How do I make an inventory list and other spreadsheets for my restaurant?

Spreadsheets serve as a great complement to, or replacement for, the other software a restaurant might rely upon. Spreadsheets can handle nearly any task you require of them. They are very versatile. Small restaurants, with a limited software budget, might find them particularly useful.

The author states that a computer is “Second only to a good set of knives”. And spreadsheets are “the cat’s meow.” They can help a restaurant with organization.

Spreadsheets can intimidate some people. But, they are only as complicated as you make them. It is suggested that you take a course if you must. Particularly if you want to take advantage of the power of formulas.

Spreadsheets will make your life as a restaurant manager easier. Once you take a little bit of time to climb the learning curve.

Spreadsheets can fill in gaps in functionality for pieces of software. Many POS systems and most accounting software will export to .csv format – which can then be imported into a spreadsheet.

Some of the things a restaurant can use spreadsheets for

Staff scheduling

Drop in pre-made shifts for each employee

Order sheets

Purchase orders for ingredients

Automatically calculate tax and totals

Vendor lists

A master list of all vendors with name, address, phone, and email

Keeping good documentation will help with financing. Good documentation provides detail about how and why your startup restaurant will be successful. Spreadsheets are an excellent tool for providing documentation.

“Can I get an SBA loan with no credit?” Unfortunately, you cannot. But, there are other options available to start a business with no credit. Not every option is practical for every entrepreneur. Plus, each has its pros and cons. However, if you want to start a business and have no credit history, you should read further about your options.

To be clear, what follows is options for starting a business with no credit.

There are more options available for businesses that are already operating. Those are covered at the end of the post.

Here’s a summary of the options for getting a startup loan with no credit. Each is covered in more detail below.

“No-credit” loan option

Pros

Cons

Small business grants

Don’t require repayment

Limited availability

Microloans

Quick approval

Typically only available for “underprivileged” groups

Friends & family

Lenders who know you well

Potential to damage relationships

Get a co-signor

Can help establish credit

Co-signor is responsible if you don’t pay

Business credit cards

Easy to obtain

Need personal credit history

Crowdfunding

No repayment necessary

Typically only available for B2C businesses

Small Business Grants

Grants can come from anywhere, so requirements can vary widely. However, credit history is not typically a requirement.

Another benefit of grants, of course, is that they do not require repayment.

No credit history and no repayment? Sounds like a hell of a deal, right? Well, the catch is that grants are typically stringent in their requirements. Plus, there’s typically a lot of competition.

However, free money to start your business is a great thing. So, it doesn’t hurt to spend a little time researching grants that your business might be eligible for.

Microloans are often made by nonprofit organizations. Therefore, they are not as concerned with credit history or worthiness as a traditional financial institution.

So, what’s the catch? Microloans are typically only given to “disadvantaged” borrowers. Certain races, genders, etc. Therefore, if you’re a white male, you’re likely excluded from eligibility for most microloans.

Friends and Family

Friends and family are a potential source of financing to start your business if you have no credit history.

Friends and family know your character. Therefore, assuming your character is good, the chore is to convince them of the viability of your startup. To do this, you’ll need a good business plan.

Blood and money don’t mix. That’s how the saying goes. The reason is that it can damage relationships with your friends and family. That might be too high of a price to pay. So, move forward carefully.

Find a Cosigner

If your time horizon is long enough, you can build credit by taking out a loan and asking someone to cosign with you. A cosigner increases the likelihood of approval.

Consistent, on-time repayment of the loan will help build your credit. Solid credit history will help you get a loan to start a business – someday.

In fact, depending on the nature of your business, you could technically use a cosigner to get a loan to start your business right now.

For instance, if you are buying a piece of equipment, or vehicle, or some other asset that serves as the foundation of your business. Something that makes for good collateral. It’s possible, with a cosigner, that you could take out a loan for that equipment – and then be in business.

Business Credit Cards

I hesitated to include this option because I don’t want it to come off as deceptive. It’s splitting hairs and a matter of interpretation. It depends on whether you or your business, have no credit history.

You can fund your business with a business credit card. If your business has no credit history.

However, you will almost certainly need a personal credit history in order to get a business credit card.

Crowdfunding

Most crowdfunding isn’t a loan. But, it can be a different means to the same end.

Indiegogo, Kickstarter, and GoFundMe are examples of crowdfunding.

Generally, business-to-consumer (B2C) companies have more success with crowdfunding than business-to-business (B2B) with crowdfunding.

Typically, repayment isn’t required for crowdfunding. There are three types of crowdfunding that do not require repayment. These are:

Donation-based

Donation-based crowdfunding is where supporters give money without any expectation. Typically, this is reserved for people in need.

Therefore if you want to pursue this avenue, your business had better serve a critical need for society.

Equity-based

Equity-based crowdfunding is a situation where people who contribute to your company also become owners. Their expectation is to earn a return on their contribution. Just as a shareholder in a publicly traded company would.

Rewards-based

With rewards-based crowdfunding, you promise supporters a product or service in return for their contribution.

No-credit options for established businesses

Below, are some other frequently-cited options for getting a business loan with no credit. However, they are only going to be available for existing businesses. These are not loans you can get to start a business.

Nevertheless, I include them because they could be viable options for financing in the future, as your business grows.

PayPal Working Capital

As you might’ve guessed, this is only an option if you process payments via PayPal.

You must have a 90-day history with and a PayPal Business or Premier account. Additionally, you must process up to $20,000 annually through PayPal.

A PayPal Working Capital loan is paid back by PayPal taking a little bit of each subsequent sale that you make through PayPal.

Invoice factoring

Fundbox and Bluevine are examples of invoice factoring.

Invoice factoring is also known as factoring accounts receivable (AR). Invoice factoring is where you use your AR as collateral for a loan. So, obviously, you have to be in business, making sales, in order to have accounts receivable.

“Do you need to get a business loan for your startup?” No. But many startups will choose to secure a loan to start their business. Why? Primarily because most entrepreneurs don’t have the means to finance 100% of their startup. Also, equity financing is typically only available for high-growth businesses.

Debt vs equity financing for startups

Most startups need financial help from outside sources. These sources of financing fall into two general categories:

Debt

Equity

Debt financing

Debt is borrowed money that must be repaid according to an agreed-upon schedule and at an agreed-upon cost (interest rate).

One of the advantages of debt is that you don’t give up any ownership of your business. All the lender is concerned about is receiving regular repayment plus interest.

Once the loan is paid off the relationship with the lender ends.

Additionally, interest is tax-deductible. It is subtracted from operating profit before taxes are calculated.

Finally, debt repayment is predictable. It’s an easy expense to forecast.

That’s also one of the disadvantages, though. Debt is a fixed cost.

If the proceeds from debt aren’t used in a manner that earns a good return on investment (in terms of revenue or reduced costs) then that fixed expense drags the business down. Whether times are good or bad the cost of debt stays the same.

Another downside of debt for startup financing is that you may have to personally guarantee repayment of the loan with your own personal assets.

Equity financing

Equity is ownership of the business. Unless you give someone else equity in your business, you will always have 100% ownership.

If you finance with equity, you give up a certain percentage of ownership of your business. I.e. profits and sales proceeds.

Equity has its advantages.

For starters, you are not obligated to repay equity financing. The outside investor should understand that risk

One disadvantage of equity is that your investors may not agree with your business decisions. Since they are owners, you’ll have to take their opinions on managing the business into consideration.

Investors can be bought out, but that can be expensive.

Types of loans for startup businesses

Not all startup business loans are the same. If you decide to secure a loan to start your business, you have several options.

Equipment financing loans

Loans for startup businesses have strict standards that must be met. If you call the loan by a different name, those standards might loosen.

Equipment financing loans are for buying equipment, machinery, and other fixed assets.

The equipment you purchase serves as collateral for the loan. Repayment is typically made in installments.

Business credit cards

In addition to providing financing, business credit cards can establish credit for your business.

It’s likely that you will have to “cosign” with your business (personally guarantee) before getting a business credit card.

Business credit cards also, often, come with generous rewards programs.

SBA loans

The Small Business Administration doesn’t lend to your business directly. They guarantee the loan to incentivize the lender.

SBA loans are, typically, more “paperwork-intensive” than other options.

SBA loans can also be made for larger amounts than some other alternatives.

Microlender loans

Microlenders are non-profit organizations that provide debt financing to startups who might not qualify with traditional lenders.

These loans are typically “smaller” than those made by a traditional financial institution.

P2P loans or crowdfunding

Peer-to-peer loans, currently, are only made to individuals. Not businesses.

P2P loans are also, typically, small. But, approval and funding are quick.

Loan crowdfunding, unlike other types of crowdfunding (donation, exchange, and equity), requires payback. It’s not dissimilar to P2P loans.

Friends and family loans

Borrowing from a friend or family member might be easier. But, it can come with other complications.

Make sure the terms of the friend/family loan are clear.

Obtaining a startup business loan

If you’ve decided to secure a loan for your startup, these are, more or less, the steps you’ll follow to get funding:

Keep in mind the fixed assets you’ll need to launch.

Also, money that will need to be spent before operations commence.

Additionally, your small business will need cash-on-hand at launch

Work in an additional amount for unanticipated expenses you might incur before your business becomes self-sufficient.

2) Decide what type(s) of startup business loan you want

Review Types of loans for startup businesses, above, and choose one or more that suits your business’s needs.

3) Compare loan providers

Several different providers should be available for whatever type of loan you seek for your startup.

Compare costs, terms, credit requirements, collateral required, documentation, business requirements, and other variables between providers. A table with the providers in the left column and the variables along the top might help you compare.

Look up and compare reviews for providers, too.

APR

Loan term

Credit req

Collat needed

Docs needed

Biz req

Reviews

Provider 1

Provider 2

Provider 3

4) Assemble the needed documentation

Every type of startup business loan will require at least some type of documentation.

Common types include a business plan, historical financial statements, personal & business bank statements, personal & business tax returns, legal documents (leases, contracts, etc). Be prepared to provide more documentation. This should get the ball rolling, though.

5) Complete the application process

Each type of startup business loan will have its own unique application process.

You can apply with more than one provider at a time. This could help you secure a loan quicker. Beware of the effect of multiple inquiries on your credit score, though.

What factors can get your startup business loan application declined?

Not every loan gets approved. In fact, a lot of startup business loan applications get declined. Don’t despair.

If you do get rejected for a loan try to get an authentic reason why. Rejection sucks. But, understanding your shortcomings can help make it clear what you need to work on.

Here are some areas to address, before you apply, to minimize your chances of rejection.

Low credit score

Lenders aren’t visionaries. They rely heavily on the mysterious algorithm known as a credit score.

If your (or your business’s) credit score is too low, you’ll be systematically dismissed. Work to get your credit score to the minimum needed for the type of loan you’re seeking.

Lack of credit history

This can affect your credit score.

If you have no credit history, then, in most lender’s eyes, you have bad credit.

Fortunately, it doesn’t take too long to build a credit history. If you do so with on-time payments, a lot of your credit issues should disappear.

A high-risk industry

Lenders want to minimize risks.

If they deem your industry (or business model) high-risk, they will likely decline your loan application. If they don’t understand your industry (or business model), they’ll probably deem it high-risk and decline your loan application.

If you find yourself in this position more thorough market research might help. Plus, you might search for a lender that specializes in your particular industry.

Character issues

A criminal history and/or a bad reputation can result in a declined loan application.

Conviction of a crime involving “moral turpitude” is likely an instant rejection. If you’re unsure, you can speak with a representative of the lender to gauge their stance on your crime.

Infamy as a particularly immoral person, even if not criminal, isn’t going to help your cause either. In instances like this, you’ll likely have to apply somewhere your reputation doesn’t proceed you.

Lack of collateral

Collateral lowers risk for lenders. If things go bad, they can sell the collateral and recoup some of their losses.

However, if you’re securing a startup loan to pay for things like labor, marketing, or research, then there is nothing tangible for them to sell if you default on the loan. Therefore, they’ll see the loan as riskier and the likelihood of your business getting declined increases.

Capacity to repay

Low margins, a poor location, and many other factors can make your financial projections suspect in a lender’s eyes.

Even if you can show that it is possible for you to pay back the loan, that possibility might be based on so many shaky assumptions that the risk is too high to make a startup loan to your small business.

A poor business plan

A well-researched and thought-out business plan sends a strong message. It shows that you have carefully considered the present and future environment of your startup.

Beyond that, if it’s done right, it also serves as a marketing tool for the funding your startup needs to be successful. Every section of your business plan should make a case for loaning your small business the money it needs.

Lack of quality advice

Business is complicated.

It could be that your business is a good credit risk, but, you’re just not able to convey that to lenders. If that’s the case, check with your local SCORE chapter. There may be volunteers with that organization that can help you put your best foot forward.

Giving up

You’ll get declined for every loan you don’t apply for. Rejection can be discouraging, but try to take a lesson from it and make improvements where needed. Don’t keep banging your head against a wall.

Also, if you’re going to pitch your business, show some enthusiasm. Business revolves around selling and your startup’s potential is the first thing you have to sell. If you’re not pumped about your startup’s potential, then go back to the drawing board and refine it until you are.

Do you need to get a business loan for your startup?

It technically isn’t necessary to secure a loan to start a business. But, if you want to start a business, there’s a pretty high likelihood that you’ll need one.

Understanding your options and the loan process will help you decide what kind of debt financing is right for you. It will also help you to be prepared and increase the chances of your approval.

The financial projections section of your business plan is where you forecast your sales, expenses, cash flow, and capital projects for the first five years of your small business’s existence.

This is a critical section for readers of your business plan. It tells them:

How you expect your startup to perform financially

When you expect your new business to be profitable

How profitable you expect it to be

These are things you’d want to know as an investor, right? It’s up to the reader to decide whether they think your forecast is feasible.

Additionally, as an entrepreneur, it forces you to consider, thoroughly, what the first five years of business might look like. This will give you a good plan to work off of, will help you to be proactive, and will increase your likelihood of success.

Finally, the financial projections are the foundation of your funding request. Of course, your funding request, after all, is the primary purpose of your business plan.

Without knowing how much cash you need to launch and operate early-on, you won’t know how much you need to ask for. The funding request relies heavily upon financial projections, particularly the capital budget.

An example of a funding request, for this same business, will be posted separately.

This example of financial projections is built off of two previous posts:

Download the restaurant financial projections spreadsheet

If you’d like to download the spreadsheets I used to make these financial projections for a restaurant that can be done below. Keep in mind that these were (hastily) built off of budgets for a manufacturing company and tweaked for the restaurant industry. However, they should serve as a good starting point.

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

Startup restaurant financial projections

The financial projections for Diner, LLC provide a well-thought-out, cohesive, and comprehensive forecast of the restaurant’s performance from initial funding through the fifth year of operation. These forecasts will validate the feasibility of the concept and the appeal of an investment in this venture.

The financial projections for Diner, LLC include an initial capital budget for all of the fixed assets and other costs necessary to launch the restaurant.

Additionally, five years of pro forma income statements are included. These pro forma income statements are built off of a detailed five-year operating budget.

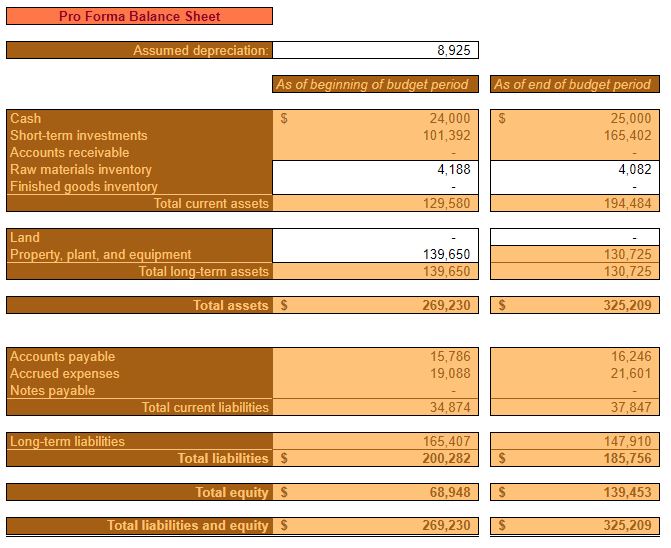

Furthermore, five years of pro forma balance sheets are also included. These pro forma balance sheets are built on five years of detailed cash flow analysis.

For the purpose of brevity, not every detailed budget is included in this business plan. However, all are available for decision support, upon request.

Items in italics represent those directly referenced in the financial projections.

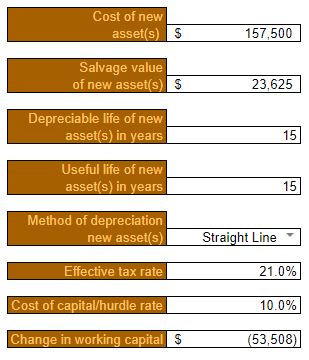

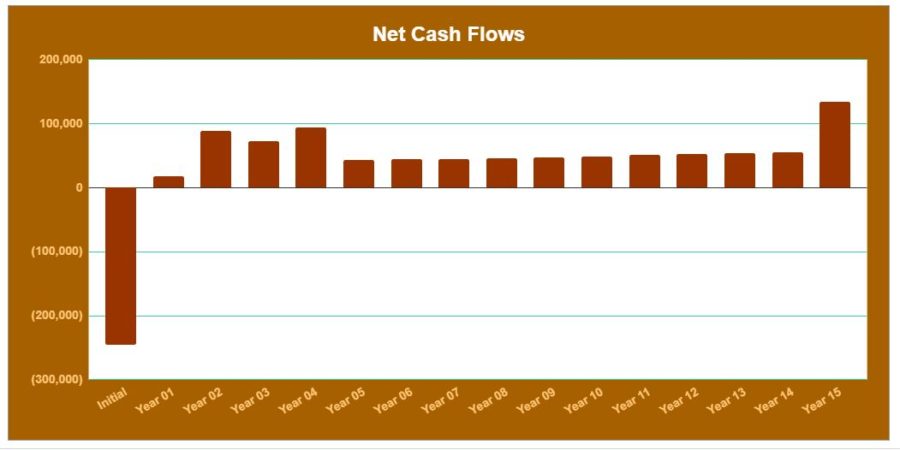

Startup restaurant capital budget

The capital budget summarizes Diner, LLC.’s forecasted operational and cash flow results over the next fifteen years. It takes into account:

Fixed assets needed to operate the restaurant

Launch costs necessary to begin operations

Cash-on-hand needed to launch the restaurant

To cover unanticipated expenses

Fixed assets necessary to operate Diner, LLC. are estimated to cost $157,500.

The salvage value after fifteen years is estimated at $23,625.

On average, all assets are assumed to have a depreciable (and useful life) of fifteen years.

Fixed assets will be depreciated using the straight-line method.

The effective tax rate, for purposes of calculating a depreciation tax shield, is estimated at 21% throughout the capital budget.

A discount rate of 10% is used to calculate NPV and other capital budgeting metrics. This discount rate considers the cost of borrowing (6%) and adds an additional risk premium of 4%. 6% is the estimated interest rate for an SBA 7(a) Small Loan and is calculated by adding 2.75% to the current Prime Rate (3.25%).

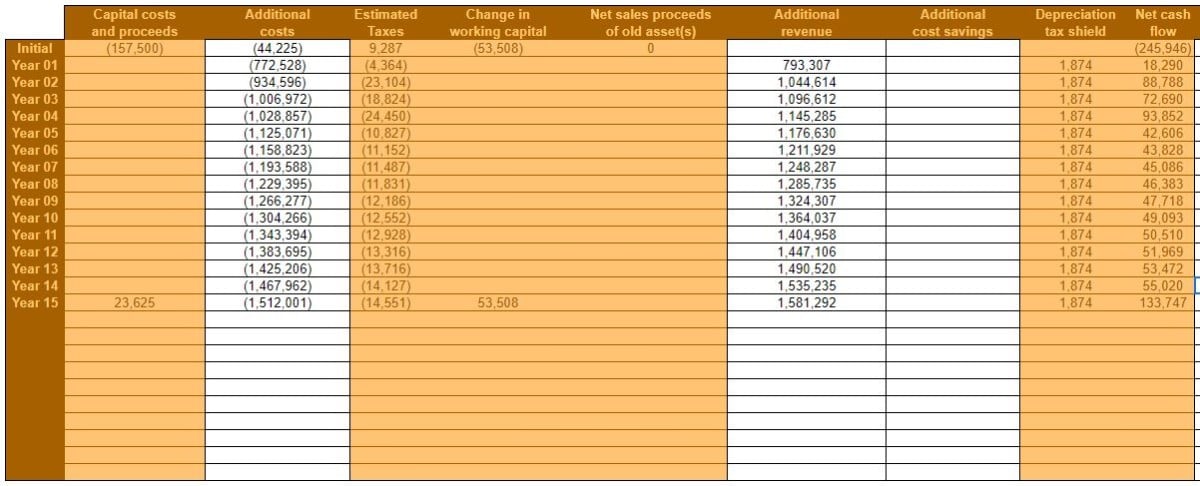

Click to enlarge

Initial Additional costs include launch costs that can’t be depreciated. E.g. professional services, organization & development costs, and other pre-opening costs.

Additional costs for Year 01 through Year 05 are pulled directly from the operating budget. Additional costs for Year 06 through Year 15 are assumed to grow at a rate of 3% per year after Year 05.

Additional revenue for Year 01 through Year 05 is also pulled directly from the operating budget. Additional revenue for Year 06 through Year 15 is assumed to grow at 3% per year after Year 05.

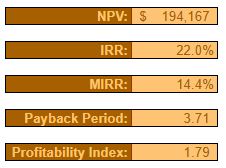

Over the course of fifteen years, the Summary of the capital budget shows:

Net present value (NPV) of $194,167

Internal rate of return (IRR) of 22%

Modified internal rate of return (MIRR) of 14.4%

Payback period of 3.71 years

Profitability index of 1.79

It’s worth noting that if the restaurant were to be sold at the end of fifteen years, the NPV would be considerably higher – accounting for the proceeds from a sale.

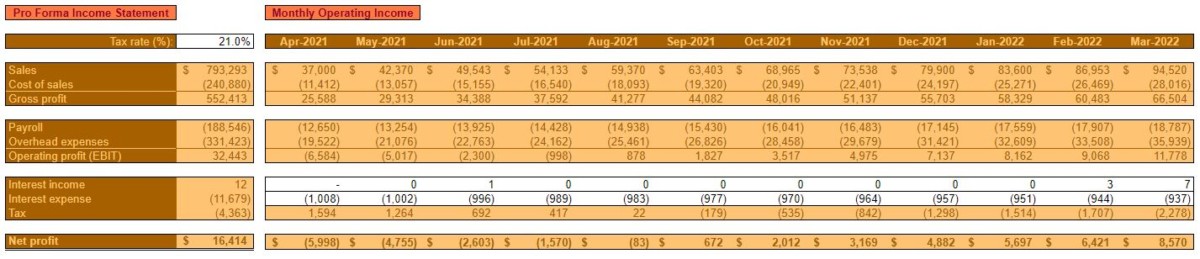

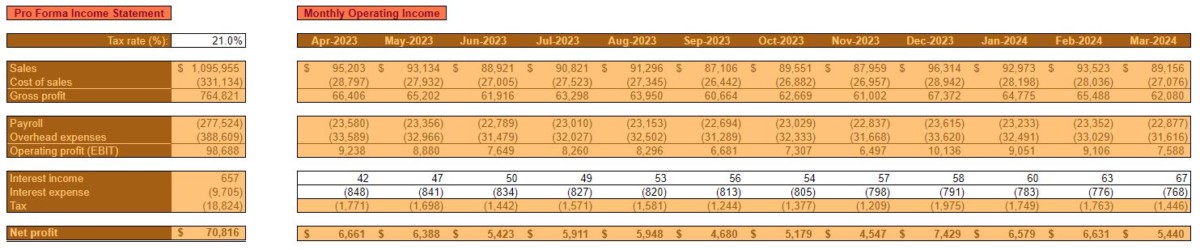

Startup restaurant operating budget

In the operating budget, Diner, LLC.’s sales, ingredients (cost of sales) payroll, and other overhead expenses are forecasted by month. Additionally, annual amounts are shown in a Pro Forma Income Statement. Each individual component of the budget is analyzed and forecasted separately in an attempt to be as comprehensive and realistic as possible.

Restaurant operating budget Year 1

Click to enlarge

Year one of operations is characterized by low initial sales that grow quickly throughout the first 12 months of business. The first month of profitability is estimated to be Month six – September 2021.

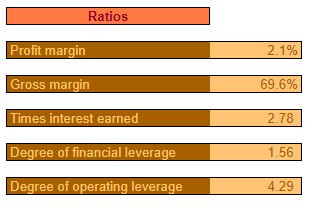

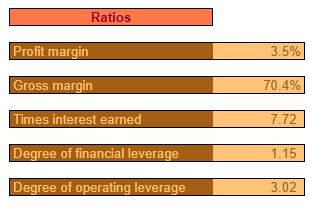

As such, the Profit margin is very low for the year overall but, it is expected that the year will be profitable.

Click to enlarge

The Sales Budget breaks down the expected Unit volume and Dollar Sales for each category of products sold. These categories are:

Entrées

Appetizers

Desserts

Non-alcoholic beverages

Alcoholic beverages

Each individual product in a category will have a different price, of course. However, for the sake of simplicity, items were grouped by category and an average Sales Price is estimated.

Sales prices will initially be set higher than average. At or near the “indifference price point.” At this price point, the number of customers that consider the price a bargain should be close to the number that feel it’s starting to get expensive.

This is done with the hopes that the Diner, LLC.’s novelty, image, and quality will still provide a perceived value for customers. Additionally, pricing as high as practical will help to offset the low initial Unit Sales after launch.

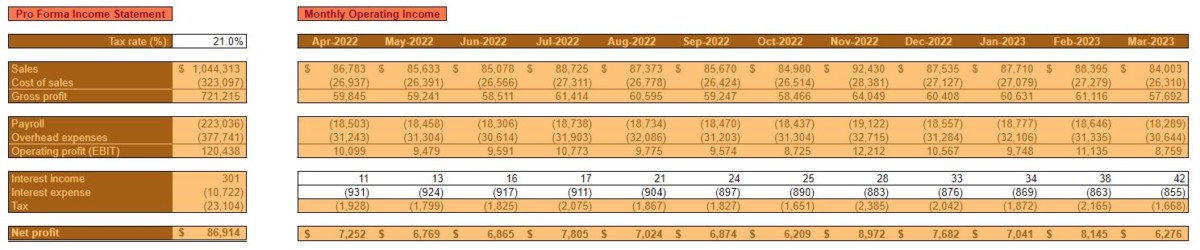

Restaurant operating budget year 2

Click to enlarge

Year two of operations is characterized by a leveling off of Unit Sales after reaching near practical capacity at the end of year one.

Additionally, it’s anticipated that Sales Prices will remain the same throughout the year after being on the high side in year one.

However, in spite of rising costs, overall sales are expected to increase significantly due to consistent demand throughout year two.

Click to enlarge

As mentioned, most costs, including ingredients, are expected to increase by an average of 3% in the second year.

As with sales categories, for the sake of simplicity, ingredients are grouped together into categories. Their costs represent an average of all the ingredients contained in a category.

Restaurant operating budget Year 3

Click to enlarge

In year three, unit sales are expected to continue to remain level. Sales Prices are anticipated to increase by approximately 5% to offset increased costs. Diner, LLC. is expected to have its highest year of profitability yet.

Click to enlarge

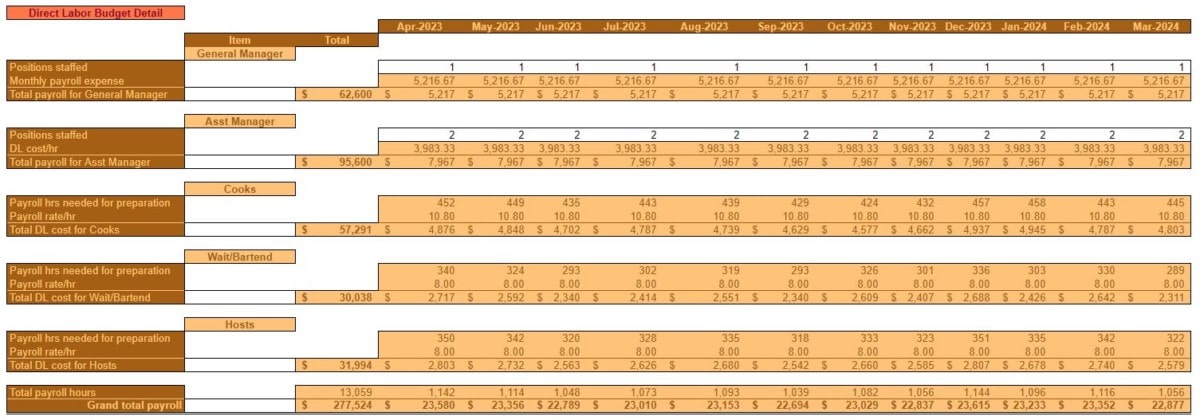

As was the case in year two, payroll is again expected to increase. This is due to an increase in wages and salaries of roughly 3%. It is Diner, LLC.’s intent to incentivize customer service and quality through above-average employee compensation.

In years one and two, the staff is expected to consist of:

One General Manager and one Assistant Manager, along with Cooks, Waitresses/Bartenders, and Hosts as needed, part-time, depending on sales volume. The General Manager and Assistant Manager are expected to cover any staffing shortcomings.

In year three, however, it is budgeted to add a second Assistant Manager position to relieve some of the responsibilities of the other managers.

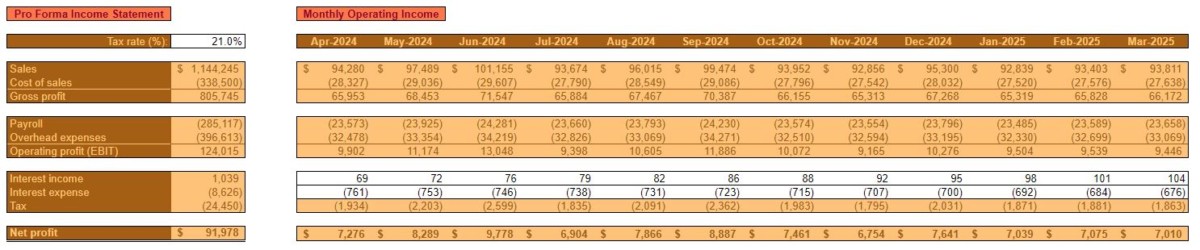

Restaurant operating budget Year 4

Click to enlarge

With Unit Sales, for all practical reasons, expected to be maxed out, Sales Prices would need to be increased in year four in order to achieve meaningful revenue growth.

As is typical, all costs are expected to increase by 3%, on average, in year four.

One exception is the Rent/Occupancy expense. When operations are initiated, Diner, LLC. is expected to enter into a three-year lease. At the beginning of year four, the lease will have expired and a new lease will need to be signed. A 10% increase in Rent/Occupancy expense is anticipated.

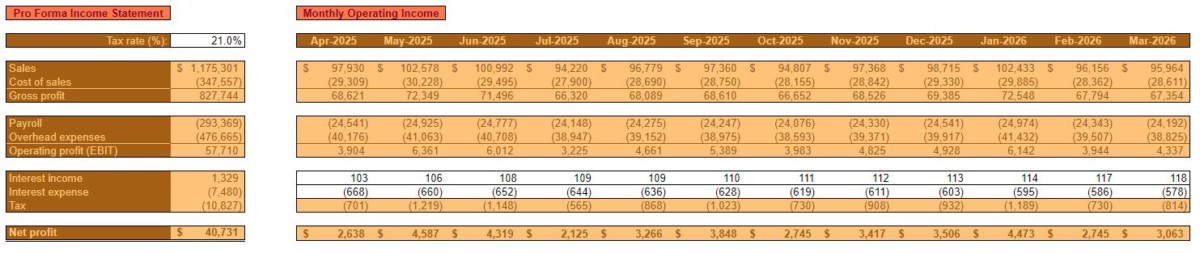

Restaurant operating budget Year 5

Click to enlarge

By the end of year five, Diner, LLC. is expected to remain profitable. That is, as long as Sales Prices are kept adequately above costs without sacrificing demand.

In order for the Diner, LLC. to grow from this point, the opening of a new location or another type of expansion would need to take place.

Click to enlarge

Startup restaurant cash budget

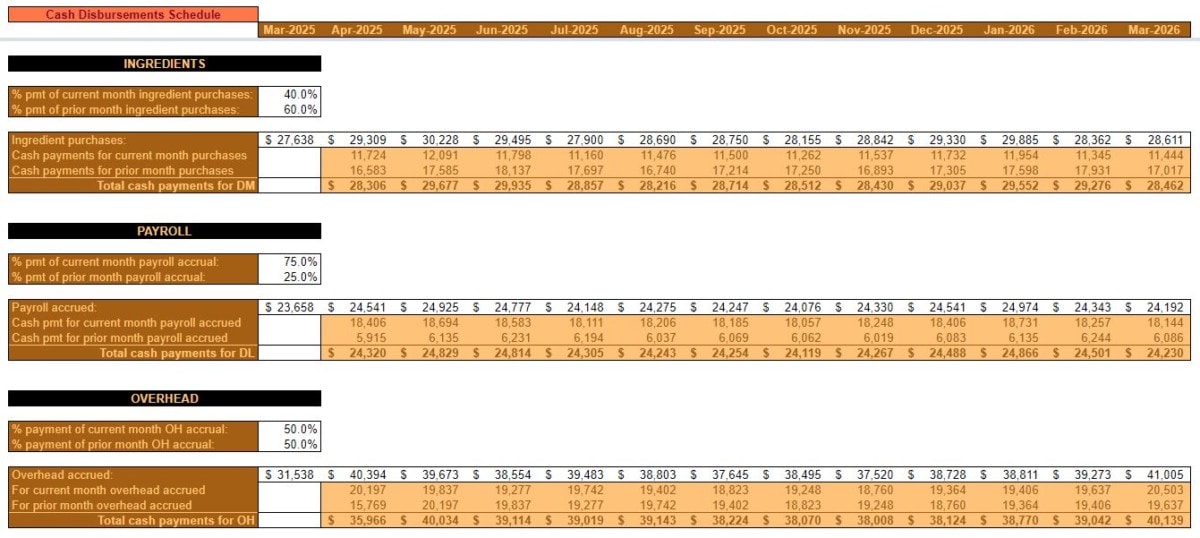

The cash budget forecasts the timing of cash collections and cash disbursements. This is done in an effort to ensure that Diner, LLC. remains solvent.

Obviously, the nature of the restaurants’ business model is such that cash collections are always made at the time of sale. So, no Accounts receivable are ever anticipated to be on the books.

However, ingredients, payroll, and overhead are not necessarily paid for in the same month but those expenses are incurred. Therefore, the timing of cash flow out will not necessarily correspond with expenses on the operating budget.

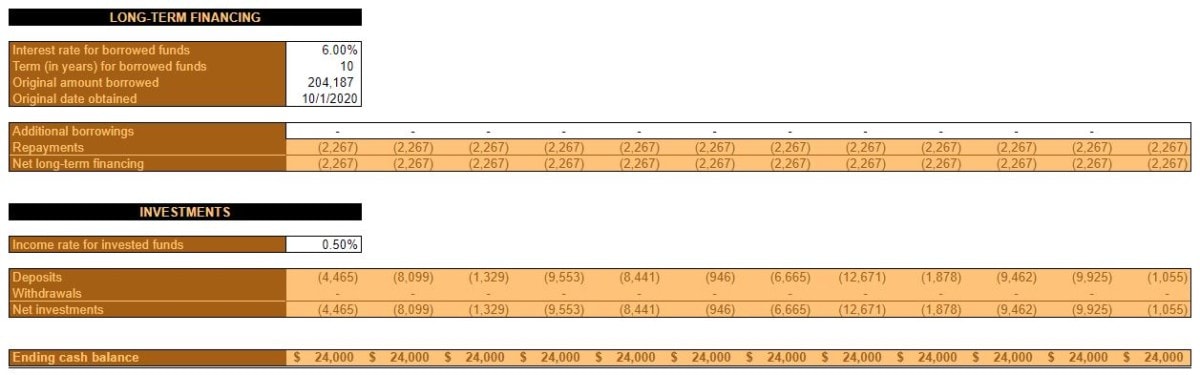

The cash budget is where a Desired ending cash balance is specified. Additionally, details on any financing (long-term and/or short-term) and savings account balances are also addressed.

Restaurant cash budget Year 1

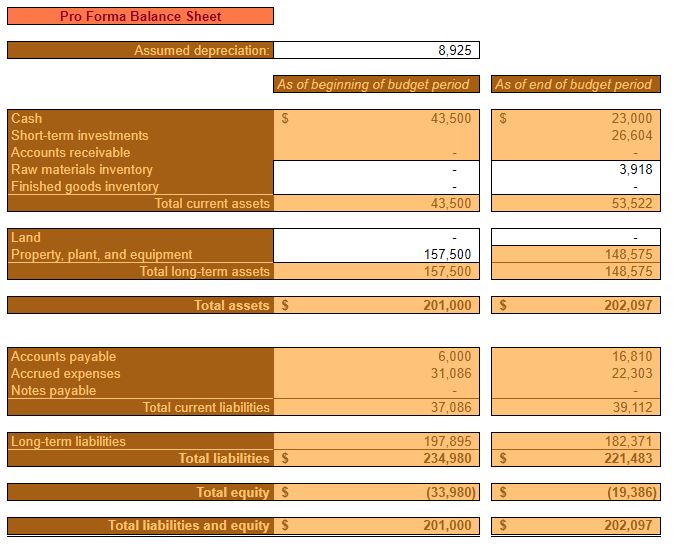

In the time leading up to the first month of operation, a considerable amount of money will need to be borrowed by Diner, LLC. to pay for pre-opening expenses. The Beginning cash balance is set at $43,500 in order to offset low initial sales.

Click to enlarge

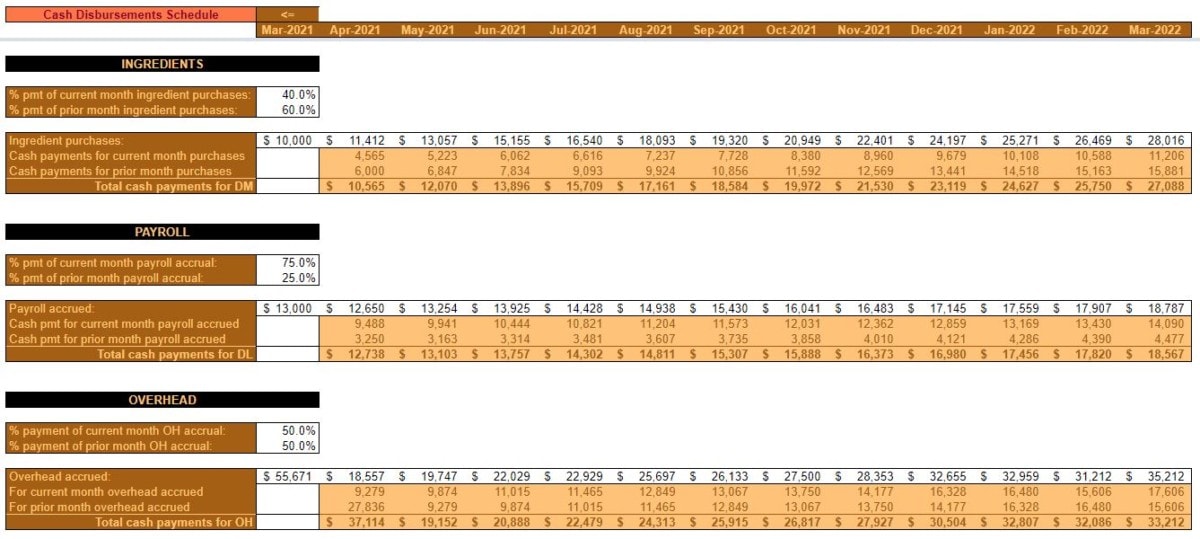

Pre-opening ingredient purchases, payroll, and overhead expenses are estimated and accounted for.

The timing of cash payments is estimated by assigning a % pmt of current (& prior) month for each expense type.

Restaurant cash budget Year 2

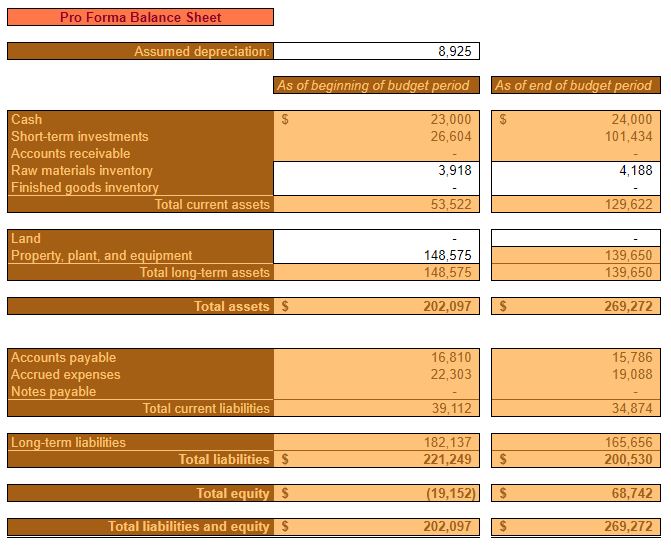

The increase in Unit Sales for year two is expected to help turn negative equity positive. Additionally, prudent cash management is expected to contribute to the security and solvency of Diner, LLC.

Click to enlarge

Maintaining an Ending cash balance of $24,000 every month puts the restaurant in a position where it doesn’t need to rely on any short-term or long-term financing. It also facilitates the ability to put excess cash into a liquid investment account. This investment account is available to offset negative, unforeseen, events. Or, to put towards future growth and expansion.

Restaurant cash budget Year 3

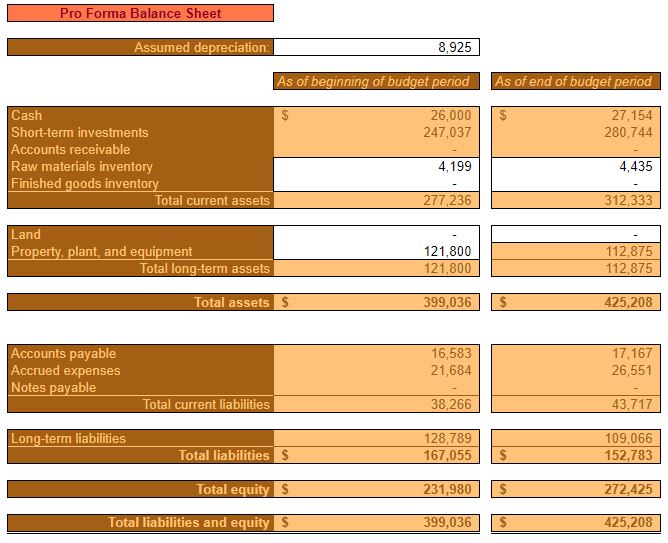

Year three is expected to see the continued reduction of debt and a subsequent increase in assets and equity. Certain balance sheet items like inventory, Accounts payable, and Accrued expenses are expected to increase in line with increasing costs as outlined in the operating budget.

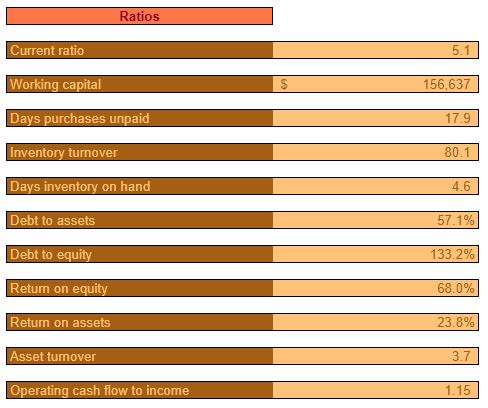

All ratios at the end of year three are expected to be relatively healthy. At this point, Diner, LLC. is expected to still have a relatively high Debt to equity ratio. This ratio is expected to continue to decrease, however.

Restaurant cash budget Year 4

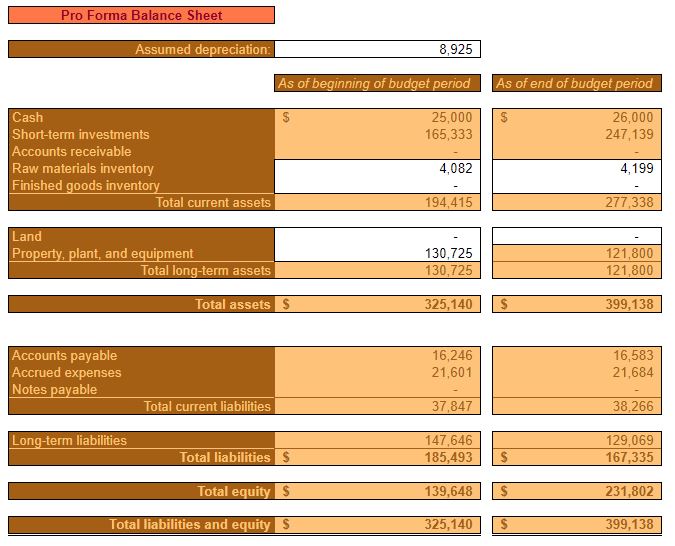

Throughout year four, assets and equity will continue to grow.

Cash and short-term investments begin to make up a considerable portion of assets.

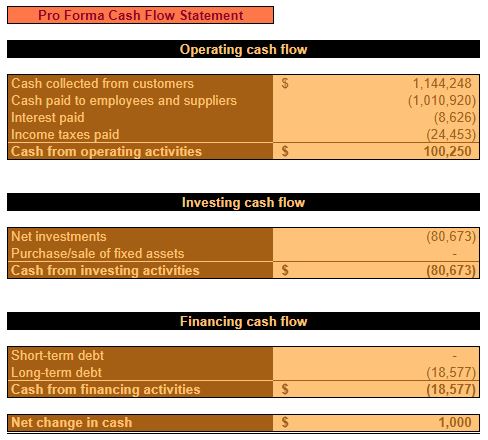

The year four pro forma cash flow statement offers a different perspective than the income statement and balance sheet. It shows how it’s anticipated to be cash positive from operating activities and how the majority of that cash will be used to pay down debt and put into a short-term investment account.

Restaurant cash budget Year 5

By the completion of the fifth year of operation, equity is estimated to be between $250,000 and $300,000. Cash balances continue to grow at approximately $1,000 per year, in order to account for increasing expenses.

Barring unforeseen events, Diner, LLC. should be expected to adequately cover expenses and to deposit a considerable amount of cash receipts into short-term investments.

This growing investment account will serve as a margin of safety for unforeseen circumstances and/or will allow for expansion or other projects – should that course of action be chosen.

How do you write a compelling company description for your business plan? You know your company inside and out. But, it can be difficult to convey those things in a way that will grab readers’ attention. The key is to start with what you know and build on it with some simple methodologies.

The company profile section of the business plan is your opportunity to make a memorable introduction to whoever may be reading. But, most of all, it’s a chance to set your startup apart from other aspiring businesses. Businesses that are after the same investment dollars you are.

If you’ve written a profile for your small businesses on social media (or your own website) then you’re off to a good start. Something is better than nothing. However, there are steps you can take to make your company profile stand out.

The same general principles apply for company descriptions in a business plan and company profiles on websites. You might have the urge to keep it very buttoned-up and boring. That’s an outdated notion, though. Don’t be afraid to let your company’s uniqueness and creativity show in this part of the business plan.

Again, there’s an opportunity here to really resonate with the reader. There are lots of other (critical) sections of the business plan that are going to deal with numbers and other technical aspects. The company profile may very well be the most memorable part. That is, if it’s written correctly.

Approaches to get started

Below, are a few methods to try out when drafting your company description. I suggest you try several of them – even if only briefly. Hopefully, one of these approaches will ring true and capture the essence of your company.

You’ll notice that there’s a lot of bleed-over in these different methodologies. They’re not all 100% unique. What that means is that you can incorporate many of these approaches in your business plan company description. You need not adhere to just one.

Of course, with all these methodologies there are certain things that are going to need to be included. But, don’t let that make you feel stifled. There’s still plenty of room for imagination and authenticity.

The must-haves are:

What your company does

Who your customers are

Where your company is located

The legal structure

Who are the founders are

A brief history

Beyond that, you’re free to approach this task however you see fit. Have fun with it!

Also, much like a mission statement, you don’t want to let your company description go stale. Even after you’re done with your business plan, you’ll want to include a company profile on your website and/or social media. Don’t just set it and forget it. Revisit it from time to time and make sure that it’s reflective of what your companies evolved into.

1) Make it personal

As the founder, you know what the company means to you. That’s a great starting point for a powerful company description. What was it that inspired you to start this business? What was unique about the road that brought you to this point?

A company profile from your perspective gives your business plan a personal touch. Something that will hopefully hit home with the reader. To really go above and beyond you can include a picture of yourself and a signature. A little extra human touch.

2) Emphasize the people behind your product/service

This is similar to the make it personal approach. But rather than focusing on you, the founder, you’ll focus more on your team. Ultimately, it’s people that make a company. Products and services are important, but it takes human effort to make a business successful.

Perhaps you don’t want to focus on team members specifically? You can instead focus on the personality traits or human qualities that encompass the team. Whether it’s passion, diversity, or expertise, you can highlight those factors that make your team exceptional.

3) Tell your company story

People love stories. In this case, you don’t want your company profile to be the length of a novel. But, if it’s intriguing enough it can be on the longer side.

Stories give context. If they’re good, they allow the reader to see the world through someone else’s eyes. You can obviously see the potential benefits of telling a story in your business plan company description.

Maybe you don’t think that your company’s stories are all that interesting. That’s all right. It doesn’t have to be the greatest story ever told, as long as it’s authentic.

4) Highlight your inspiration

This is slightly different than telling a story.

Here, rather, you’re speaking on the things that have inspired you thus far in your company’s journey. You can talk about how you settled on the imagery (logo, colors, fonts) that makes your company unique. What inspired the company’s tagline?

Think about all the little things that comprise your company‘s image – how did you come up with them?

5) Utilize video

Obviously, this approach only works if your business plan is in an electronic format. If that’s the case, you can include a link from (or embed the video into) your business plan.

They say a picture is worth 1,000 words. Well, a video could be worth much more than that. Not to mention, using this unique format would make your business plan exceedingly memorable.

Of course, all the same guidelines apply for a video company profile as a written one. In fact, it might be beneficial to have a video company profile to complement your written one even if you don’t plan on using it in your business plan.

6) Utilize pictures

Maybe you think a video is overkill? That’s fine. If you want to spice up your company description, images might have the same (or even a greater) effect.

Images allow you to get creative. For every point you want to make in your company description, you can include an image that illustrates and complements that point.

Video is dynamic. Images are static. So, if there’s a particular visual that can really clarify what your business is about – an image might be the way to go.

7) Create a timeline

Time is one of the foundations of business (along with money in and money out). So, why not embrace the importance of time by formatting your company description as a timeline.

Everything in your business was decided on at some point in time. So, that makes it easy to include the must-haves in this unique style of company profile.

This format can highlight how fast you are growing and/or how quickly you’ve been able to adapt to your environment.

If you’re not keen on just using a timeline as your company description, it can still serve as a valuable illustration to complement a written format.

8) Be to-the-point

Though most of these ideas emphasize creativity, perhaps that’s not your personality. Maybe it’s not the nature of your business. There is something to be said about brevity.

So, maybe it makes sense for you to cover all the important points in a straightforward manner.

Company history? Here’s a one-sentence answer.

Products and services? Here’s another one sentence answer.

And so on…

A bare-bones business plan might appeal to some readers. It could be that they don’t want to see a flowery company description. Rather, they would appreciate your to-the-point addressing of the subject matter. You can always include more detailed information in the appendix.

Additionally, white space can be visually appealing. A minimalist approach can look good. Plus, I think it’s important not to let your company profile drag on forever. That will just seem vain and will risk losing the reader’s attention.

9) Brag a little bit

A business plan is a sales document for all intents and purposes. It exists to convince people to invest, one way or another, in your startup. So, don’t be too humble when you’re trying to sell your company’s potential.

The company description in your business plan can be a great space to mention everything you’ve accomplished thus far.

Awards, reviews, customer feedback, and anything else that provides social proof that your company is onto something great.

10) Define your new unique selling proposition (USP)

I am a big proponent of the USP. I think it’s what sets your company apart from the competition. Focusing on your USP will help your small business be more successful.

So, if you’re going to need a USP, why not clearly define it early on? Why not highlight it in your business plan?

Think about what makes your products and services better than the competitions’. Think about what would make customers choose to do business with you.

Nothing can describe your company better than singling out what makes you unique.

11) Refer to your mission and vision statements

As discussed in the mission statement post, you should have an idea of what you want from your business. Your mission statement is the driving force behind every decision you make as an owner. Or, at least it should be.

If you have an effective mission statement, you can see how it would serve as a good starting point for a company profile.

In another post on strategic planning (strategy formulation) I encouraged you to solidify your vision for your company. E.g. what your company will look like in 5-10 years. You may not have this written down, officially, as a “vision statement.” But, if you’re going through the strategic planning steps, you should have a good idea of your vision.

What you want from your company and what direction you want to take it are important pieces of your company puzzle. These pieces of information will contribute greatly to the description of your business.

Company description examples and analysis

I’ll give the same advice I did on the mission statement post…

If you’re still struggling with writing a company profile, it might help to look at some examples. No need to reinvent the wheel here.

Don’t copy another company’s description word for word, of course. But, there’s no harm in using a profile you find interesting as a model. By adding in the elements unique to your business, you’ll have a perfectly fine company description to work with. If you want, in the future, you can always start over to make something completely unique.

Here are some quality company profiles I found. I also included some of my thoughts. These are taken from websites, not business plans because company profiles are easier to find.

First of all, you’ll notice that Nordstrom’s company description utilizes images. Nothing particularly striking, to me. But, it does add to the visual appeal.

They also touch on a little bit of company history on the linked page. What’s notable, however, is the use of a timeline if you click on the Company History link. The Company History is a really great illustration of Nordstrom’s storied history, in my opinion.

The first thing you’ll notice about Nike’s company description is that they utilize video (in the background) and emphasize their mission statement.

Next, they highlight their commitment to innovation – what some might say is Nike’s USP. Innovation in sustainability is addressed lower on the page too.

After that, they note the people behind the products. Particularly the factors that make their team great.

Delta, like Nike, puts a video at the head of their company profile. In Delta’s case, however, it’s user-controlled. Not running in the background.

Delta also utilizes a lot of white space on their About page. This format is to-the-point but allows readers to click and learn more – if they so desire.

Like the other examples, Delta takes advantage of the opportunity to toot their own horn. Highlighting the number of customers and destinations served.

Another business plan company description example

In all of my business plan posts, I like to do more than write. I like to take part in the subject matter. However, my previous business plan post put a bit of a damper on my startup idea – a topical, all-natural hair regrowth supplement. It seems that the market might be saturated for that particular type of product.

Nevertheless, for the sake of consistency, I’ll continue to follow along as I always have. Here’s a rough draft of my business plan company profile:

Hair Regrowth Supplement Company, LLC (HRSC) manufactures and wholesale distributes an all-natural hair regrowth supplement for men and women.

The company is headquartered in My Town, USA. Product manufacturing is conducted by a third party partner in Florence, KY. Distribution to retailers is also handled by a third party partner in Prince George’s County, Maryland.

HRSC was founded by Mr. Founder in 2019 with the goal of providing a natural, topical, option for hair loss sufferers. The formula for HRSC’s prototype product was inspired by a little know article in a German medical journal published in 2008. From there, the formula has been improved several times over in an effort to increase its effectiveness and ease of application.

Mr. Founder was frustrated with the (perceived) lack of available options in the topical all-natural hair regrowth market. He wanted an alternative to FDA approved treatments with their lack of efficacy and potential side effects. He experimented with the product himself and was satisfied with the results. This prompted him to explore offering the product to the public. The existing formula offers a safe and potentially effective treatment for individuals in the early stages of hair loss. Most importantly it does so with no downside or adverse effects.

As you can see, I included all of the requisite information. I also decided to make it a bit personal and to highlight my inspiration for the company. Below the text, I might also include a picture or two of the product to give the reader a better sense of what I would be selling.

Make your company description memorable

Hopefully, you now have enough ammo to get your company profile started.

Again, you don’t want it to be too lengthy. But, you also want it to have substance.

If you find that your company description begins to look like a wall of text -add some subheadings in there. That will make this section of your business plan more readable and easier to scan. Not to mention more visually appealing.

Generally, there are three things to quantify – how often customers visit, how long they stay, and what actions they take while they’re there. Understanding this information will help your business maximize its investment in marketing.

In order to sell to customers, you have got to get them to engage with your small business. In order to sell to a lot of customers, you need them to engage with you heavily.

Therefore, it’s worth thinking carefully about measuring customer engagement. Customer engagement can happen in person, on a website, on social media, or over the phone.

Defining customer engagement is tricky. You’re likely to get 10 different definitions from 10 different people. Personally, I like to think of customer engagement as a reflection of how passionate your customers feel about your business.

If you’re going to make big efforts in the customer engagement arena – you had better make sure you’re measuring the results of those efforts. After all, you can’t improve something you’re not measuring. Fortunately, there are many metrics that you can track to see if your efforts are bearing fruit.

These metrics fall into three broad categories:

How often your customers engage?

How long your customers engage?

What actions are they taking when they engage?

What is meant by customer engagement?

Customer engagement is a term used to describe the active involvement of a consumer in a company’s product or service offering.

It’s about creating an ongoing dialogue with customers, and it takes many forms:

Customers who feel that they can influence a product or service offering (such as government services).

Customers who are encouraged to provide feedback on products/services (and whose feedback is acted upon).

Customers having ownership over their experience. This could be through buying shares in the business or other methods where customers become owners.

Here are a few examples:

Part of the Solution

People will always complain about customer service. However, if you look around, there are ample examples of brands making consumers part of the solution. This happened in a big way in the airline industry after 9/11. Airlines needed to improve service or face losing customers.

In many cases, they brought in the consumers by holding town hall meetings as part of the solution. Customers aired their grievances and were rewarded for constructive criticism with better service.

Crowdfunding

In other instances, consumers raised money via crowdfunding sites like Kickstarter to fund development projects of products that had not yet hit the market.

It is interesting how companies are trying to get new technologies out there by using Kickstarter so people can test them before buying them. For example, this was used on the Amazon Echo when Kickstarter backers got a special price to buy it.

Marketing Strategy

In other cases, companies have co-opted the customer as part of their marketing strategy, which is a modern twist on word-of-mouth promotion.

For example, a recent campaign by clothing company Patagonia encouraged customers to return their older jackets via a special box they created, with every returned jacket being recycled into new materials for future use.

It’s an attempt to stop ‘fast fashion’ where many clothes are cheaply made and only worn once before being discarded. The campaign essentially told consumers: “you can help us make better products, and we’ll reward you for doing so.”

It’s also interesting how companies rely more on word of mouth or ‘buzz’ where they give discounts to people who talk about their products.

How often are your customers engaging?

One of the biggest mistakes that small businesses make is doing too much (or not enough). There is a good spot in-between and it depends on what type of business you have, how often you offer your service, and who the customer is.

A prospect that visits your business and then disappears is a lost opportunity.

If a prospect visits your business and becomes a customer – that’s valuable, of course.

If that customer keeps coming back – that’s the most valuable of all.

It’s from the repeat customers that you get the most bang for your marketing buck.

If customers keep coming back, you can assume that they feel as though they are getting value from your product or service. The more often they come back, the greater the value. Customers that engage daily are generally worth more than does that do weekly or monthly.

Applications such as Google Analytics will tell you how frequently (potential) customers visit your website. If you sell your products/services in-person or over the phone then gathering customer information might help you to understand customer engagement. Rewards programs might also help here too.

How long are your customers engaging?

Customers who receive high value from your products and services are not only going to visit often but they’ll stay for longer too.

Again, there are many options when it comes to software that measures user frequency and activity time for your website. Activity time is not as easy to measure for a brick-and-mortar business. If most of your customer activity is over the phone, it might be that you have records that can give you some insight. Or, it might be the sort of thing that you can log into your CRM software

In-person, this can only be practically measured through observation. Therefore, the results will be anecdotal. However, if you commit to measuring this information, insights can be gathered. It might be that you need to group customers by demographics when measuring.

What actions are your customers taking?

A company cannot think about every possible customer, product, and context interaction. However, no business should forget to get basic information from customers.

Customers who come often and stay a long time are positive indicators, certainly. But, ultimately you need those customers to take action. The ultimate action you need them to take is to make a purchase.

If your business is online, you can measure what pages customers visit, if they opt into marketing communications, if they abandon their cart, plus a multitude of other things. For a brick-and-mortar business, as usual, it’s not so easy.

A brick-and-mortar business that only deals with customers over the telephone could only really document what the customer said. Speaking is really the only “action” customers can take. For example, what products did they inquire about? What other questions did they have?

For a retail (in-person) business, again, you probably have to group customers by demographics.

I read a book on this subject once. Unfortunately, I can’t remember the title. Anyhow, it was about a guy who built a consulting business by documenting customer actions.

He would go into a retail business and take notes of the actions that the customers typically took in the store. He would also measure the amount of time they were in the store.

Armed with this information, he would then approach the retailer and offer to sell it. The information he gathered would speak volumes about customer actions and habits. Much of the retailers’ responses revolved around repositioning merchandise in the store.

If you’re a retail small business owner, you don’t have to approach this as scientifically as the author of the book did. But, you can do something similar. It’s just a matter of setting aside the manpower. Discreetly watch the actions that customers take in your store and document it. Plug the data into a spreadsheet or some other software where you can interpret it. Then, take the necessary actions.

Below, are some ideas on customer actions that you can measure. Many are similar across all three mediums. Others, with a little tweaking, might be applicable in another medium.

Website/Online

In-person

Phone

Visiting your website

Visiting in-person

Calling your business

Viewing/clicking an ad

Referencing an ad

Referencing an ad

Downloading document

Taking a flyer

Returning a call

Opening email

Asking for assistance

Making a purchase

Requesting more information

Making a purchase

Requesting more information

Viewing webinar

Accepting assistance

Completing a survey

Visiting online store

Joining rewards program

Accepting solicitation

Making a purchase

Applying for financing

Contacting live chat

Referring customers

Completing a survey

Leaving a product review

Rating a product/service

Reordering a product

Challenges to measuring customer engagement

Marketers measure customer engagement by email, social media, website traffic, and purchases. But they often forget to include service metrics.

As you might have gathered from the previous sections, measuring customer engagement isn’t always simple.

Sometimes, collecting data is logistically difficult. Such as documenting what actions your customers are taking. Other times the information is hard to quantify and interpreting actions can be very subjective.

Ultimately, you want to measure customer engagement to understand how it will affect your revenue and net income. But, making the connection between actions and revenue can be difficult. Don’t lose sight of your ultimate goal – which is to build a healthy small business.

What do you do with customer engagement data?

Collecting and analyzing customer data will help your marketing campaigns. It also lets you improve the customer experience, like by giving people better product recommendations, communicating with them more often, or even making sure that they stay loyal to your company.

Once you’ve gone to the effort gathering customer engagement information, what then?

It may be that, in the beginning, you simply want to understand how your customers are engaging with your business. But, there will come a point where you want to act on the measurements you gather.

At which point, you need to be clear on what it is you want to achieve.

Do you want to increase the frequency of customer engagement?

To get more out of your marketing dollars?

Or, do you want customers to take different actions?

You can get even more specific. For instance, do you want to sell more of a particular product/service to a particular customer avatar?

You might find that you need to start using different customer engagement metrics in order to meet your more lofty goals.

What it all means

Measuring customer engagement is important for maximizing your marketing ROI. It’s also closely tied to your conversion funnel – turning leads into customers.

Therefore, even nominal efforts in measuring customer engagement can go a long way toward helping your small business.

How would you, personally, define customer engagement?

I would define customer engagement as any interaction that happens between a consumer and the brand across multiple channels during the customer journey. The whole idea of customer engagement is not only selling but also to have continuous engage customers through their lifecycle. Having a solid customer engagement strategy is vital for delivering a conversational experience.

What are some ways brick-and-mortar businesses can track customer engagement?

Some ways the brick-and-mortar businesses can track customer engagement are:

1. Store visits – It includes the number of transactions per month

2. Spend per visit (basket size) – Refers to an average $ size per transaction

3. Product spend – It indicates the revenue by category, upsell, and cross-sell rates

You can set a CSAT survey to track your store experience based on the score by asking ‘how satisfied were you with your most recent experience?’

What should a business do once they’ve gathered customer engagement data?

Once the data is collected the data, businesses can proceed with the following steps:

1. Segment the data based on your target audience and product category to understand how your customers are spending.

2. Identify your value in terms of your product positioning and identify the gaps to align your products to your target audience.

The weighted-average inventory turnover ratio for all retail is 8.0. Different types of retail businesses have vastly different inventory turnover ratios, though.

What does inventory turnover tell you? What do you do with the information? It can take a company years to determine the appropriate quantity of a product to hold in stock. Too little means your consumers don’t get what they want. Too much means you ‘re wasting precious storage space and your money is not working for you. Without a doubt, your product turnover is indeed a major part of the inventory management process.

Before we delve into the specifics, let’s go over some inventory basics.

What is meant by inventory turnover?

Inventory turnover, sometimes know as stock turn, is a calculation of the frequency of sale of a particular product in one year. In essence, it answers the question – “how many times did you sell all of your inventory?”

Inventory turnover can be measured by item, category, or (most commonly) in aggregate.

It is usually measured annually but can be calculated on a quarterly or even monthly basis too. Why annually? Well, a product is not sold in the same manner throughout the year. There is seasonality. Many products will experience peaks and valleys in sales over the course of a year.

So, measuring inventory turnover annually allows you to get a more comprehensive view of the issue. A comprehensive view of any situation will allow you to make more sound decisions.

What is the inventory turnover ratio?

The inventory turnover ratio is a numerical representation of your company’s inventory turnover.

The formula for calculating inventory turnover describes the sales of a particular item, compared to inventory held, over a specific period.

In simpler terms, it helps you to see how fast each product is selling out. Understanding how frequently every item in stock is sold, can improve your operations in a variety of ways, some of them include:

Comparing your business to a benchmark (competition)

Calculating inventory turnover for retail business

The formula used for determining retail inventory turnover is:

Inventory turnover = cost of goods sold (COGS) ÷ average inventory

The term “average inventory” is noteworthy because, at any specific time, the value of your inventory can drastically change. It can be disproportionately high at one point in the year and disproportionately low at another. Thus, in order to reflect precise and accurate figures, an average is used in the calculation. Using average inventory to calculate stock turn will yield more accurate results.

To be honest, average inventory is approximated. It’s not necessary or practical to figure the average based on day-to-day or hour-to-hour levels. Rather, you can add the beginning-of-year and end-of-year inventory dollar values and divide by two. Alternatively, you can use the highest and lowest month-end inventory dollar values. It doesn’t matter which you use, as long as you’re consistent.

What exactly is a “good” inventory turnover ratio for retail?

A retailer, like every other business, always seeks to grow its sales and consequently its profits. In order to do so, a retailer has to utilize the inventory space it has.

There is a fine balance between having too much product on hand and too little. As mentioned previously, too much inventory is costly. Too little inventory probably means you are compromising on sales.

A good inventory turnover ratio for retail is a subjective thing. It depends. Retail encompasses a lot of different types of businesses. Here’s how I went about answering this question.

First, I found a good article with turnover ratios for different types of retail businesses. Source.

Then, I referenced Census data to find the number of establishments in the U.S. for each type of retail business. Source.

Then, knowing the number of establishments for each type of retail business, I was able to come up with a weighted-average inventory turn ratio for retail businesses.

Here’s what that looks like:

Retail Business

NAICS Code

# of Establishments

Inventory Turnover Ratio

Weighted-Average

Womens clothing

448120

32,941

4.3

.55

Jewelry

448310

21,300

1.4

.12

Shoes

448210

24,716

2.4

.23

Pet supplies

453910

9,997

6.2

.24

Furniture

442110

23,615

3.5

.32

Sporting goods

451110

21,422

2.7

.23

Supermarket / grocery

44510

64,938

14.7

3.74

Beer, wine, liquor

445310

34,510

6.2

.84

Hardware

444130

15,031

2.8

.16

Baked goods

311811

6,915

57.5

1.56

TOTALS

255,385

7.99

In general, you could say that turning inventory over 8 times (7.99 rounded) is average for retail. “Good” might be considered anything above and beyond that.

That won’t really tell you much, however. As you can see by the table, the inventory turnover ratio varies wildly depending on the type of retail business. The range goes from 1.4 for jewelry to 57.5 for baked goods!

If you’re really astute, you’ll probably notice a correlation between the inventory turnover ratio and what the retail business sells. The more durable the products, the lower the turnover. Cost and shelf life also play a part.

So, the real answer to “what is a good inventory turnover ratio for retail?” is “what is the average inventory turnover ratio for your type of retail business?”

But, that comes with an important caveat!

What also must be asked is “how many times did my business stock out and lose sales?”

Because, if you’re losing sales, a high inventory turnover ratio doesn’t mean much.

Be sure to keep things in context.

Interpreting retail inventory turnover

You might think the greater the inventory turnover ratio the better. However, there are some exceptions. You could be purchasing goods in lower than ideal quantities, which will eventually lead to higher shipping costs and out-of-stock goods.

A low inventory turnover ratio can mean poor output from your sales team or a decrease in your products’ popularity. Perhaps your prices are too high. Or, maybe you’re not marketing properly. Whatever the reason – it translates into products remaining too long on your racks. Storage costs can be high, and they continue to pile up as inventory goes unsold.

Why it is important to calculate your inventory turnover?

Maybe you already actively manage inventory turnover and are looking for strategies. Or, maybe you’re new to the concept and are interested in the benefits that management can bring to the business. Either way, if you own a retail store, it’s important that you monitor this metric.

Here are some of the benefits of measuring inventory turnover in your retail store.

You are financially better off

If you are looking for one KPI (key performance indicator) for your business, inventory turnover is it.

The calculation is valuable if you look for financing from banks too. Since inventory is always set up as security for a loan, companies want to make sure that the product is easy to market and can be converted into cash quickly.

You’ll make better business decisions

Closely managing stock turns allows you to make better purchasing choices. Then, you’ll only keep the storage space for the products that are actually selling. Hence reducing your storage costs, which, in turn, allows you to be more flexible on price.

Some of the decisions that can be made using inventory turnover ratio include;

Which products need to be purchased

If the ratio is too high for a specific item, that could be an indicator that a particular product should be ordered more often. Is it stocked out a lot?

What units must be moved

Inventory turnover may indicate when certain products should be given better “real estate” in the store.

What needs to be scheduled in advance to provide plenty of flexibility

By understanding the frequency of an item that turns annually, you can plan better to avoid stockout situations.

Once you have a proper control over your product turnover, it gets easier to tackle the aforementioned situations quicker

You’ll likely develop a system or process that facilitates more efficient inventory management.

As a retailer, it is important to ask yourself whether your products are turning faster or slower than they were last year. If so, why?

Has the expected level of sales changed? Do your inventory management processes need to be tweaked?

Inventory turnover has a huge impact on your retail business

Remember, inventory (no matter what type) is the same as taking cash and placing it on a shelf. If it just sits there, it does you no good.

Inventory turnover is a relatively simple thing to measure and it can have a huge effect on your retail business’s success. If you’re not currently managing inventory turnover in your retail business, consider doing so.

If you know the price of something, you can calculate the cost that will give you a 30% margin as follows: Cost = Price × 70% (1 – margin %).

In business, the very existence of an enterprise is determined by its profitability. Making a profit can be an elusive process, requiring a good understanding not only of the Cost of Goods Sold (COGS) but also the functions performed to sell the product or service.

There are many models that help define costs so that profit margins can be properly calculated. Choosing the best model is critical to establishing proper pricing levels. The math involved in calculating a 30%, 40%, or 60% margin isn’t the difficult part of the process. It is determining the right starting point that requires the most scrutiny and clarity.

Easy to Say But Hard to Do

The first thing to consider is – have all the relevant and pertinent costs been included in the final cost calculation? This is where many companies become confused and the process of determining costs can become quite complex.

Unless the true costs of a product or service are known, any calculation related to profit will not be accurate. This failure to incorporate all relevant costs could end up costing a company dearly.

It’s All About the Budget Baby!

Putting together the costs associated with a product/service includes much more than the obvious costs (material, labor). These are the beginning point for the calculation, but there are other areas that should also be included in the formula. Consider the following:

Invoice Amount

Does the invoice include any discounts for early payment or penalties for late payment? Those numbers should be included in the costing formula.

Handling Costs

If the item is delivered or picked up, there will be a separate cost involved in its transportation. There are also the costs associated with handling the item after its receipt like inventory and warehousing expenses.

Cost of Money

Products that sit on the shelf for an extended period of time have company money invested in them that is not producing at income while it is tied up in inventory. This is known as an opportunity cost.

Taxes

Like death, taxes are inevitable and the costs involved in paying taxes on inventory or property held at the end of a tax year can add to the product’s true cost. Inventory that turns quickly isn’t as much of a concern as inventory which takes a long time to get sold or used.

Overhead

This is always a loaded question with an explosive answer. What is overhead and how should it be allocated? Calculating overhead accurately is a science unto itself. Determining how to allocate it can be problematic at best.

Fudge Factor

Also known as “budget override” or “other costs.” This is an amount added to other costs to make sure nothing is left out of the calculated amount. In most cases, this is an additional 2% to 5% to help cover any unexpected changes.

Add It All Up and It Spells True Cost

The cost of acquisition, handling, overhead, and other considerations have been added up. A final total true cost has been determined. Now what?

With all that formulation and processing, the resultant number is one you can have confidence in. Now that we’ve looked over what the true costs are we can finally multiply it by 30%, 40%, 60% and there’s the sales price. Right?

No.

Markup is not the same as margin. But, more on that in a bit.

Price is what determines margin

Knowing the true cost is the first step, but now it’s time to look at the selling side of the equation. Here are some other factors to consider:

Cash Flow

Is the product or service sold and paid for immediately or does it go on an account for 30 days or more? Are there discounts offered for prompt payment or pre-payment of invoices? Will the buyer earn volume discounts for large orders or is a discount earned over time based on volume?

Associated Costs to Deliver

Sales programs offering free freight or trips to Hawaii for sales associates are additional costs that should be estimated when determining overall profitability.

Negotiation Protocols

Some companies state their prices and no one challenges those prices; other companies state a price but they know the customer will be negotiating the price based on different issues. Allowances should be made to include any fluctuations involved as a result of negotiating the price for the product or service provided.

After-sale Follow-up

Once the product or service has been delivered the costs associated with the transaction aren’t done accumulating. After-sale follow-up by customer service, warranty expenses, and product administrative costs like safety notifications or updates add up quickly and should be taken into account.

Inflationary Issues

Not all inventories are subject to inflationary conditions but many companies find themselves confronted by the costs associated with wider economic issues. Issues that could alter the costs of inventory or services. Construction, manufacturing, and many other industries are constantly facing changes in local, regional, and national economic conditions that affect their business at its most basic levels.

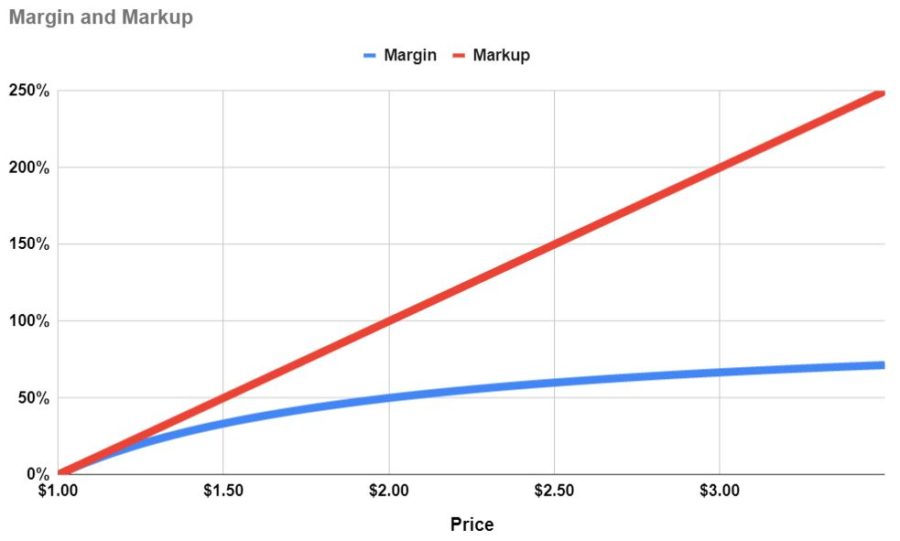

Margin vs Markup

These are two terms that are often mixed. They are similar (even sound similar!) but they are not the same.

Margin can only approach 100%. Markup can be an infinite percent.

Markup is based on cost. It is calculated by dividing profit (gross, operating, or net) by cost.

Say something costs $1.00. If it’s marked up 30%, the price would be $1.30. If it’s marked up 60% the price would be $1.60.

Margin is based on price. It is calculated by dividing profit (gross, operating, or net) by price.

Say something costs $1.00. If it has a 30% margin, the price would be $1.43. If it has a 40% margin, the price would be $1.67.

Price = Cost ÷ (1 – margin %)

Here are some more comparisons of margin and markup:

Price

Cost

Margin %

Markup %

$1.00

$1.00

0%

0%

$1.43

$1.00

30%

43%

$1.67

$1.00

40%

67%

$2.50

$1.00

60%

150%

$3.00

$1.00

67%

200%

$4.00

$1.00

75%

300%

Click to enlarge

Retail, Wholesale, or Manufacturer – The Rules Still Apply

So, is a 30%, 40%, or 60% margin good?

It depends.

It depends on whether you are talking gross margin, operating margin, or net margin. It also depends on the industry and business model you are referring to. Every business and industry is different. What’s good and what isn’t can only be determined when comparing to an appropriate benchmark.

Some industries work with high profit margins and others work on minuscule margins.

Regardless of where an organization stands in the supply chain, the need to maintain profitability is important. Advanced accounting methods combined with software that can quickly search through data to extract the most important information makes the process of assigning costs much easier and much faster.

However, the need to incorporate all salient costs and related expenses can become burdensome and overly detailed if not monitored for accuracy and applicability. Traditional models have been replaced by highly-customized programs that reflect the conditions of individual companies rather than using industry-wide standards for calculating costs.

Protecting the Margin

Knowing the true and detailed costs of a product or service is critical in a competitive environment. If margins start to slip, most businesses will go to their suppliers looking to save money and maintain profit margins by asking for discounts. Or, they might take other cost-saving measures.

Any Way You Cut It, Margin Still Matters Most

The discussion over the difference between the terms “margin and “mark-up” are arguments over the same thing – profit. Unless an organization is a non-profit, its goal is to make a profit and to do so for as long as possible.

Net profit is often called the “bottom-line” and it still defines an organization’s character and capability to many. Every financial analyst, stockbroker, and business columnist focuses on a company’s ability to not only generate a profit margin but to do it repetitively and under a variety of conditions. Knowing the numbers and figures that determine the actual costs for a product or service leads to the opportunity to produce the desired margin more readily and realistically.,