly – to the extent that it’s practical.

As mentioned, the cash budget is built off of the operating budget.

Just simply adjust all of those sales into the future and enter them in the month you expect to collect cash.

Alternatively, for each expense, adjust it to the month in which cash will actually leave your bank account.

From there, all that’s left to do is make a note of your starting cash. Then, add the cash you expect to collect every month and subtract what you expect to spend. This will leave you with a new cash balance at the end of every month which, in turn, becomes your starting balance the following month.

You haven’t forgotten about your capital budget, right? Those capital expenditures and projects can have a huge effect on cash flow. Make sure they’re being accounted for in your cash budget.

Pro forma balance sheet

The pro forma balance sheet is a snapshot of your company’s owner’s equity for each of the five years forecasted.

With your operating and cash budgets in hand, you have what it takes to calculate your assets, liabilities, and owner’s equity balances at the end of each year.

Admittedly, calculating a pro forma balance sheet can be a little daunting. If you’re not well-versed in accounting you might reach out to someone for help. Alternatively, you can use the Spreadsheets for Business example + template of a small business financial budget for inspiration. The pro forma balance sheet is automatically calculated based on what you enter for the cash budget.

A pro forma cash flow statement is also automatically calculated.

How do startups get financial projections?

The information above outlines the quantified information to include in your business plan.

I would suggest that you accompany each budget and pro forma statement with some qualifying information too.

For instance a written synopsis of why you forecasted what you did. A reasonable narration of your startup’s financial position over the next five years. This will help flesh out your vision of your company’s future and why it would be a smart investment.

The Funding Requirements section of your business plan is where you outline:

How much money your startup is going to need to begin operations and reach self-sufficiency

Whether you are seeking debt financing, equity financing, or both

Any other details regarding how the money will be used, how much will be returned to the financier(s), and when it will be returned

Unless you have a really big chunk of money saved up, you’re probably going to have to do what most other startups do – ask for money. Ultimately, the goal is, of course, to make the business self-sufficient. But, early on, if you want to scale up quickly, you’re probably going to have to leverage someone else’s money.

What would you want to know if you were giving someone money to start a business? Would you want to know how they’re going to use it? How they’re going to preserve it? How about how they’re going to build upon it?

Maybe you’re a lone wolf? You want to keep this operation as lean as possible. Particularly when it comes to people.

I can appreciate that!

Nevertheless, if you’re going to be funding this thing on your own, you still want to hold yourself accountable. You want a plan regarding where your money will be spent, and how you’re going to earn a return on it.

1) Capital, operating, and financial budgets

Starting a business from scratch is not so different from a decades-old business starting a new year. The required tasks are nearly the same.

Writing posts on, and making templates for, strategic planning topics is the foundation of this website. Capital, operating, and financial budgeting is critical to small business success.

The capital budget will specify any projects and/or large-scale assets you intend to buy. Plus, what kind of return you expect on that investment.

The operating budget is where you forecast your first one, three, or five years of operation. Your revenue, your cost of revenue, and your sales/administrative costs. An operating budget leads to the creation of a pro forma income statement.

Finally, your financial budget. This is your cash budget. It specifies when you think you’ll actually put money in your bank account from all those sales you’ll be making. It also specifies how you plan to stay solvent. This budget leads to the creation of a pro forma balance sheet and cash flow statement.

2) Determine funding need

All of the preceding budgets, particularly the financial (cash) budget, show where the money is going to be used. Once you compare the business’ cash needs to the cash you’re contributing, you’ll know how much is required from outside sources.

Budgeting will also show when and how the business is expected to make enough to support itself. Furthermore, other important milestones will be reflected. Milestones such as your first sale, your first $10,000 in revenue, your first $1 million in revenue(?), and so forth.

Can you see how these budgets will serve as a good measuring stick for your business’s launch and growth?

3) Funding details

Now that you know how much outside funding you’ll need to get off the ground, it’s time to really get into the nitty-gritty details.

Step one is to specify how much of the funding will be debt and how much will be equity. If you’re seeking equity investment, you’ll want to outline a proposal dictating what their investment will buy them. Also, how much power that equity investment will wield.

Another important point to clarify is the timeframe. For instance, things such as debt/balloon payments. If you’re really aggressive, there might come a point where you expect to cash out of the business and pay your equity holders

Whatever the case may be, you’re going to be clear about the status of the business at the end of the five-year forecast. Plans can change, of course, but you’ll want to include an exit strategy for those who are investing in you.

Finally, you should consider building on step one (budgeting) and clarify how the debt/equity funds will be used. Will it be for fixed assets, marketing, other operating expenses, or something else?

What are business funds?

Business funds are used by the business for their financial requirements. A business needs money to run. It is the oxygen that fuels its operations.

Starting a business is not cheap. To fund your new company, you’ll need some money upfront and this can be one of the first financial choices made by entrepreneurs when they start their own enterprise. But it’s also an important decision that could have lasting impacts on how your structure and run your business over time.

There are a variety of sources to turn to if you’re looking for small business funding. Capital may come in various forms like loans, grants, or crowdfunding.

Before you seek out funds, make sure to have a solid business plan and a clear outline of how the money will be used. Investors want assurance that their investments are being well managed so they can invest with confidence in the company’s future success!

What are funding requirements in a business plan?

This is what your entire business plan has been building up towards.

If you follow these steps for calculating funding requirements, don’t you think you’ll have an enormous amount of insight as you launch your startup?

This is the culmination of all the hard work you’ve put into your business plan thus far. Once completed, you’ll know how much money you’ll need, and what you’ll use it for.

Asking someone to invest in your business is like asking for a sale. Fortunately, if you’ve stuck with me this far you’re well prepared to write the funding requirement section of your business plan. I’m sure you’ll get what you need to be successful!

The marketing and sales section of your business plan is where you explain your strategy for bringing in sales. It is critical because making sales is paramount for business success.

The following example draws heavily from the previous two posts on the subject.

In this example, I’m using a fictional startup auto repair and maintenance shop we’ll call Auto Repair, Inc.

Feel free to copy this example and tweak it for your needs.

Marketing strategy

Auto Repair, Inc.’s (ARI) marketing strategy aims to earn a high return on investment (ROI) on marketing efforts. The marketing strategy is rooted in the marketing theme.

The goal is to carefully consider and continuously review the marketing strategy – making adjustments where necessary. Whatever strategies are implemented, adherence will be enforced.

Target market

As described in more detail in the market analysis section, ARI’s target market can be summarized as follows:

Households in the same or bordering ZIP Codes as the service facility

Male

Age 21 years and over

At least 1 vehicle available to the household

Household income ranging from $40,000 to $199,999 per year

Marketing theme

ARI’s marketing will adhere to a consistent message highlighting the benefits of using their auto repair services and their unique selling proposition (USP).

ARI will hold itself to the highest standards of honesty and integrity. The benefit to the customer will be knowing that they aren’t being deceived and not being charged for unnecessary repairs. The intent is to make ARI the first choice for automobile maintenance and repairs in the local market.

Furthermore, by paying for the expedited shipping of parts that aren’t in inventory, ARI will be able to offer its customers timely service. The benefit of expedited shipping is that customers won’t be inconvenienced for any longer than necessary.

It is these two things – honesty, and timeliness, that comprise ARI’s USP. This is what ARI will strive to be known for. It is what will make them unique among their competitors.

Promotional strategy

It is ARI’s intent to focus on three promotional strategies at any given time. The ROI for these promotional strategies will be measured to the extent possible.

Flexibility will be a priority. The promotional strategy that is performing worst will be replaced or adjusted upon quarterly review. This strategy should result in a continually increasing marketing ROI.

All promotional efforts will emphasize the previously mentioned marketing theme.

The following are the initial strategies ARI intends to employ:

Sponsoring local community events

ARI will focus on community events in the local metropolitan area that pertain to automobiles. These events will be sponsored, if possible. A presence will also be maintained at these events where coupons and promotional materials will be handed out.

Social media

ARI will maintain a strong social media presence. In order to increase the likelihood of effectiveness, ARI will outsource this activity to a local marketing firm. Additionally, ARI will employ the use of exclusive codes in social media promotions which will aid in tracking the scope and scale of social media efforts.

Referral program

ARI will implement a referral program that will strongly incentivize current customers to refer new customers. Under this referral program, if new customers state that they were referred by an existing customer, the existing customer will receive a 50% discount on their next oil change.

Technology

ARI will rely heavily on technology in order to leverage and measure the effectiveness of their promotional strategies.

Social media, as mentioned previously, will play an important part of ARI’s marketing strategy. Initially, social media will serve as one of the primary means of promotion.

Additionally, analytical tools will be relied upon to gauge the effectiveness of ARI’s marketing and sales strategies.

Finally, customer relationship management (CRM) software will be critical to maintaining a reliable database of prospects and existing customers. Plus, it will facilitate the collection of relevant information and aid in the overall marketing and sale strategy.

Pricing strategies

Carefully considered pricing is critically important to ARI’s success. Automobile service and repair is, unfortunately, viewed as a commodity. It is ARI’s intent, through an effective marketing strategy, to differentiate themselves from the competition and lessen the commoditization of their services.

ARI’s initial pricing strategies will be as follows:

Bundle pricing

A detailed analysis will be conducted to determine attractive, yet profitable, discounts that can be provided to customers who purchase two or more services concurrently. These dynamic pricing models will be programmed into the CRM software and applied automatically.

Psychological

Psychological pricing will also be used in promotional materials. Where practical, prices will be adjusted to the nearest $.99.

Sales strategy

ARI’s sales strategy revolves around a flexible, practical, and transparent process that makes all employees continuously aware of the company’s progress towards its sales goals.

Process

All of ARI’s employees will be coached on the sales process which revolves around its marketing theme. The marketing theme emphasizes customer service, honesty, and timely service.

This theme will be highlighted in all customer interactions. Particularly through the use of transparency in discussing repairs. Also, through emphasizing the expected time of maintenance and repairs.

Continuous learning

Training will be conducted quarterly for all employees and on an as-needed basis individually.

During training, the tenants of the marketing and sales strategy will be highlighted. Employees will be given the opportunity to ask questions and discuss scenarios. At this time, there will be an opportunity to address any necessary issues, shortcomings, or changes. All of this is done in an effort to reinforce the strategy, and to be flexible as needed.

Sales goals

At ARI’s quarterly sales training, sales goals for the company as a whole will be stated.

Additionally, the sales goals, and progress towards them, will be made clearly visible to all employees throughout the quarter. Every employee will understand the part they play in contributing to those goals.

Sales goals will be tied to the annual strategic plan, and, more specifically, the operating budget.

Sales goals will revolve around total revenue, and be broken down into monthly, weekly, and daily milestones.

Sales forecasts

Sales forecasts are covered in detail in the financial projections section of the business plan.

“What are smart goals in sales?” Smart goals are clear on:

What your business wants to achieve

How your business will know when it’s achieved them

Your business’ power to achieve them

The realistic possibility of achievement

The timeline needed to make the achievement

As a (soon to be) small business owner, you’re going to learn that meeting goals is critical to your success. Appropriate objectives allow you to orient yourself. They let you know where you are in relation to where you want to be. They also help you track your progress and keep your business growing.

Sales goals shouldn’t be so lofty that the reader of your business plan thinks you are trying to deceive them. On the other hand, you don’t want them so modest that your business looks like a bad investment.

The acronym SMART is, admittedly, overused. Though it’s cliché, it does serve as a good starting point for goal creation. If you adhere to the SMART guidelines, you should have worthwhile sales goals. Goals that will motivate you and show the world that your business has a plan for growth and success.

Credit: needpix.com

Specific sales goals

Goals are no good if they’re not specific. Abstract or subjective goals aren’t clear enough to provide motivation.

Which of these sounds better to you?

Increase sales every quarter.

Or…

Increase sales by 15% monthly in the first six months. 10% monthly in the second six months. And, 8% monthly in the second year of business.

The reader of your business plan is going to want to see something more like the second example. Concrete speculation about how you’ll grow your business.

Specific goals let you know when you reach them, and when you’ve fallen short. It also helps to divide goal achievement into manageable chunks.

Measurable sales goals

Specific goals can be measured. If you can’t measure your progress towards a goal, then you’ll never know if you’ve achieved it.

Which of the following gives you more confidence in a business?

“We plan to put ourselves in a position for success”?

Or…

“We plan to have 20% referral business by the end of our second year”?

The second example can be measured. The business can track referrals and will know if it’s progressing. If you can’t measure your sales goals, you’ll never know if you achieve them.

Attainable sales goals

Yes, everybody who launches a small business wants to be successful. Most have big dreams about achieving awesome levels of success. And that’s all okay.

However, if your goals aren’t realistic, they’re little more than dreams.

Which of the following seems more attainable for a startup cleaning business?

100% market share in their city?

Or…

After 3 years, obtain a 50% market share within the ZIP Codes that they operate in?

Theoretically, I suppose, 100% market share as possible. But, the goal of 50% market share (in the immediate vicinity) is much more attainable. It’s a stepping stone, in fact, to 100% city-wide market share.

Attainable goals bring milestones down to a more reasonable level. Meanwhile, they should be aspirational enough to translate into business success. The reader of your business plan will appreciate “stepping stone” goals over lofty visions of success.

Realistic sales goals

While stepping stone attainable goals add up to big-time attainable goals, unrealistic goals don’t lead anywhere. They’re so over-the-top that they’re just not practical.

Which of the following seems more realistic for that same startup cleaning business?

$1 million in revenue in its first quarter of operation?

Or…

$3,000 in revenue in the first month, Growing at a rate of 15% for the next five months?

The first goal isn’t going to motivate you. It sure as hell isn’t going to inspire confidence. The reader of your business plan would think that you have a tenuous grasp on reality. Therefore, they are unlikely to invest in your business idea.

Timely sales goals

Finally, goals have to work within the restraints of time. Just like anything else.

Think of it this way…

What if the startup cleaning business has a goal of $3,000 in monthly revenue? Is that good?

It depends, right? It might be good – if it was for month one. It’s not so great if they’ve been in business for five years.

Clarifying a timeline for your goals puts them into perspective.

What are 8 types of sales goals?

The SMART guideline tells you how to create your goals. But, it doesn’t tell you what metrics to use.

Sales affect everything in a business. Tracking total units and/or revenue is okay. However, you can expand upon that and go into more detail. The reader of your business plan will probably appreciate it.

Again, be mindful of the timeline. What’s most appropriate, do you think? Weekly, monthly, quarterly, yearly, or something else?

Furthermore, another thing to consider is breaking your sales goals down. This can be done by detailing products, categories, departments, salespeople, or any other way you deem appropriate.

Here’s a couple of ideas for different types of sales goals to reference in the marketing and sales section of your business plan.

Income statement-based

Sales units

Revenue

Margins (revenue – expenses)

Profit margin’s (profit as a % of revenue)

Conversion funnel-based

Leads generated

Prospects converted from leads

Customers converted from prospects

Repeat/referring customers

If you’re a brand new business you might focus more on the income statement-based sales goals. If you’ve been in business a while, you might find the conversion funnel-based sales goals more appropriate.

What are SMART goals in sales?

Once again, remember to keep the SMART acronym in mind when creating sales goals for your small business.

Though, you need not specifically reference the “SMART” guidelines in your business plan. The reader will recognize that your objectives are well-thought-out, achievable, and appropriate for your young company.

Furthermore, these sales goals will aid you, as an owner, to make steady, controlled, and healthy growth in your company – helping to ensure its long-term success.

Look at your company from your customers’ perspective.

Always communicate your product’s benefits and your company’s USP.

Keep reflecting on what works and what doesn’t.

Stop wasting time on markets that aren’t your target.

Do successful businesses struggle with sales?

No.

Sales are necessary for every business. So, it follows that the reader of your business plan would want to know your strategy for bringing in sales.

Furthermore, if the cost of bringing in those sales is too high, then they count for nothing. A sales strategy will help you gain control of your sales cycle. Having control of your sales cycle will help your young business bring in steady, continuous revenue.

Beyond that, this sales strategy and the tools and processes that grow from it can help your business thrive as it moves beyond its infancy.

Here are six tips for outlining a sales strategy in the marketing & sales section of your business plan.

1) Utilize technology

The reader of your business plan is going to want to be confident that you know how to use every tool in the toolbox, so to speak. They know that your competition probably does. And if your competition doesn’t, then it’s a great opportunity to make your startup stand out.

A benefit of utilizing technology is its ability to automate the marketing process. This frees up time for employees to connect with customers on a personal level – when necessary.

Is there more to marketing technology than just social media?

You bet. Here are some other technologies to consider:

Marketing technology helps you to stay top-of-mind with your customers. The first company they think of when they think of your product or service.

2) Develop a quality process

The reader of your business plan understands that there will be a learning curve for everything you do. Particularly with your selling process. However, they want to be convinced that you can climb these learning curves quickly.

Showing that you have the foundation of a quality selling process will give them confidence in your ability to succeed. Additionally, it will help those who sell for your company to sell as much as possible. An added benefit!

Are you concerned that you don’t know anything about documenting a sales process?

Start simple. Add complexity and tweak the process as needed. As time goes on, document what you’re actually doing. Is what you’re doing more effective than what’s documented? Less effective? This will help ensure that everyone who sells for you is adhering to best practices.

Knowing that everyone on your team is following your process will give you peace of mind. It will also make it easier to analyze your sales data and give yourself quality, actionable information to improve the process. Plus, it helps to identify the problems before they become catastrophic.

3) Take care of your customers

Is it easier to get a new customer or to keep an existing one?

You probably know the answer to that. You can bet the reader of your business plan does.

It is easier (and therefore cheaper) to take care of your existing customers.

Make sure that customer satisfaction is a prominent part of your sales strategy. Outline how you will keep your customers happy with rewards, engagement, customer service, or any other appropriate means.

4) Stick with a steady theme

People like consistency. Unpredictability does not breed trust.

Make sure that a consistent sales message is conveyed in the marketing and sales section of your business plan.

If every piece of marketing and every sales interaction answers these two questions – you should be alright. Make sure everyone in your business, not just the sales team, can answer these questions.

Also, make sure that your benefits and your USP coalesce with the other sections of your business plan. E.g. market analysis, organization and management, and service/product line.

5) Always be learning

Make it clear to the reader of your business plan that continuous learning is part of your ongoing sales strategy. This will show them that you are adaptable and you will continue to improve your sales results.

Show them that you’re going to hold your salespeople accountable. This doesn’t mean that you have to rule with an iron fist. It simply means that you’ll keep the feedback loop open. This will show the reader of your business plan that you can keep your employees motivated and will get the most out of their abilities.

Have you ever regretted stopping to catch your breath and to think about a situation?

Probably not.

In the midst of executing your sales strategy, stop every once in a while and reflect on what’s worked and what hasn’t.

It was here that you honed in on your ideal customer(s). Time, money, and energy spent trying to sell to anybody outside of your target market are wasted.

Again, make all of your employees understand your customer avatar(s). Particularly your salespeople.

Everybody in the world isn’t going to want your product or service. You need to understand the people with a problem that your product or service will solve. Doing so will ensure that your sales efforts are effective and efficient.

Convey to the reader of your business plan that you have a well-thought-out sales strategy. Make them confident that this strategy will not only help you give them a good return on investment (ROI) but it will also help you thrive in the long-term.