NAICS codes can be used to perform market research on businesses. The information you gather from NAICS market research will help you, as a small business owner, to make confident decisions in targeting customers.

*By the way, if you’re looking for the actual NAICS code for Marketing Research and Public Opinion Polling – it’s 541910.

What is a NAICS code?

NAICS stands for North American Industry Classification System. NAICS codes consist of between two and six digits. This code is used to classify businesses by activity (what products or services it provides).

Note that the first two letters of NAICS stand for “North American.” This means that NAICS codes are also used by our neighbors to the North and South – Canada and Mexico. The NAICS has, in large part, replaced the Standard Industrial Classification (SIC) system. You might remember SIC codes if you attended business school anytime prior to the year 2000.

The first two digits of a NAICS code represent the sector of the business. The third is for the subsector. The fourth is the industry group. Finally, the fifth and sixth represent the NAICS industry and national industry respectively (Source).

Any business might have more than one NAICS code. In fact, each location is given its own NAICS code.

Why NAICS is important

The NAICS exists to efficiently compile, create, and analyze business data. Data that is collected includes employment, revenue, and inventory; among many other things.

Since this much of this data is made public by the Census Bureau, you have the ability to use the NAICS for market research. Particularly if your business currently does, or plans to market to other businesses.

Beyond market research, NAICS codes can also help your business generate leads. In order to get the contact information, you’ll probably have to purchase it from a 3rd party vendor.

How to use the NAICS for market research

The first step to utilizing NAICS is to know the code you want information on. From the NAICS website, you can search by keyword on the left-hand side of the page. Searches can be performed on current or historical NAICS information.

The search should return codes that will link to a list of example businesses. This helps you be sure that you have precisely the right code.

Credit: census.gov

Industry Statistics Portal results

Once you know the NAICS code you want to research, click on this link to be taken to the Industry Statistics Portal. After entering your code, you’ll be given links to related data sources.

Most searches will return you to to the same four results: County Business Patterns (CBP), Statistics of U.S. Businesses (SUSB), Economic Census (ECN), and Survey of Business Owners (SBO).

The CBP includes annual reports with information on the subnational level. Employment, number of establishments, and payroll data are included.

The SUSB pulls data from the Census Bureau. Most of which is in Excel format.

The ECN includes data on people, places, and businesses. Most of this data is from the Census Bureau FactFinder. If you’re technologically sophisticated, you can also pull data via an API.

Finally, the SBO can also be accessed via an API. Beyond that many of the links also end up at the Census Bureau FactFinder.

There’s a link in the lower left-hand corner of the page to Selected Visualizations. From what I saw, this was potentially interesting information about the industry in question. Furthermore, it would allow you to drill down to the state level. But, unfortunately, as of this writing, it’s a dead link.

I sent an email to let them know about it and to see when it would be working again. No response as of yet…

Market research with a NAICS code

What are some other circumstances where you would use the NAICS for market research?

Are there other marketing opportunities with NAICS codes besides lead generation?

Small businesses and entrepreneurs use demand analysis to:

Consider substitute products and services

Get input from (potential) customers

Determine what “drives” demand

Understand what variables affect demand and to what degree

Demand analysis is about challenging your preconceived notions regarding your product/service. A stress test, if you will. A demand analysis will take your idea and start molding it into something that has even higher potential.

As an entrepreneur, you can’t be too stubborn. You have to be flexible. After going through this process, the hope is that you’ll come out the other end with an even more refined idea and a greater chance at success.

Market research and competitive analysis for a business plan

This is the second post on drafting a business plan for your startup. These posts are modeled after the SBA Business Guide.

When first thinking about the market for your product/service, don’t define it too narrowly. Try to think of substitutions that you might not have otherwise considered. No, you might not compete directly with these substitute products, but the presence of substitute products will have an impact on your pricing and demand.

Pricing too high could push customers to these substitute products. Even if that pricing seems in line with your value proposition when compared to direct competitors. But, theoretically, the amount demanded changes (inversely) with the price. A higher price will push customers to consider alternatives. A lower price should result in a higher volume sold.

Further defining the market for my product

As I mentioned in my first business plan post on the topic of demographics, I am working alongside you. I have a prospective product that I would like to explore the viability of, and I am creating a business plan for this product as I write these posts. As a reminder, my potential product is an all-natural hair-thickening topical supplement.

Anyhow, in the previous post, I used “customer avatars” to roughly ascertain the size of my market. I think I was fairly liberal in that estimation. The three of my avatars that were the most detailed totaled approximately 5.2 million people. The avatar that was broader included 6.5 million people.

As mentioned above, I have to keep in mind that not all of these people will pursue hair loss treatment. Many, will just accept it as a normal part of aging. Others will choose to address the problem but will pursue an alternative treatment method to topical supplements. Some of these alternative treatment methods include:

Obviously, there’s no shortage of alternatives to my prospective product. However, many of these treatments are ongoing and the potential exists for customers to combine them.

After listing these potential substitutions, it dawned on me that there are a couple of different classes of hair loss. I would probably target individuals that are in the early stages and are merely looking for help to slow down and, hopefully, somewhat reverse the initial effects of hair loss.

Another thing that dawned on me when researching substitutions is that it might be a mistake to only consider men when ascertaining the market for this product. Most of the results I found when searching “hair loss treatments” were articles targeted at women.

As I said, I’m taking this journey right along with you. So, I’m refining my idea and picking things up as I go along.

Gathering survey information for your business plan demand analysis

The next steps are mostly statistical. That might give you pause if numbers aren’t your thing.

I really do wish I could provide you with the handiest spreadsheet imaginable to manage the information you find. There are just too many variables, though. Different surveys asking different questions. Not to mention, every industry is going to address unrelated topics. I just couldn’t figure out how to make a one-size-fits-all tool.

What we’re going to do is compile whatever relevant statistical information we can get our hands-on, and interpret what we find. You can input this information into your own spreadsheet if you like

Statistical information, hopefully, can be obtained from a simple internet search. “[your topic/industry] survey results”, or something similar should yield some useful information. If you can’t find relevant info, then you might have to reach out to industry trade magazines or organizations.

As far as how much survey information to collect – there’s no clear answer. It depends, first and foremost, on the abundance of such information. If there is plenty available, then I guess I’d recommend collecting it until you’re tired of doing so. You can always circle back around and search for more specific results if you need to in the future.

What to focus on

Right now, focus on demographics information, substitute product information, and information about motivation (drivers).

This is where having it in a spreadsheet will come in handy. With the numbers in a spreadsheet, you can combine survey information and break it down as needed. Check out my example below to see what I mean.

Click to enlarge

Survey information about my product

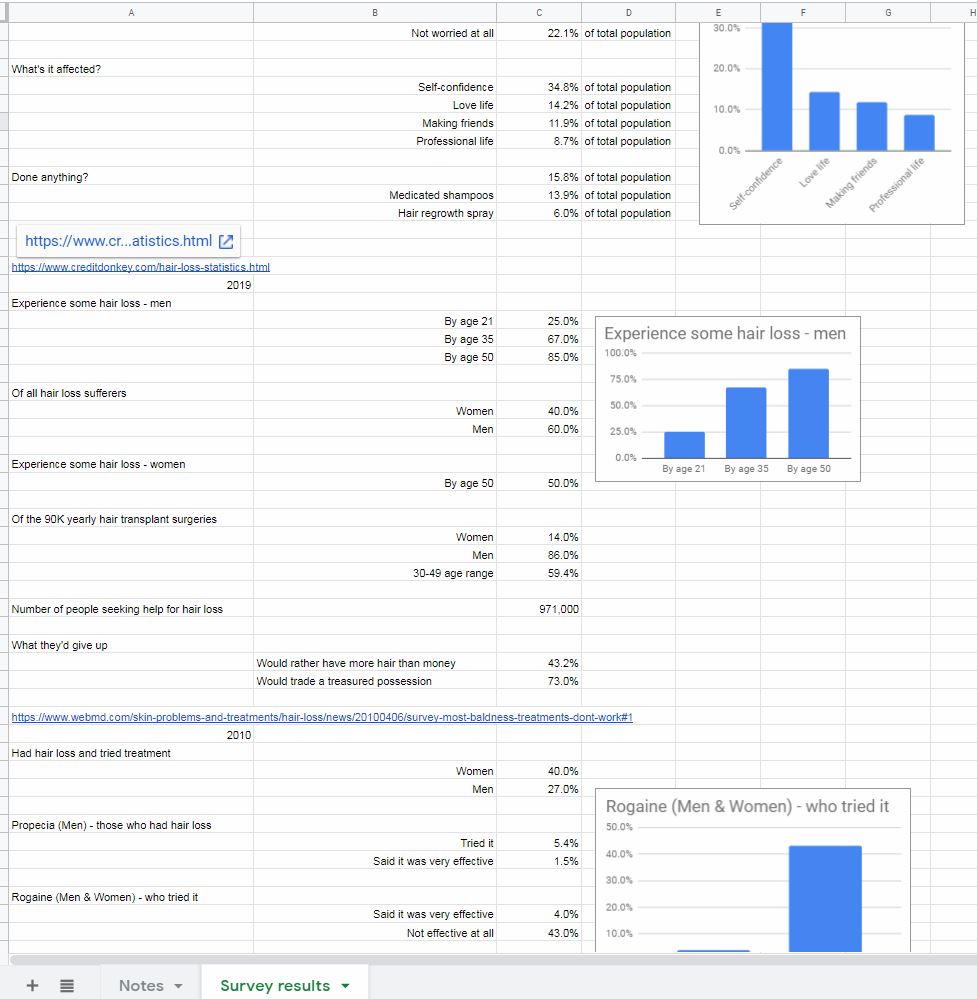

There was no shortage of survey results regarding hair loss. In fact, I grew tired of collecting information well before I was able to read it all.

I must admit, I learned something on this step. I learned that it probably makes more sense to do this research before creating customer avatars rather than after.

This research showed me that hair loss in women is a considerably more prevalent problem than I knew. So, I should definitely not exclude women when trying to calculate the size of my target market. Additionally, I learned a lot more about the age that hair loss starts to affect men and women. Not to mention, a lot of other interesting tidbits related to marketing and substitute products.

I simply typed the figures I found into the cells and tried to organize it in a somewhat easy-to-read format.

To make this information as useful as possible, I also included a link to the survey – in case I wanted to reference it again. Also, I thought it would be useful to make note of the year the survey was conducted. That way, I could note trends, if any existed.

Finally, to top it all off, I put in some charts. Charts can help to illustrate ideas in a way that numbers can’t, sometimes.

Now, I have a nice little foundation of data to build my business plan off of. I also know that there is plenty of other information out there if I want to delve further on a specific topic.

Divide total industry demand into its main components.

Now, you want to start to organize the information you found in a logical manner.

First, isolate the information related to demographics or that which otherwise describes your potential customers to you. You want to break this information up so that you can get an idea of what your potential customers might look like. You should, hopefully, begin to see customer “avatars” take shape.

Yes, I asked you to create avatars in the previous post. As I said above, that was probably premature. It would make more sense to create the avatars with this survey information, then use the census/demographic information to estimate the size of the market based on what you found.

Live and learn…

After you have the demographic information in good order, move on to the “solution” information – if available. This is information that specifies how customers are solving their problem(s) now.

If you’re lucky, this information will join seamlessly with the demographic information you organized above.

Start with the simplest questions (those with the fewest variables) and expound from there.

What if my survey data is inconsistent?

You might run into a situation where you have conflicting information. Or you might find yourself in the fortunate situation where different surveys seem to corroborate the same statistics.

If your information sources don’t jive, you have a couple of options. First, you can move forward with the information you deem to be the most trustworthy. Or, alternatively, you can average what you found. This works well if the differing results are relatively close together. Finally, you can choose to use the data source that is most recent – particularly if your industry is especially dynamic.

All of your numbers aren’t going to jive up perfectly. However, at this point, you are armed with a lot better information than when you started. Better information will ultimately lead to better decisions.

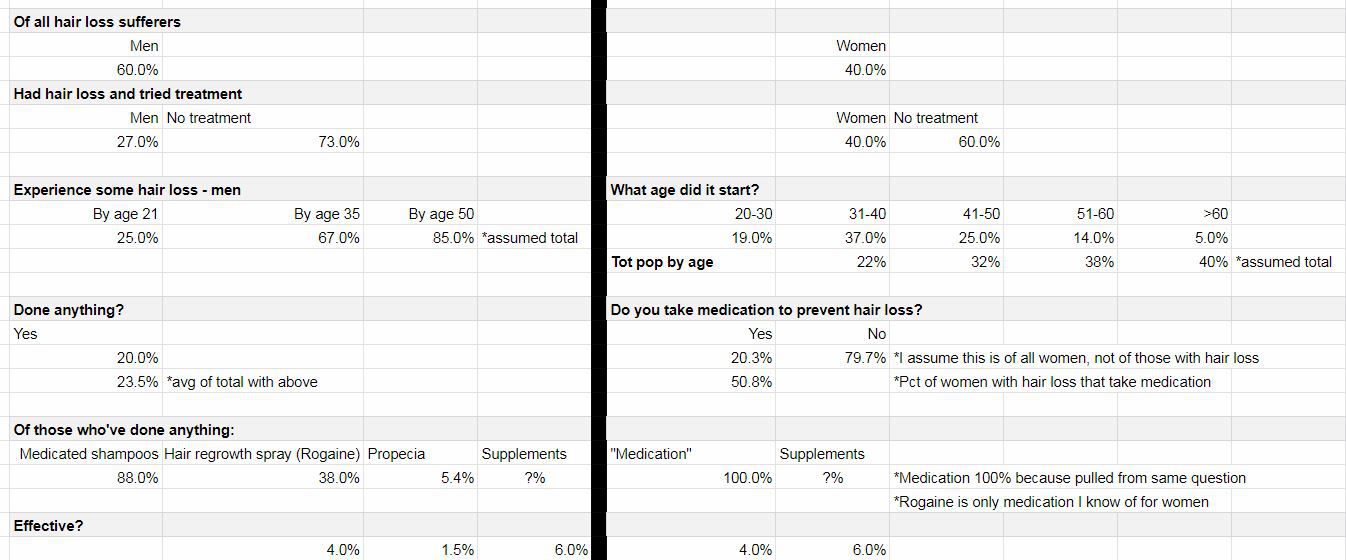

Industry components for my product

Demographics

For my part, I like to start simple and divide my demographics based on the variable with the fewest options. In this case, the simplest variable only has two choices – men and women.

From there, I used information that I found regarding the percentage of men and women that have had hair loss and have tried treatments.

Next, I break things down further based on the age that men and women started experiencing hair loss. I was fortunate to find information for both genders.

That’s the extent of demographic information I was able to obtain. I would have liked to have found some information regarding income or socioeconomic status. If that information proves to be critical as I move forward with my business plan, I’ll have to circle back around to see if I can track it down.

Once I felt good about my (revised) customer avatars, I moved on to “solution” information.

Again, thanks to the abundance of information I was able to find, I found similar questions for both genders. The first question was the simplest. It asked if the person with hair loss had done anything to address the problem.

From there, I had a couple of survey questions that explored the alternatives that hair loss sufferers had tried in the past. Additionally, I found results that gave insight into how effective these alternatives were.

When all was said and done, I had the groundwork laid for the ability to know how many potential customers I might have, their demographics, what they have tried so far, and how well those alternatives had addressed the issue at hand.

Here’s what my worksheet looks like after sorting my information into industry components:

Click to enlarge

Business plan demand analysis of drivers

Hopefully, in your search for survey results, you came across some information that provided insight into the “why people buy” question.

In particular, we’re looking for drivers of sales here. Specifically, what circumstances compel a customer to buy your product/service (or a substitute)? Hint: people usually buy to solve a problem. To avoid pain, not seek pleasure. Or, so I’ve been told…

Insight into what compels your customers to buy will not only be valuable in the drafting of the remainder of the business plan but in all your marketing efforts once you are up and running.

The information about who your customers are (from the previous step), why they buy, and what steps they are currently taking to solve their problems (also from the previous step) will hopefully paint a clear picture for you. A picture that will guide you to a point where you can position your strengths in a manner that will help other people’s weaknesses.

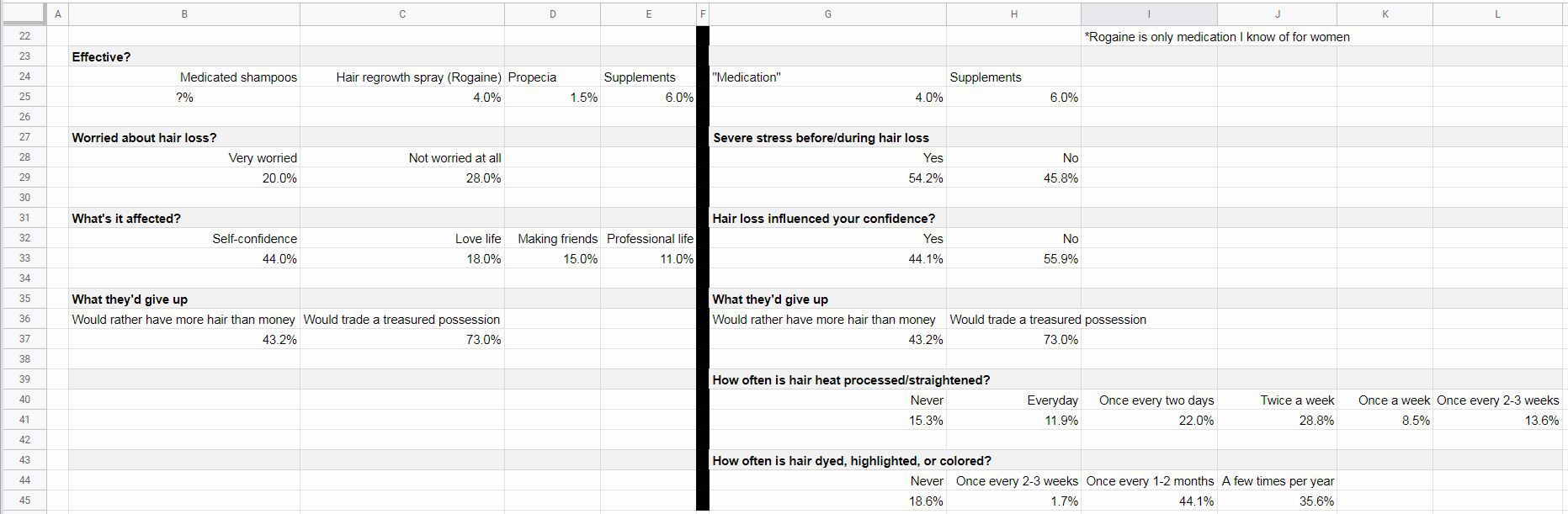

Understanding the drivers of demand for my product

Again, I was fortunate to have an abundance of survey information to draw from. A couple of my surveys not only touched on how hair loss made people feel but also on specific actions that they had taken before the hair loss started.

This information tells me an angle I can take when marketing my product, plus where a lot of my potential customers are going before they start to experience this problem. That place…the hairdresser.

Of course, that’s for women. Though there’s no rock-solid proof that it’s hairstyling that is contributing to hair loss in women, there is enough correlation to make a compelling case. For men, on the other hand, hair loss just seems to be the hand that most are dealt.

But, before we get into that, let’s look at some of the emotional drivers that might compel customers to purchase a topical hair loss supplement…

Drivers for men

On the “men” side I got information about how “worried” men were about hair loss. This told me that most men were, at least, “somewhat” worried about hair loss.

Beyond that, there was valuable information about how hair loss had affected them negatively.

Finally, the most valuable information, to me, was a question of what they would give up to solve this problem (men & women). The answers were encouraging for someone who was hoping to build a business in this industry. Almost half would rather have more hair than more money. Three quarters would give up a prized possession for more hair.

While I acknowledge that I’m not marketing a guaranteed cure to hair loss, that tells me that people are willing to try anything to fix this problem. As I know from my market segmentation analysis, supplementation works for about 1 in 17 people. Not great odds, by any means. But good enough, I hope, to at least try a new product. Especially when the ingredients are all-natural and offer no downside.

Drivers for women

About half had stress prior to experiencing hair loss. That’s a coin flip. It doesn’t mean that the hair loss was caused by the stress (though it surely didn’t help). But it provides insight into what women are feeling prior to and while they are experiencing this problem.

I also included the “What they’d give up” question on the women’s side of the analysis because my source for that information didn’t specify either gender. Plus, it seems feasible that women would feel the same or even stronger. It’s my opinion that society values female attractiveness above male attractiveness.

Finally, we get down to the brass tacks. A potential cause-and-effect situation for the problem I’m attempting to address. The number of women that are currently experiencing hair loss are also (possibly) straightening/heat processing or getting their hair colored on a semi-frequent basis.

This tells me that hairstyling might play a part in a lot of women’s hair loss (this goes back to the pressure to be attractive thing). Therefore, I should consider marketing my product in salons and other establishments that focus on women’s hair.

There’s still a lot of analysis to be done. But, two steps into the process of drafting my business plan, I feel a lot more confident about my understanding of the environment.

Here’s a look at my spreadsheet with the driver information included:

Click to enlarge

Business plan demand analysis of sensitivity

To this point, the goal has been to make assumptions and get answers. We want to have a better understanding of the environment in which our business will operate. Hopefully, you feel that you’ve accomplished that.

But, we don’t do ourselves any favors by lying to ourselves.

Lying?

Well, yes. But probably not willingly.

You start off excited about your business idea. So excited that you decide to take the first step (something that the vast majority of people won’t do). You begin to write a business plan. You can feel your idea taking shape. You’ve already refined your idea a bit and feel that by the time this whole exercise is over, there’s no way you can fail. You’ve got momentum and your confidence keeps increasing.

That is all very good. Confidence is key. But, if everything looks rosy, you might be blind to a risk that could put your baby in jeopardy.

So, I don’t want to be a killjoy. But, for the sake of our businesses, let’s take a step back and play devil’s advocate. We need to ask ourselves some tough questions and challenge our assumptions. If we can rise to these challenges, and address them with confidence, our chances of success are that much greater.

Go back through your segmentation and demand drivers and think critically about this information. Some statistics might be a given, without much wiggle room. Others might be misrepresentative of reality. In these instances, tap into your inner cynic.

Make notes of what the worst-case scenario might look like. If you’re using a spreadsheet, like me, maybe use a different colored text. Address things like survey questions that might have been misinterpreted or alternative explanations for results.

Don’t get too down-and-out here and don’t dwell on this step too long. You don’t have to necessarily plan what you would do if these worst-case scenarios came to be. You just need to imagine them so that when the time comes for serious planning, you can take these risks into consideration.

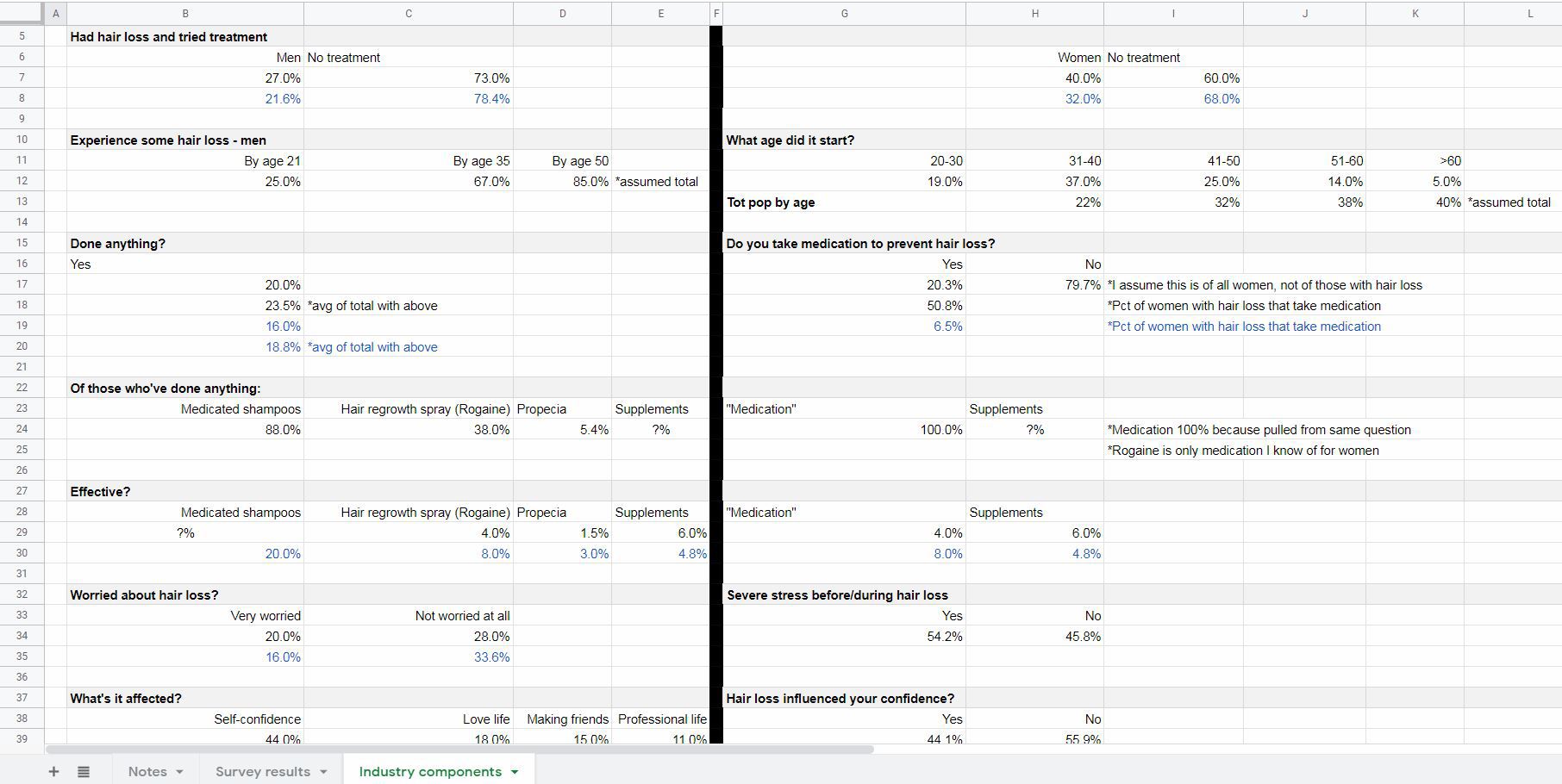

Demand sensitivity for my product

Demographics

I think my categorization by demographics is pretty safe. It’s rather well established how many men and women experience hair loss. The only thing that I might tweak is the number of men and women who have had hair loss and tried treatment. I lowered those estimates by 20%. It could be that the respondents’ interpretation of “treatment” is to comb their hair a different way or to shave their heads rather than to buy a product to battle hair loss.

Furthermore, what if the number of people that have “done anything” is lower? What if I misinterpreted the question for women that asked: “Do you take medication to prevent hair loss?” Maybe it was 20% of women who actually had hair loss rather than all women? The effect of that would be dramatic.

Substitute products

What if the alternative treatments were more effective than I’ve been led to believe? It could be that the respondents only consider “effective” to be a restoration to a full, thick head of hair? Also, just because they consider them ineffective, it doesn’t mean that they’ll stop using them. They might think that all of their hair will fall out if they stop (which could work in my favor, though). Perhaps they were overly optimistic when it came to supplements? It could be that supplements gave them other benefits, but didn’t make their hair loss any worse – so they considered them “effective.”

Drivers

Could it be that fewer men are really “(very) worried about hair loss” than I’m led to believe? Are more are “Not worried at all?” Plus, it might be that those who are only “somewhat worried” aren’t motivated to do anything about it.

As far as confidence (love life, making friends, professional life) goes, it might be that that hair loss is a contributor to low confidence, but not the primary driver. Maybe they’re overweight or socially awkward and that’s why they lack the confidence they desire?

As far as “what they’d give up” it could be that the respondents were primed by the hair loss questionnaire to be more self-conscious than they usually are. If it came down to it, perhaps not so many would be willing to part with valuables to solve this problem.

Finally, as far as hair styling being a cause of hair loss in women, it could be that I am wrong. Maybe hair styling has no effect on hair loss. Or, maybe women overestimate how often they heat process or color their hair. It only feels like every day/once every 2-3 weeks. When, in fact, they do it a lot less often.

Okay, that’s enough pessimism. It seems unlikely that every worst-case scenario would be true. But, there’s probably a mix in there between my initial interpretations and the not-so-great ones.

This exercise should help me going forward to make realistic forecasts and assumptions. Which, in turn, should help me be proactive to some of the challenges I might face.

Here’s a final look at my spreadsheet with my worst-case notes in blue:

Click to enlarge

Business plan demand analysis

This step takes a little bit of thought and a decent amount of research. This is done to give you a deeper understanding of the market you hope to compete in and the customers you hope to sell to.

What other steps would you have taken to refine estimates of demand?

Do you think my demand sensitivity was rational? Or, was I taking it too easy on myself?

Sorting through demographic information is one of the first steps in doing market research and competitive analysis. This is stuff you’ll need to know in order to prepare an effective business plan. Without this information, you, as a founder, don’t know if there is a sufficient market to support your business. You will also be starting off at a disadvantage when planning other aspects of your business.

**Note: this business plan demographics guide was written just before the Census Bureau changed its primary portal for data from the American FactFinder to Data.Census.Gov.

Download a free copy of the workbook used in this post

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

Keep in mind that this workbook is only designed to work with table S0201, Selected Population Profile in the United States. Any other table might not be in the correct format.

About these posts

This series of posts was written to convey my take on how to write a business plan. My intent is to follow up with several more posts after this one.

I’m using the U.S. Small Business Administration (SBA) Plan your business guide as my outline (link). In true SpreadsheetsForBusiness.com fashion – I plan to include free downloadable spreadsheets where appropriate.

Rather than just recycling the same information you could find elsewhere, I’m going to take this journey with you. I’ll be building my own business plan as I write these posts. This is my first business plan, so you’ll be learning right along with me.

My business plan

My plan is based around a hypothetical business that will manufacture and market a hair regrowth product for men (and women, I suppose). The plan is to manufacture the product with all-natural ingredients.

What are business plan demographics?

Sorting through demographic data for your business’ potential customers is the first step in understanding what type of person (or business) might be interested in your product or service.

It can provide an unofficial ceiling to the number of customers you might expect. It’s from this information you can get into more detail about demand, market saturation, pricing, and so on.

Common demographic information includes:

Gender

Age

Race

Income

Education

Marital status

Employment status

Geographic area

Why worry about business plan demographics?

Focusing on marketing to specific individuals helps you plan with clarity. The saying goes: “you can’t please all the people all the time.” By not trying to market to everyone a little bit, you can focus your efforts on creating a really good experience for some people.

Whatever your business is, it probably is a reflection of yourself. Your interests and talents, that is. Who you market to will also depend on your characteristics and preferences. So, as you choose the demographics of your avatar, consider who you identify with and would be comfortable marketing to.

How to find and analyze business plan demographics

The market for a product or service is quantified by the number of people who make it up and the total amount of money they spend. We can quantify the size of the market by segmenting people based on their demographic characteristics

Of course, since most of this information is numerical, I’ll be using a spreadsheet to keep track of what I found and what changes in variables mean for the market of my aspiring business.

Also, I’ll be using online resources for the sake of time and simplicity. Theoretically, market research could involve things like focus groups and surveys. That’s more involved than I want to get for this idea, so, I’ll stick with the free information.

The SBA has a nice list of resources for market and competitive analysis here.

Demographic information

Here, we’re just looking for basic information about the people who I might be selling to. For instance, how many people are in the age range that I would market to? How much money do they make? Are they single and looking to mingle? Or, are they in committed relationships and proud of their bald head (like a certain “old man” I used to know and miss very much)?

Here, you can find Census data about your state, city, or even zip code. Not every business is going to be nationwide. Some, like a restaurant, will be very local.

Also, if your business will market to other businesses (B2B), then the information contained here may or may not be pertinent to you. Try another part of the Census website called the Small Business Edition (link) if you’re not finding what you need.

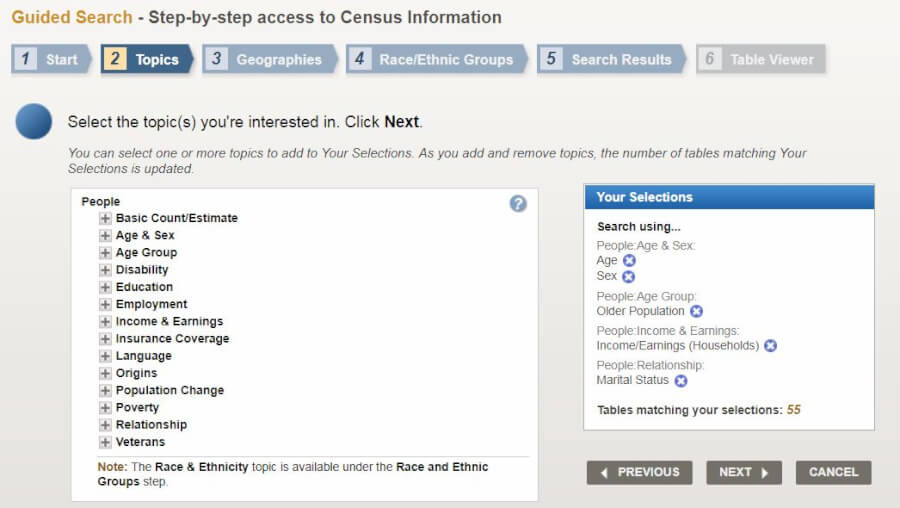

Since, as of now, I envision my business being nationwide (at the very least regional), I chose to use the “Guided Search.” From there, in the “Topics” section, I chose to look at information pertaining to age, sex, age group, income/earnings (households), and marital status.

I can always delve into more detail or retrieve different information at a later time. My hope is that this gets me started.

Click to enlarge. Credit: factfinder.census.gov

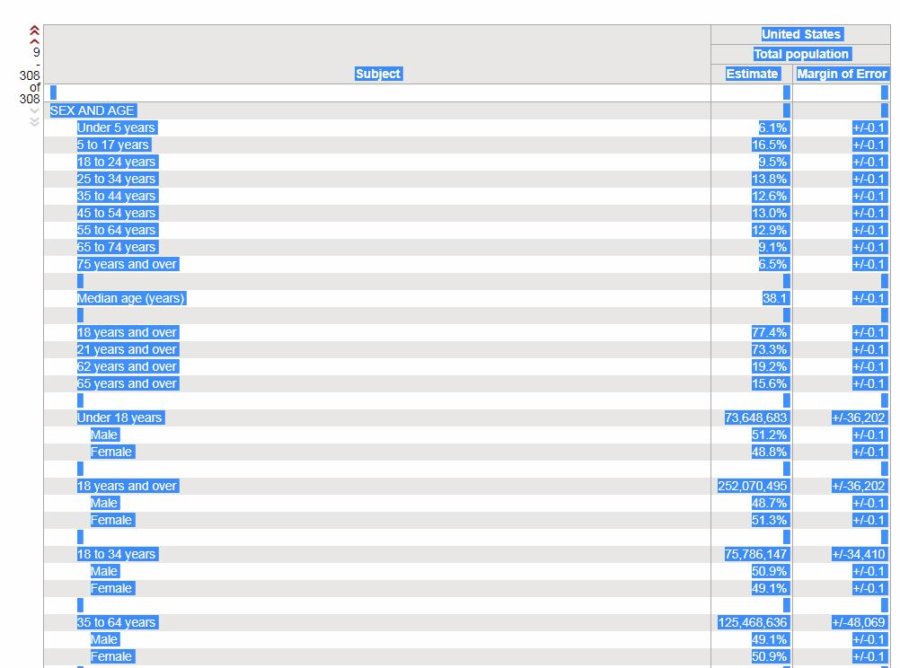

Additionally, on the next screen, I chose to break the information down by region. I included all regions so that I could total them for a view of the entire country.

Finally, on the last screen, I opted to see the one table that outlined this information in 2017, the latest year available.

Don’t bother with the “Download” Action. It will give you your data in a different format than it is displayed.

Click to enlarge

Instead, just highlight everything in the FactFinder table and copy + paste it in a spreadsheet.

Click to enlarge Credit: factfinder.census.gov

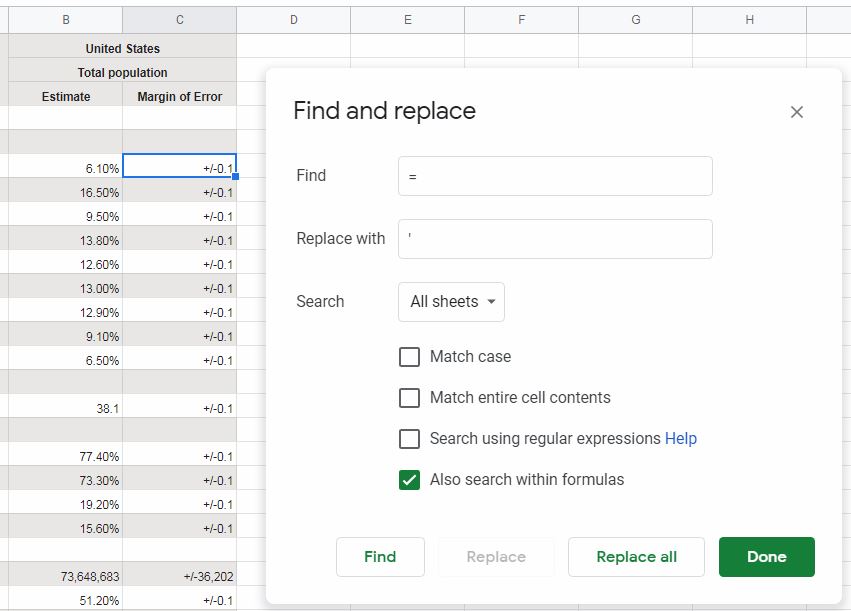

Fixing errors

From there, do a Find and replace in your spreadsheet to get rid of the errors that are a result of a “=” being placed in front of the “+/-.01” in the Margin of error column. Replace the “=” with an apostrophe. Be sure to Also search within formulas.

Filtering for the demographic information I need

My goal here is to get a range of the number of potential customers based on a set of demographic statistics. I have a lot more information than I need, so let’s see if we can widdle this down into something more useable.

To do this, I added some columns to the Demographic Info worksheet.

First of all, I added a column (Estimate #) that aimed to translate some of the percentage population information into quantities. The format of every download from FactFinder isn’t going to be the same. But, an attempt was made to give you access to both percentage and quantity information for each line item.

Additionally, you’ll find a column named Enter 1-10 to rank demographics. Here, you’ll be able to rank demographic information and narrow down your market on the Pick Demographics worksheet.

Maybe you have a couple of different mixes of demographics in mind. That’s fine. Once you are satisfied with one mix of demographics you can highlight the information on the Pick Demographics worksheet, then copy and paste the values (Ctrl + Shift +V) into one of the boxes on the Customer Avatars worksheet.

This allows you to keep tabs on several different customer profiles as you move forward with your business plan.

Keep in mind, this is just the first step of the business plan. The whole point of a plan such as this is to be proactive. In order to be proactive, you’re going to have to be flexible.

If, as you move along through the steps, you reconsider your target demographic – that’s fine. Just circle back and refine your avatars and make adjustments to other parts of the plan as necessary. Don’t get discouraged if you have to do this. That isthe whole point of this exercise.

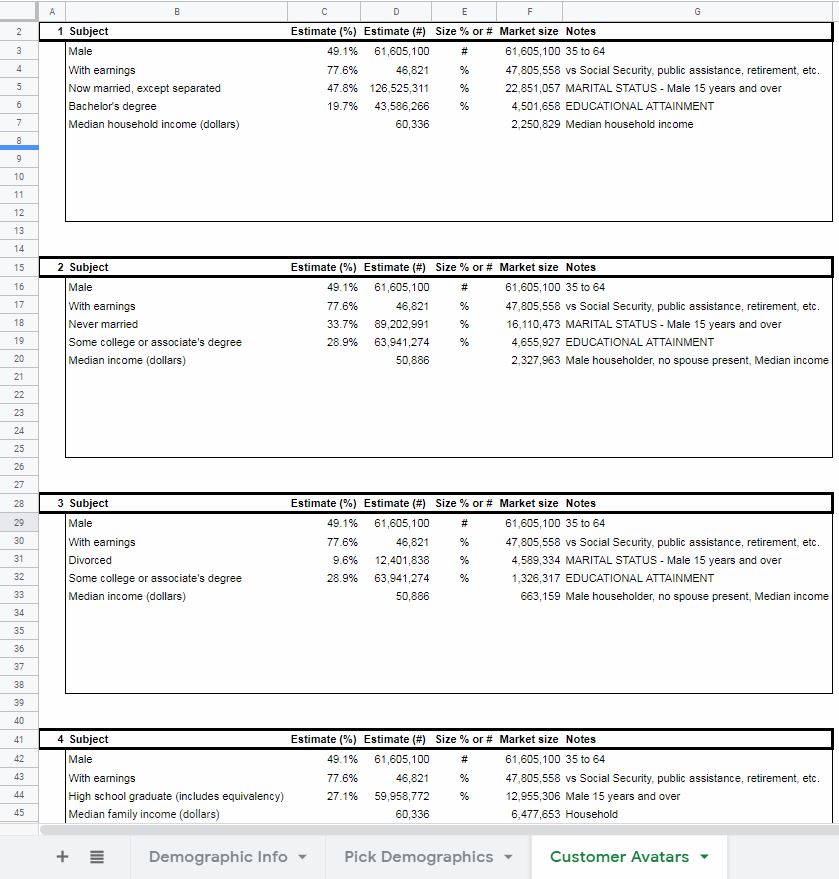

My avatars

For my avatars, I created four, relatively similar mixes of demographic characteristics.

Gender and income

All include males. Though females can also suffer from hair loss, I am assuming that males would be the primary customer and who the majority of marketing would be geared toward.

Next, every mix of demographics included individuals with earnings as opposed to those with retirement income, with Social Security income, or any other type of public assistance.

Right now, I anticipate that this product would be sold at a premium price due to its uniqueness and all-natural ingredients. This would mean that customers would likely need to earn above-median incomes in order to be in a position to buy a product such as this. Assumptions such as this might change as I progress through this business plan.

In three out of my four avatars, I made assumptions about the relationship status of these men. The demographics included were Now married, except separated, Never married, and Separated. These were my three main avatars.

Education

The fourth included Males, With earnings, and who were High school graduates. This is my “catch-all” avatar. The real total addressable market for my product is probably between this population and the total of the three mentioned above.

The main difference between the three main avatars had to do with education. I assumed that men who were single might be more likely than married men to purchase a product such as this, I lowered the EDUCATION ATTAINMENT to Some college or associate’s degree.

Defining a target market with business plan demographics

Be sure to download your own copy of the workbook used in this post. Just fill out the form at the top.

What other sources would you use to find demographic information for your business plan?

How about the avatars? How would you have screened them further?

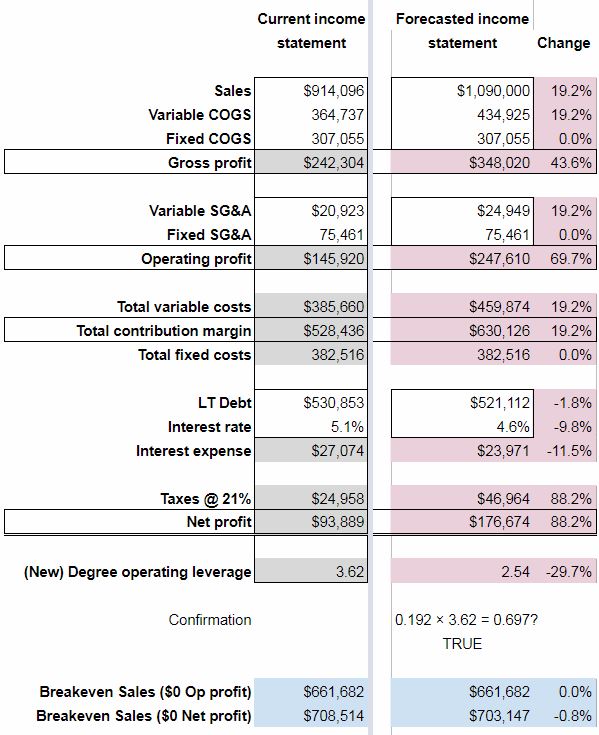

Businesses use operating leverage to keep costs fixed when they expect extraordinary sales volume. Keeping costs fixed means that businesses can carry more of that revenue to net profit.

The degree of operating leverage is a formula used to calculate how much operating leverage a business is employing. This formula tells you what will happen to operating profit when revenue increases or decreases.

The degree of operating leverage can be calculated two ways.

The first calculation looks at past costs:

Degree operating leverage = % change in Operating profit (EBIT) ÷ % change in Sales

If you don’t know your cost mix (variable vs fixed) then you don’t know how it’s affecting your small business. You don’t know if it would be advantageous to change the mix. And, if you did, what would happen. You don’t have a complete picture of your business and, therefore, aren’t making fully informed decisions.

Download the operating leverage workbook

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

Degree of operating leverage and fixed costs

Operating leverage is the use of Fixed costs in order to amplify changes in Operating profit due to a change in sales.

Fixed costs might be considered risky because they do not change no matter how much you produce. But, they also don’t rise if you produce (and sell) more. The risk and reward go hand-in-hand.

The degree of operating leverage is a ratio that tells you how much your Operating profit will change due to a change in Sales.

For instance, if your degree of operating leverage is 5.0, then a 10% increase in Sales will translate into a 50% (5.0 × 10%) increase in Operating profit – all other things being equal.

Conversely, a 10% decrease in Sales will translate into a 50% decrease in Operating profit. The pendulum swings both ways.

Which formula should you use to calculate degree of operating leverage?

You can determine your small business’s degree of operating leverage through a couple of easy calculations. Or, you can just plug your numbers into the free workbook!

Some suggest calculating the degree of operating leverage as follows:

% change in Operating profit (EBIT) ÷ % change in Sales (Source)

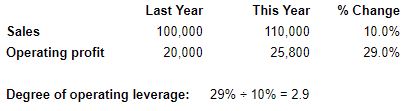

For instance, comparing this year to last year, let’s say your Sales increased 10% and your Operating profit increased by 29%.

29% ÷ 10% = 2.9. That was your degree of operating leveragelast year. This formula doesn’t tell you what it is now.

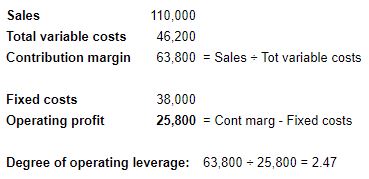

In order to calculate your degree of operating leverageright now, use the following formula:

Total contribution margin ÷ Operating profit (EBIT)

If you’re not familiar, Total contribution margin = Sales – Total variable costs. Not just manufacturing variable costs (Variable COGS), but SG&A variable costs too.

Degree of operating leverage and profit

Your degree of operating leverage can give you insight into the risks you run from your cost structure (mix of fixed and variable). It tells you how susceptible your Operating profit is to changes in demand.

It will also allow you to know how much you need in Sales to breakeven. The higher your Fixed costs, the higher that breakeven point will be.

Beyond that, it tells you if your Fixed costs are in line with your ability to generate Sales. If that ability is high, then your company can benefit from the leverage provided by Fixed costs and can earn excess returns.

Conversely, if those Fixed costs are locked into assets that won’t contribute meaningfully to Sales, then they are going to be a drag on Operating profit. You’re always going to be fighting against them.

Financial and operating leverage are similar in that they employ the use of fixed costs in order to (hopefully) amplify the effects of sales on net profit and operating profit respectively.

Here are a few of my thoughts on the subject:

Since financial leverage is owed for years to come, it is, obviously, long-term. Therefore, it should be used on long-term projects. Projects that will bring in extra revenue for years to come. Hopefully, even, beyond the point when the interest is paid off. Don’t use financial leverage for something that will provide a one-time spike in sales.

Operational leverage, on the other hand, is tied to assets that can be disposed of. They’re not very liquid assets, certainly. But they are typically a burden that can be relieved of easier than contractually owed interest. Real estate can be sold, salaried employees can be laid off. And so on…

Ironically, financial leverage is frowned upon and looked at as riskier than operating leverage. However, both essentially serve the same function. They’re components of the income statement entered at different places.

Fixed expenses can be a powerful lever or concrete boots that drag your company down. It’s all about how those fixed expenses are put to work.

How to understand and act on your degree of operating leverage

Once you know what your Degree of operating leverage is, then you will know what changes in Sales will mean for your Operating profit. If you don’t anticipate that Sales can be increased, then you’re going to have to explore means to reduce Fixed costs.

On the other hand, if you anticipate the Sales will improve next year, then you have to ask yourself if you’re willing to add more Fixed costs (that will further increase Sales). If you’re confident you can do so, you might have a really great year.

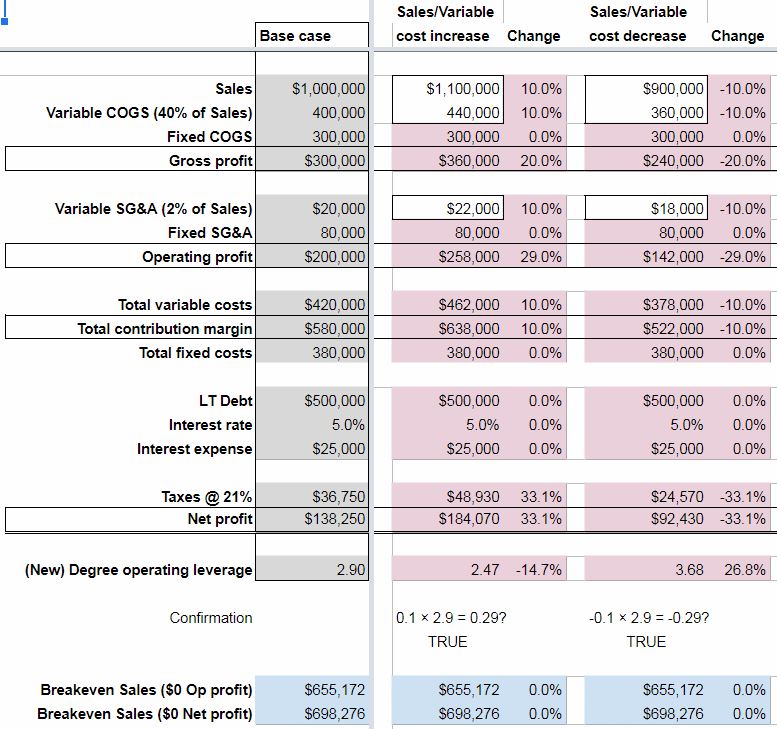

A change in sales or variable costs and the effect on a company’s financials

As can be seen on the Effects of changes worksheet – a 10% increase in Sales, Variable COGS, and Variable SG&A would translate into a 29% increase in Operating profit from the Base case. This is to be expected since the Degree of operating leverage for the Base case was 2.90 (10% × 2.90).

Keep in mind that Variable costs would increase at the same percentage as Sales – as is their nature.

The flip side is also true. A 10% decrease in Sales and Variable costs means a 29% drop in Operating profit (-10% × 2.90).

Note that the Breakeven Sales amount doesn’t change in either scenario. This is because Fixed costs didn’t change.

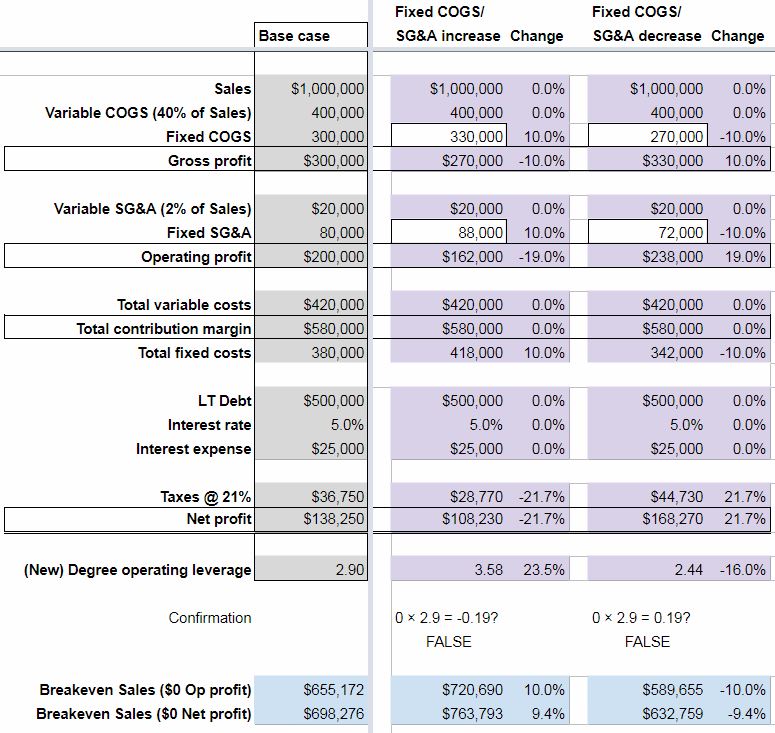

A change in fixed costs and the effect on a company’s financials

“Why would fixed costs change?” you might ask. “They’re fixed,” you say.

Well, in theory, they don’t. But in practice, they might.

First, not many costs are 100% fixed or variable. It’s a sliding scale. Over a long enough timeline, all costs are variable they say.

Also, Fixed costs are often tied to fixed assets. Fixed assets are acquired and disposed of over the years. Salaries, which can comprise a lot of Fixed costs too, fluctuate with the hiring and loss of employees.

So, as you can see, it’s not much of a stretch for Fixed costs to change.

When they do, we can see that a 10% increase in Fixed costs translates into a 19% decrease in Operating profit. Not at all what we would expect from our Confirmation equation. 0% × 2.90 = 0%! Operating profit shouldn’t change!

But in this hypothetical example, it did. And, in real life, it could.

Of course, the opposite was true too. A 10% decrease in Fixed costs meant a 19% increase in Operating profit.

Notice, too, that a change in Fixed costs meant a change in the opposite direction for the Breakeven Sales amount. Not surprisingly.

What will the degree of operating leverage tell you about your company?

Don’t forget, you can get insight into the degree of operating leverage for your own business by accessing the accompanying spreadsheet for this post. Just enter your information in the white cells on the Your degree of operating leverage worksheet.

Fill out the form at the top of this post ↑ for quick, easy, free access.

What are your thoughts on the use of operating leverage vs financial leverage?

What is your degree of operating leverage and would you like to increase or decrease fixed costs?

Financial leverage is simply the act of borrowing money to invest. This is done with the hope of earning a return on that money. A return that is greater than the cost. Often, the potential for gain is disproportionately bigger than the cost. But, the cost is fixed and will be the same regardless of the return earned. Small businesses must learn how to effectively manage their degree of financial leverage. Otherwise, they could find themselves buried under the weight of repayment.

Let’s talk about some of the advantages and disadvantages of financial leverage. Also, how the degree of financial leverage ratio can provide insight into net income.

Download your copy of the workbook used in this post

Complete the form below. Upon email confirmation, the workbook will open in a new tab.

Financial leverage advantages

Financial leverage is a strategy that can be employed to boost gains. The cost of borrowed money (typically) doesn’t change. So, if that money can be used in a way that earns returns beyond the cost of borrowing – a small business can end up way better off than it would have otherwise.

I always say that every investment comes down to three things – cash in, cash out, and time. If the cost of leverage (cash out) is low enough and the terms are favorable (time), then the cash in has the best opportunity to be big enough to make financial leverage worthwhile.

High financial leverage helps small businesses avoid dilution of earnings from the issuance of equity. It also gives them the ability to put more money to work than they would have otherwise. Both of these advantages can translate into excess returns.

Additionally, interest is tax-deductible. This lessens the tax burden that a company would realize if the same funds were raised through equity. Keep in mind that interest is a fixed cost. A fixed cost that can negatively affect a small business if operating profits aren’t high enough.

Financial leverage is a better fit for some businesses than others

On my sister site, I’ve written often about the benefits of certain business models. For businesses with the right business model, more financial leverage could be very beneficial. This is if it brings in more long-term customers. These business models are conducive to earning a good ROI on borrowed money.

Handling debt responsibly = the ability to borrow more in the future

If a small business effectively employs financial leverage, their creditworthiness improves. With improved creditworthiness, they will (likely) be able to borrow more in the future. If they continue to execute effectively, they can earn compounded returns.

The cost of borrowing (rate) could drop with a successful history of repayment. This could decrease the cost of future financial leverage. Lower cost should mean lower risk. Lower risk increases the likelihood of employing it in a successful manner.

Financial leverage disadvantages

Just as it has the potential to boost gains, financial leverage can also boost losses. Every dollar borrowed represents a little more risk. Again, that’s why the return from the borrowed monies means so much.

But, the lender doesn’t care if your small business makes 10x the cost of borrowing. Or, if it “only” makes 100% of the cost of borrowing. It expects its money back, plus interest, either way.

Borrowing money will increase your cash flow out. If the cash flow in isn’t enough to offset that, then, sooner or later, insolvency will ensue.

It all depends on the context

A lot of the negative stigma surrounding borrowing stems from the personal sector. In the personal sector, when people borrow, they often do so to buy consumer goods. Things that don’t earn any sort of return. These items actually depreciate in value. For example, cars and technology.

Nobody flinches when somebody borrows an ungodly sum of money to buy a house. This is because a house (for better or worse) is expected to increase in value.

Just as certain business models are conducive to financial leverage, others are not. Consider business models that sell time for money or one-time purchase items. These businesses will have to be confident in their financial modeling to ensure that they can earn an adequate ROI on financial leverage.

Finally, the perception of leverage depends on timing. During boom times, the companies borrowing look like geniuses. Conversely, if the economy turns against a business that has irresponsibly borrowed, then they could look foolish.

Financial leverage + operating leverage?

There are two general types of leverage that a small business can use. Operational leverage (which I plan to write about next) and financial leverage. The degree of operating leverage measures the effect of fixed costs (not interest) on operating income.

Beware compounding leverage by adding operating (fixed costs) to financial, or vice versa. This could sneak up on a small business. It could create a situation where management is caught unprepared. The result is potentially catastrophic. It’s important that scenarios like this be modeled out and planned for.

Most people understand the risks associated with borrowing money (financial leverage). The risks of operating leverage are a little more camouflaged.

Make sure you plan around your company’s (potential) total leverage situation. Annual strategic planning with an operating budget allows you to do just that.

Regulatory authorities might paint an overly rosy picture

When interest rates are kept low, the hurdle rate (minimum ROI to justify investment) is also lower. This incentivizes small businesses to take on projects that they might not otherwise. Less is demanded of investments. The pursuit of extraordinary returns might stop short in favor of quick-and-easy (but “good enough”) returns.

Also, by making interest tax-deductible, the effective cost of leverage is lowered even further. This further incentivizes small businesses to use financial leverage. Doing so could amplify any of the previously mentioned disadvantages.

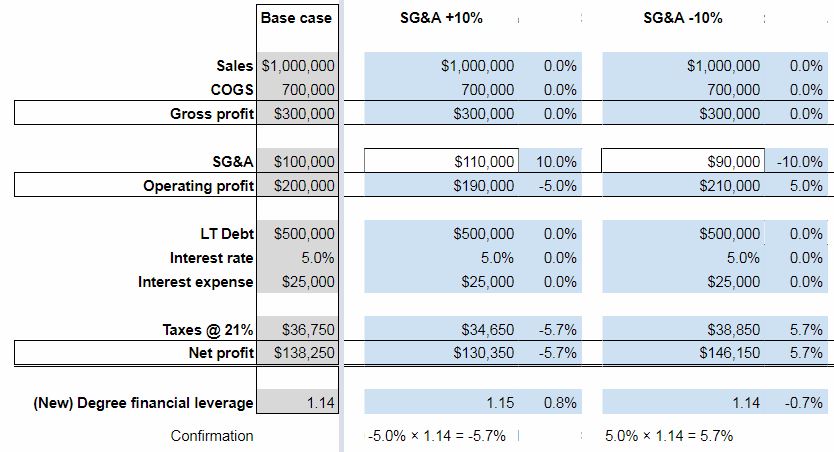

Financial leverage example

The Degree of Financial Leverage shows the amplification that borrowing money can provide to profits and losses. So, for instance, in the example operating budget, the Degree of Financial Leverage is 1.4. This means, at this level of borrowing, that for every 10% change in Operating Profit, Net profit would increase by 14% (10% × 1.4).

That sounds great, but the opposite is also true. If Operating Profit declined by 10%, then this level of borrowing would cause Net profit to decrease by 14%. That’s the nature of leverage. It amplifies gains and losses.

I created a spreadsheet to model the changes in profit due to changes in other line items. It helps to better understand how the income statement is affected by financial leverage,

I started with a Base case income statement for a small business that has $1 million in sales. This example business also has a 20% operating margin with $500K in debt at a 5% Interest rate. Its Net profit is approximately $138K.

This company’s Degree of financial leverage is 1.14 ($200,000 ÷ [$200,000 – $25,000]).

Only one variable was changed at a time. Here’s what I found:

The effects of an increase or decrease in sales

A 10% increase in Sales translates into a 50% increase in Operating profit – all other things being equal. As expected, this 50% increase in Operating profit translates into a 57.1% increase in Net profit. This is because the Degree of financial leverage is 1.14 (50.0% × 1.14 = 57.1%).

The same thing happens, in the opposite direction. When Sales drop by 10%, Operating profit decreases by 50%. Net profit drops by 57.1%.

The effects of an increase or decrease in COGS and SG&A expenses

Since COGS is less than Sales, a 10% change doesn’t have as big of an effect on Operating profit. The result is a drop in Operating profit of 35%. As expected, the resulting change in Net profit is -40% (-35.0% × 1.14 = -40.0%).

SG&A expenses, being even lower, have less of an impact on Operating profit. A 10% increase only lowers Operating profit by 5% and Net profit by 5.7% (-5.0% × 1.14 = -5.7%).

Of course, things work the same in the opposite direction. A -10% change in COGS increases Operating profit by 35% and Net profit by 40%. A -10% change in SG&A expenses increases Operating profit by 5% and Net profit by 5.7%.

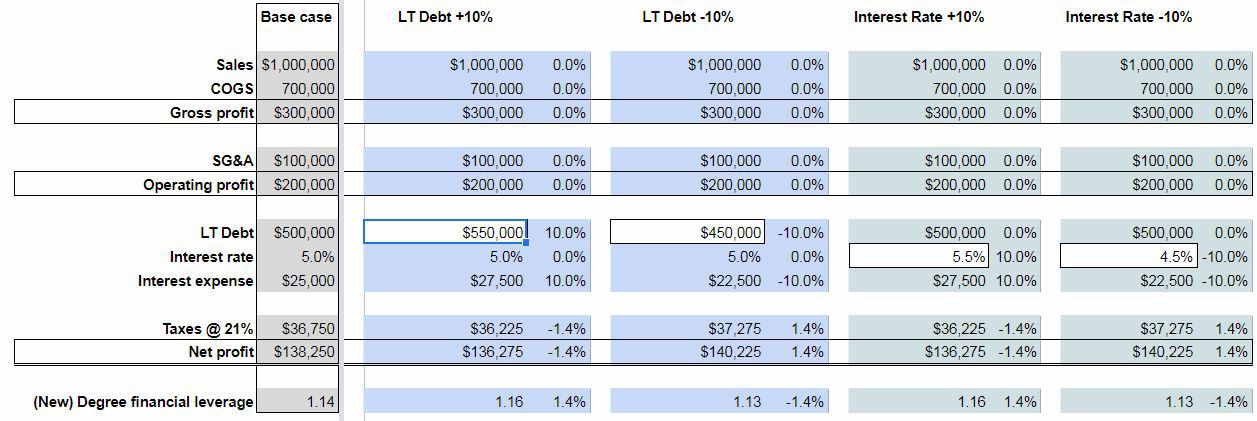

The effects of an increase or decrease in Long-term Debt & Interest rates

As shown above, changes in the income statement that result in increases to Operating profit are amplified in Net profit by the Degree of financial leverage.

But, what about changes below Operating profit? As expected, a 10% change in either the amount of LT Debt or the Interest rate, results in a corresponding 10% change in Interest expense.

This hypothetical small business carries a sizable amount of LT Debt. Still, Interest expense is still a relatively immaterial expense. Thus, the effect of a change in LT Debt and Interest rates is only ±1.4% on Net profit.

Click to enlarge

Going forward with a new Degree of financial leverage

Because of the nature of the Degree of financial leverage calculation (Operating profit ÷ [Operating profit – Interest expense]), when Operating profit increases, the Degree of financial leverage decreases – all other things being equal. The opposite is, of course, true too.

What does this mean?

It means that if your small business increases Operating profit this year, then your Degree of financial leverage is going to go down for next year. Which isn’t catastrophic. But, it means that a similar gain in Operating profit next year won’t translate into the same boost in Net profit.

To get that, your small business would have to borrow more funds.

On the same token, if your company has a decrease in Operating profit this year, then your Degree of financial leverage will increase for next year. This increase will amplify the effects of a gain in Operating profit next year. But, it doesn’t necessarily mean that you’ll end up ahead of where you would have been if you would have increased Operating profit in year 1.

Shortcomings of the Degree of financial leverage ratio

Again, the Degree of financial leverage ratio is calculated as follows:

Big companies typically borrow money through the issuance of bonds. This means that they only pay interest until the bond matures.

Small businesses, like yours, don’t issue bonds. The nature of borrowing can vary, but often, loans are repaid on an installment basis. E.g. payments consist of both principal and interest.

So, a ratio that only measures the effects of Interest expense doesn’t completely capture the impact of financial leverage. For small businesses anyways.

Two extreme examples

First, consider a small business that borrowed 10x their previous year’s revenue. If they did so at a very low interest rate, their Degree of financial leverage would also be relatively low. But, having borrowed a disproportionate amount of money, they would theoretically have the opportunity to boost Sales/Operating profit greatly.

Also, consider the other extreme. What if a company borrowed a very modest amount of money? But, was forced to pay an exorbitant interest rate? In this instance, the Degree of financial leverage would be relatively high. But, the company’s opportunity to use this leverage in a beneficial manner is limited.

Finally, in order for the Degree of financial leverage to accurately predict the change in Net profit, Taxes must remain at a constant percentage. E.g. they can’t be 21% of Operating profit – Interest expense (EBT) one year and 22% the next. The Forecasted Change in Net profit won’t equal what’s calculated in the Confirmation.

The amount of LT Debt and the Interest rate/expense must also remain constant for the “Operating profit × Degree of financial leverage = Change in Net profit” equation to work out.

So, obviously, the Degree of financial leverage has limitations. It is designed for big businesses – not necessarily small ones. It is based on amounts in the income statement, and not the cash flow statement. Thus, no consideration is taken for the effects of principal repayment.

If its limitations are kept in mind, and if reasonable changes are forecasted, then it can provide guidance on the potential benefits or detriments of financial leverage.

How financial leverage affects business decisions

Plug your small business’ information into the Your degree of financial leverage worksheet. It will help you better understand how your borrowing might help or hinder you in the coming year.

Financial leverage, in and of itself, is neither good nor bad. It’s all about how it’s employed. If it’s used to buy (rather than sell) consumable assets that provide little or no return – it’s wasted. If it’s allocated to resources that increase productivity (or earn extraordinary returns) – it’s a valuable tool for small businesses.

What are your thoughts on the use of financial leverage?

What are some of the advantages and disadvantages I neglected to include?

How about some ways that you’ve effectively employed financial leverage in your small business?

Periodic sales promotions give small businesses the best chance of boosting sales and profitability when they are carefully planned.

Care must be taken to not use periodic sales promotions as a crutch when sales fall short of expectations.

QuickBooks Online price rules give small businesses the opportunity to efficiently apply promotional pricing to products and services.

Small business owners, who are concerned about what effects sale promotions might have on revenue, can use this information to lower uncertainty

Periodic sales promotions

Weekly/monthly/holiday sales, aka periodic sales promotions, are something we’re all familiar with. The “one day only sale!” The “Memorial Day sale!” The “semi-annual sale!” Or, the most famous, the “Black Friday sale!” are all examples.

Before we get too far into it, let’s split hairs on the terminology a bit. A periodic sales promotion shouldn’t be confused with a discount or a markdown. A discount is a reduction in price for a particular group of customers. A sales promotion, typically, would apply to all customers.

A markdown is a “permanent” lowering of the price of goods in order to incentivize purchase so that they can be removed from inventory. This would be done for items that are slow-moving (or not moving at all).

Periodic sales promotions are a means of reaching periodic sales goals

Periodic sales promotions can help complement the efforts of salespeople and advertising. Whether your business markets to consumers or other businesses, a periodic sale can stimulate buying on the part of your customers.

Periodic sales promotions should compel your customers to purchase immediately. So, the nature of your promotion will have to be such that it bridges your customers’ culture with your sales goals. For example, are you trying to get customers to switch from a competitor? Or, are you trying to penetrate a whole new market?

Don’t launch a periodic sales promotion without a plan. Consider how the promotion will impact your business at different volumes. Decide what products/services should be included. Consider your best-case and worst-case scenarios so that you are mentally prepared for whatever your customers throw at you.

The upside of periodic sales promotions

Dead and slow inventory takes up valuable space. Worse yet, it ties up valuable cash. If you have inventory that is turning over slowly, you might consider how you can work it into a periodic sales promotion in order to make room for inventory that will actually sell. Doing so would be preferable to getting pennies on the dollar by discounting.

I wouldn’t offer a sale that revolved solely around dead and slow inventory, however. That might be a dud. Perhaps you might consider marking down dead and slow inventory extra – beyond the normal terms of the promotion. An example for a car repair business – a 10% off sale on brake replacement for President’s Day, with slow-moving tires offered at 40% off. Take advantage of the increased traffic to get the most that you can for the dead and slow inventory.

A periodic sales promotion might incentivize people who wouldn’t buy otherwise. If the promotion only runs for a few days, the sense of urgency could be increased. People who may only have a vague idea of what your business is about could be compelled to “check you out” while the sale is going on. Furthermore, the first-timers, if they are excited about what they found, might tell others.

Since a periodic sales promotion will hopefully bring in a lot of new faces, it’s an opportunity to collect some basic information. Even just an email address or a like on Facebook. Knowing more about your customers in general and those that were lured by the sales promotion specifically will help you to meet their needs better.

The downside of periodic sales promotions

Even the least savvy business person knows that if you sell something for less, you’ll make less profit on it. Periodic sales promotions will result in lower margins. The hope is – to make up for that with increased volume (quantities).

But, if you are able to pull off a successful periodic sales promotion, be careful not to begin to rely upon them. The siren song of a boost in sales/gross profit might prove irresistible if future sales don’t reach the levels you hoped. If periodic sales promotions are part of your strategic planning, then great. Run with it. Just don’t start using them as a crutch if things aren’t going as well as hoped.

When a customer purchases something at a reduced price, you might not be able to get a read on their future purchasing behavior. That is, beyond the fact that they’ll buy “x” amount of something at “y” price.

We’ve all heard the old adage “price, service, quality…pick two” when it comes to offering a value proposition to customers. If your business aims to excel in service and quality, but begins to succumb to the temptation to lower prices to boost sales, then you might see yourself transformed into a low-price provider – at the expense of service or quality.

It always comes down to…planning

Again, at the risk of being redundant, it all comes down to planning. Give your periodic sales promotions the thought and planning they deserve. Don’t just “knee-jerk.” Working it into a plan will give it the best chance of being successful.

Every industry is different. Every small business within an industry is different. There is no “one size fits all” solution to planning for periodic sales promotions. Nevertheless, since this website is SpreadsheetsForBusiness.com, after all, I took a stab at it.

Download the periodic sales promotion planning tool.

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

Click to enlarge

This is a very high-level workbook since it isn’t specifically made for any particular business/industry. Hopefully, however, it can give you a starting point for thoughtfully planning your own periodic sales promotion. Helping to ensure that it fits in with your strategic plan and helps your business reach its goals.

Periodic discounts in QBO

How to apply this knowledge in your accounting software, though? Well, here’s how you might go about it in QuickBooks Online.

We’ll look at periodic sales three different ways through the eyes of a restaurant:

First, an across-the-board 10% discount for everything. We’ll call it an “anniversary sale.”

Second, a 20% off of Mexican food and drinks promotion for Cinco de Mayo.

Finally, a weekly 15% off promotion for select desserts.

If you haven’t, read my previous post on the particulars of QBO price rules (levels). What follows won’t necessarily go into as much detail.

I’ll be using the sample company within QuickBooks Online Accountant. By default, this sample company is a landscaping business. For the purposes of these examples, I’ll make some changes to make the examples better reflect a restaurant business. But, if you see some odd things related to landscaping pop up in the screenshots or the video – that’s why.

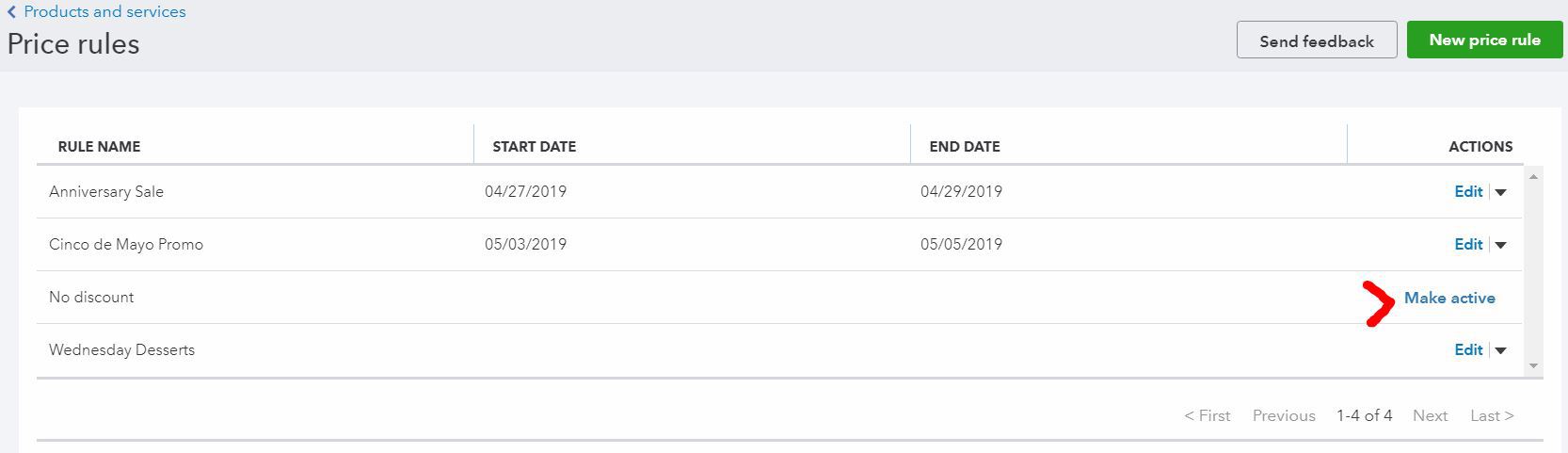

In the previous example, we created a “dummy” price rule that provided no discount. We did this so that the price rule would not be applied by default during a sales transaction. However, in this example, for our restaurant, we want it to be automatically applied so that we don’t forget to give it to our customers. So, in this case, we’ll forego the creation of a “no discount” price rule.

Click to enlarge

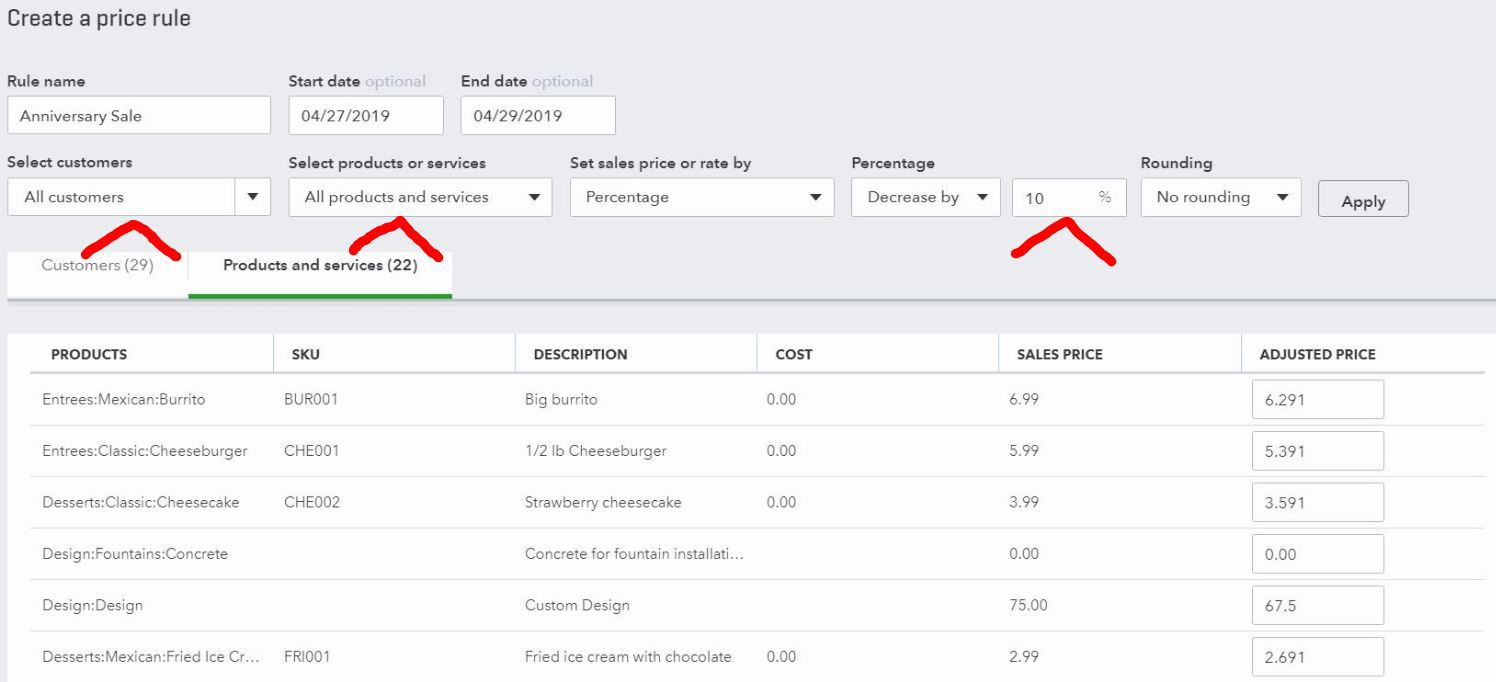

Anniversary promotion

The across-the-board 10% discount is easy to set up. In the price rules screen, we’ll create a rule called Anniversary Sale. This rule will only be in effect over the weekend of April 27, 2019.

Since it is an across-the-board discount, All customers and All products and services will remain selected by default. A 10% decrease in price will be applied.

Simple.

Click to enlarge

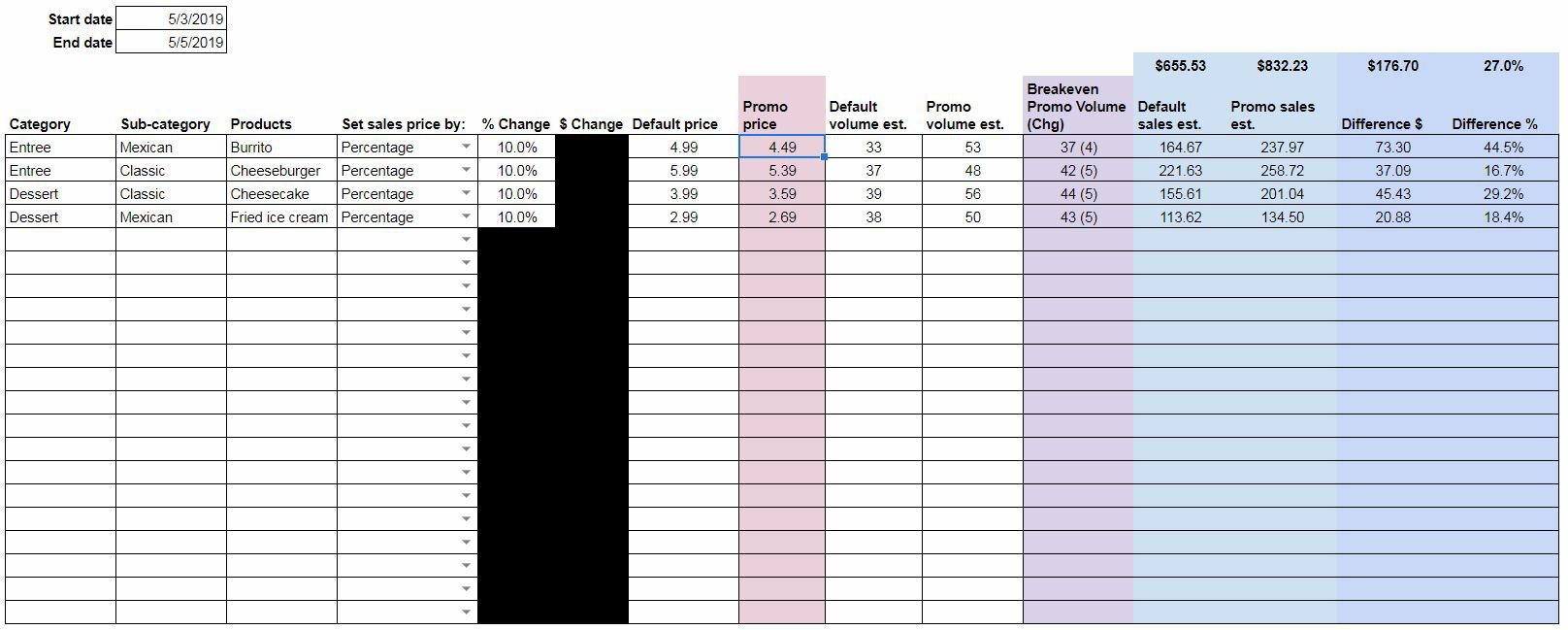

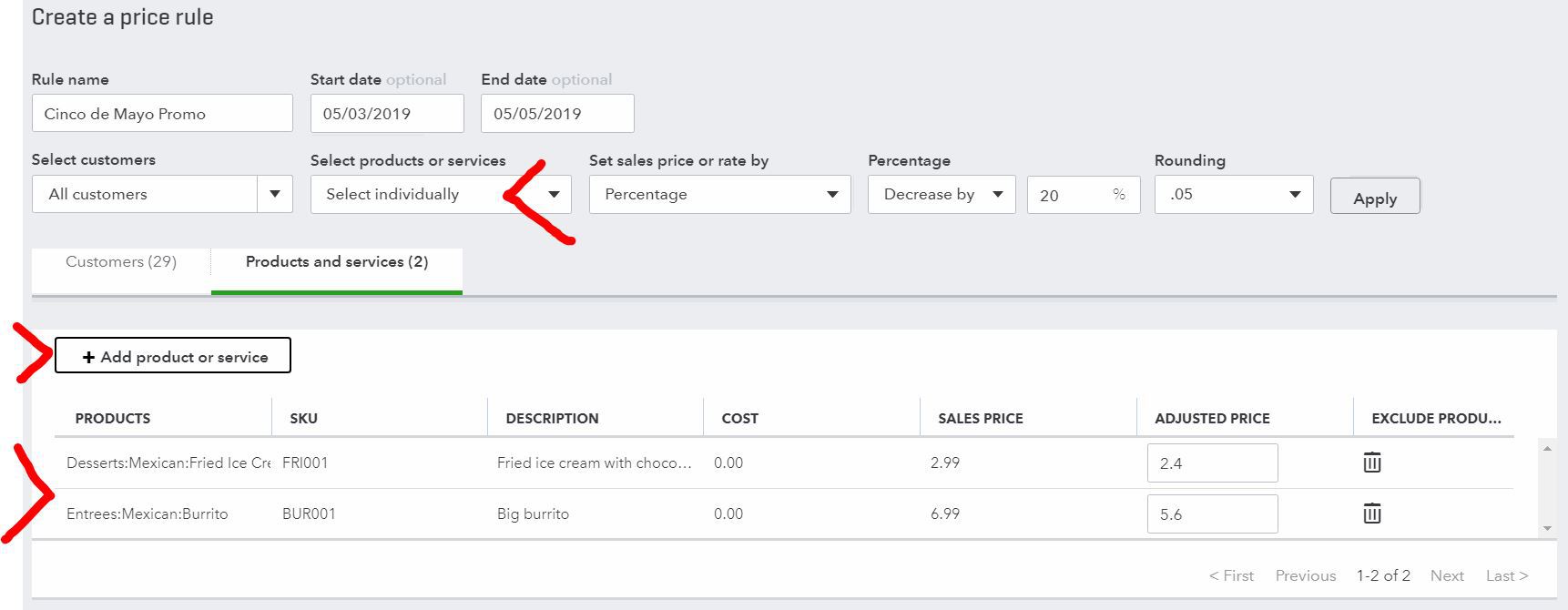

Cinco de Mayo promotion

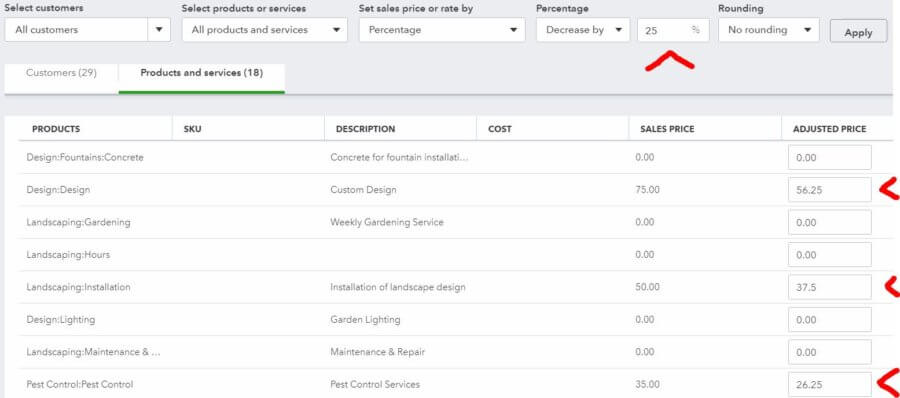

Next, we’ll look at the Cinco de Mayo promotion. In this case, it’s only our restaurant’s Mexican fare that’s on sale. Also, the sale only runs over the weekend – May 3, 2019, through May 5, 2019.

In this price rule, we selected the products in our Mexican subcategory. We then chose to decrease the price by 20%.

Click to enlarge

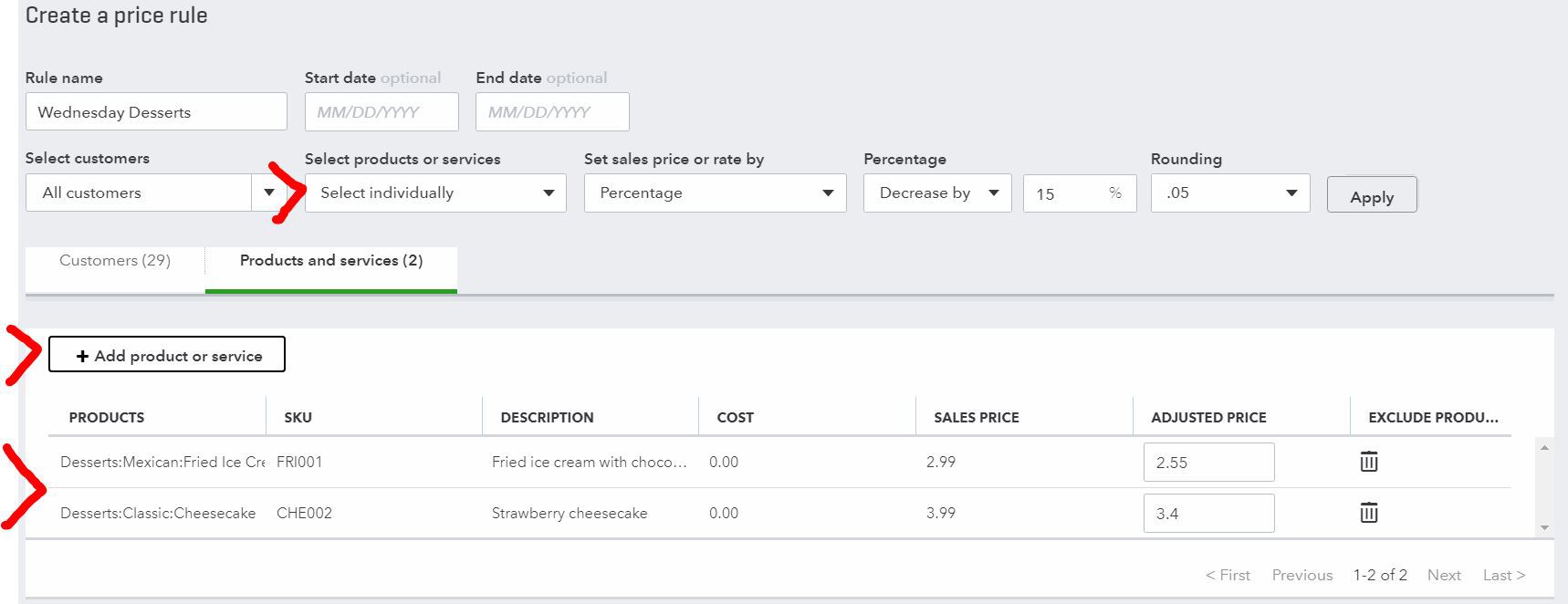

Weekly dessert promotion

Finally, we’ll tackle the restaurant’s weekly (Wednesday) discount on desserts, designed to get people in the seats during the slow mid-week time period.

This was approached in much the same manner as the Cinco de Mayo discount. Except, there is no Start date and no End date. This is an ongoing promotion. All products in the Desserts category were selected for inclusion and they were decreased in price by 15%.

Click to enlarge

Periodic sales promotions

When it comes to pros & cons, advantages & disadvantages, upside & downside posts, I always overlook a few. What are some of the pros and cons I missed for weekly/monthly/holiday sales promotions?

What other considerations need to be taken into account before a small business launches a weekly/monthly/holiday sales promotion?

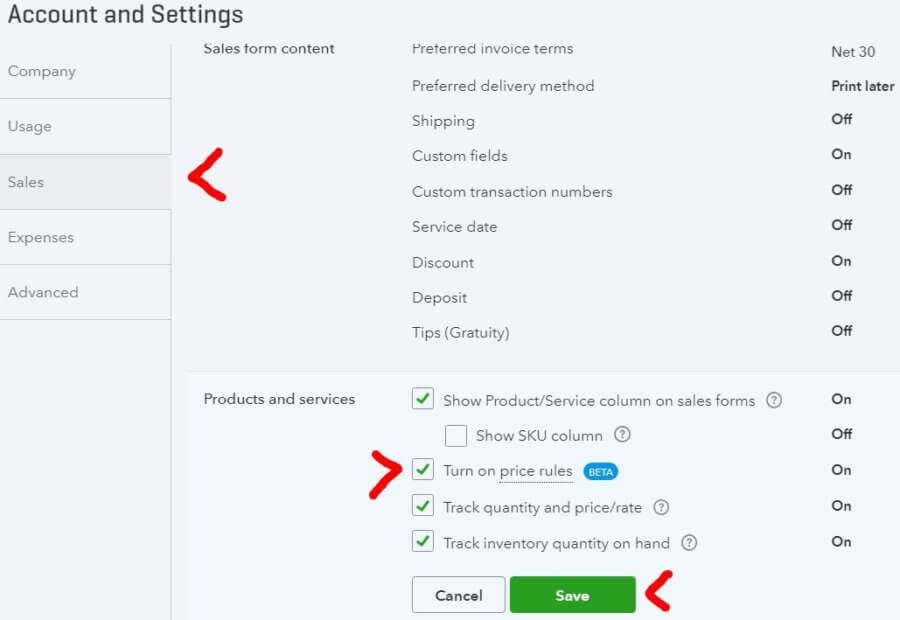

Gear (icon) > Accounts and Settings > Sales > Products and Services > Turn on price rules

To create price levels:

Sales (left menu) >Products and Services > More > Price rules

Price levels (levels) in QBO allow users to specify price changes for customers, products, or a combination of the two

Promotional pricing can help drive sales and profitability

What are QuickBooks Online price levels?

Price levels (rules) are used in QBO to quickly and easily give special pricing on particular items, and/or to particular clients. You can mix and match customers with products/services when setting up price levels. Also, you can broaden your selection to all products/services that fall within a particular category. For instance, maybe you want to only have a sale on installation and not physical products. Not every pricing rule has to be across the board.

Price levels can be set up to give a percentage discount, a fixed dollar amount discount, or… you can simply enter a custom price for a particular item.

Furthermore, if it makes sense in your pricing strategy, you can even increase prices. Plus, you can round to the nearest dollar, $.49, $.99, and many other amounts.

Finally, for each price rule, you can enter a Start date or End date to control when the rule is applied. Beyond that, QuickBooks Online gives you the ability to easily activate and inactivate a particular price rule after it’s created. Therefore, you can create price levels now, and put them into effect as needed.

Why use price levels in QuickBooks Online?

Promotional pricing is a valuable tool when used wisely. It can help small businesses drive sales and profitability. It might even be a coordinated part of your strategic plan.

Whether it is a periodic/seasonal sale, coupons, a referral program, a customer loyalty program, or a volume discount – there are plenty of reasons that you would want the ability to easily applying special pricing for specific customers and products/services.

First things first, in order to use price levels in QBO, you’ve got to turn them on. By default, they’re turned off. The option to create a price rule won’t be available if they aren’t turned on first.

By the way, in my walkthrough here, I’ll be using the QuickBooks Accountant sample company. The sample company is a landscaping business.

Go to the gear in the upper right corner and select Account and Settings.

Once in the Account and Settings menu select Sales. Under the Products and Services section, you’ll see Turn on price rules (beta). Click on that and the checkbox. Then click Save and Done in the bottom right-hand corner of the screen. Price levels are now turned on.

Creating a price rule

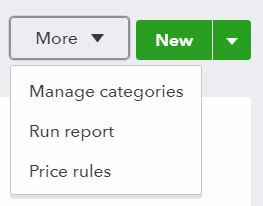

Now, that price levels are turned on, you can create one. Go to the Sales section on the left (main) menu and select Products and Services. Alternatively, you can go directly to Products and Services from the gear in the upper right-hand corner.

Once in the Products and Services screen, click on the More drop-down menu in the upper right-hand corner and select Price rules. If this is your first rule, you’ll see the little intro graphic and text. Click the Create a rule button.

Each price rule in QuickBooks Online will need a name. A rule name should be succinct, yet detailed enough for you to understand what changes it will make when it’s applied.

As mentioned, you can make effective dates (Start date and End date), if you’d like to limit the time window in which this price rule will be in effect.

Next, you’ll decide whether you want this rule to affect all customers or just specific customers. And, you’ll decide if you want it to affect all products and services, categories of products and services, or individual products and services.

After that, you’ll specify what degree you want the rule to adjust the price. You can choose to adjust the price by a percentage, a fixed amount, or you can enter a custom price. Beyond that, you can specify if you want the price adjusted up or down. Price levels aren’t just for markdowns!

Finally, you’re given the option of having your price rule rounded to a specified amount. $.05, $.50, $.88, and so on…

That’s it! Those are the only variables to enter when making a price rule. You’ll see in the table at the bottom after you click Apply, the original price (Sales price) and the Adjusted price. The Adjusted price reflects the effects of the price rule you just created. Review those changes to make sure there are no surprises. Then click Save and close at the bottom.

Using a price rule in a transaction

In order to use a price rule, you’ll have to apply it to an individual sales transaction. So, for example, if we click on Sales in the left menu. Then, click on All sales on the top menu. Finally, click on the New transaction drop-down and select Sales receipt.

In this example, I’m just using a Sales Receipt for illustrative purposes. Pricing levels can be used in Invoices, Estimates, Sales Receipts, Credit Memos, and Delayed Charges.

Populate all of the customer information at the top. Select the Product/Service at the bottom. Click the Rate drop-down box and you’ll find the price rule you just created available as an option. Select the rule and you should see the Subtotal on the Sales Receipt change accordingly.

Download the free template by filling out the form below

Estimate the amounts and timing of cash inflows

Forecast the amounts and timing of cash outflows for expenses and capital projects

Determine a desired ending cash balance for every month in the planning period

Factor in the effects of short-term and long-term financing

Analyze the most likely, best-case, and worst-case scenarios in your financial statements

Get your copy of the church financial budget template

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

Sample church financial budget to help your congregation reach its goals

All right, we finally made it! This is the third post on church budgeting. It’s also the sixth, and final, post on church strategic planning. Yes…this is long overdue.

Capital budgeting for churches was addressed previously. As was creating an operating budget. The capital budget involved the forecasting of cash inflows and outflows from the installation of a new parking lot. The operating budget involved estimating revenue and expenses to arrive at a pro forma (estimated) income statement.

The financial budget builds off of the operating budget. It allows your church to estimate the timing of cash inflows and cash outflows. Doing so will help ensure that your church doesn’t run up against a cash flow crunch throughout the coming year.

Yes, strategic planning is time-consuming and labor-intensive. Never more so than the first time you do it. For the church that is serious about ensuring the ongoing fulfillment of its mission, it is time well spent.

What is a church‘s financial budget?

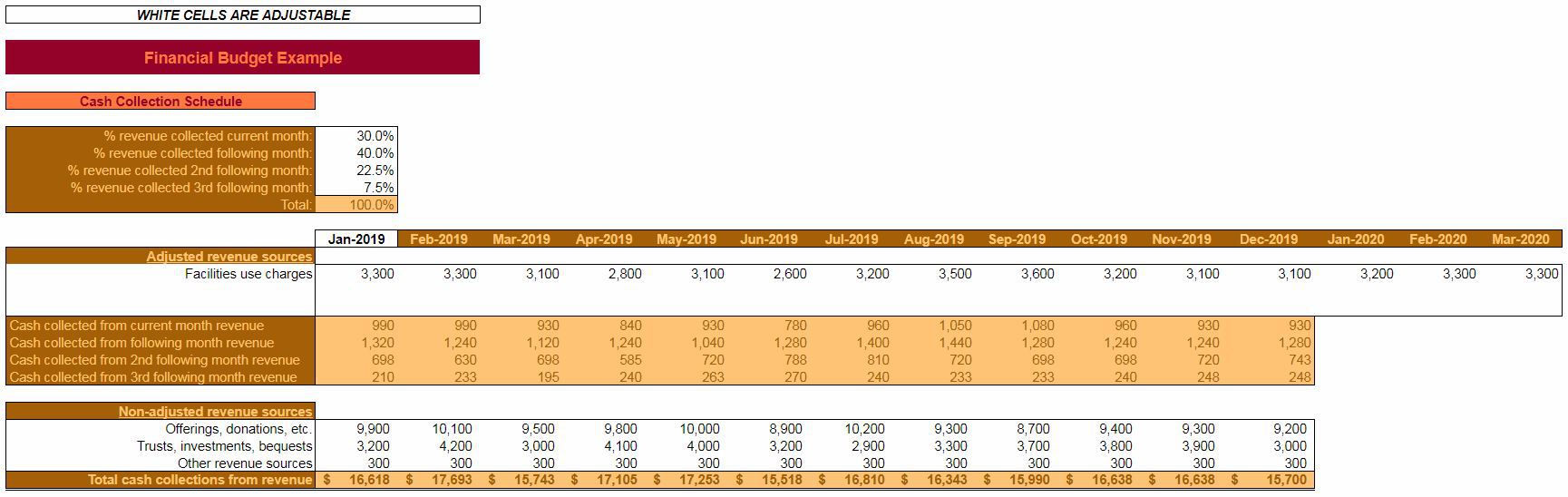

A church financial budget walks through the expected timing and amounts of cash receipts and expenditures over the course of the next year. Churches are in a unique (and somewhat enviable) position since most of their revenue comes from donations. They typically receive cash instantly.

One exception, for the church, might be Facilities use charges, or something similar. Revenue like this is often paid in advance to reserve dates and times. Since the cash comes in earlier (typically) than when the service is delivered, there could be a situation where cash flow and revenue recognition are different.

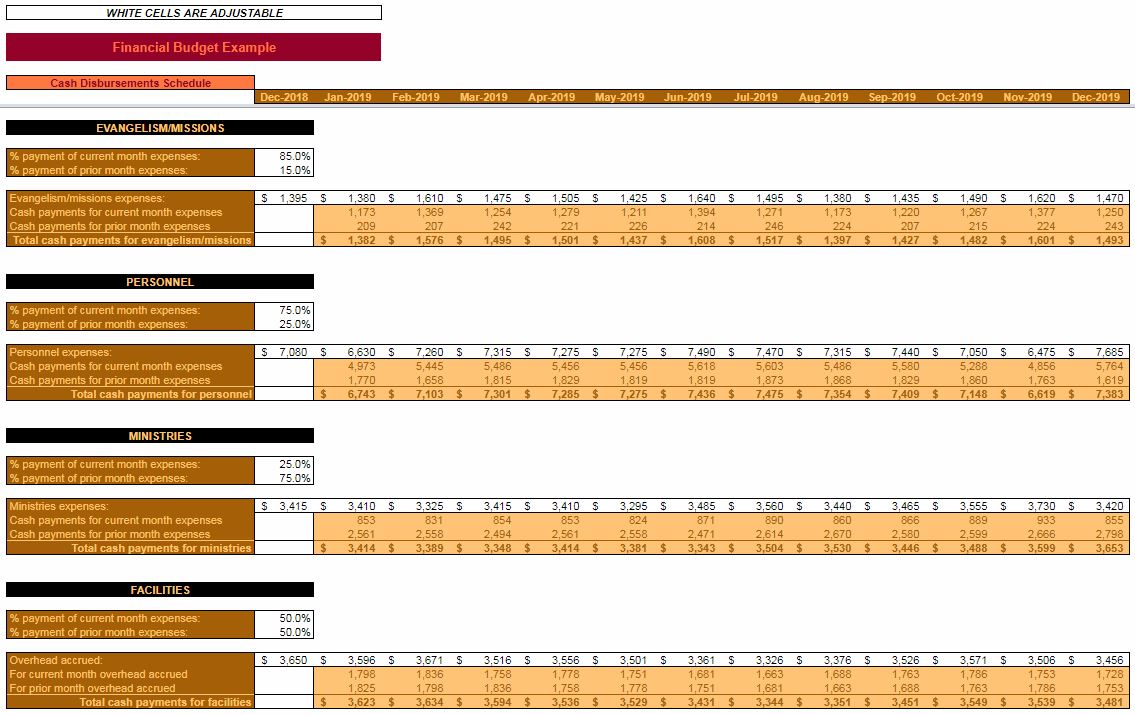

On the cash disbursement side, a church faces a lot of the same issues as a for-profit business. The recognition of expenses could be different from when the actual cash leaves the church’s checking account.

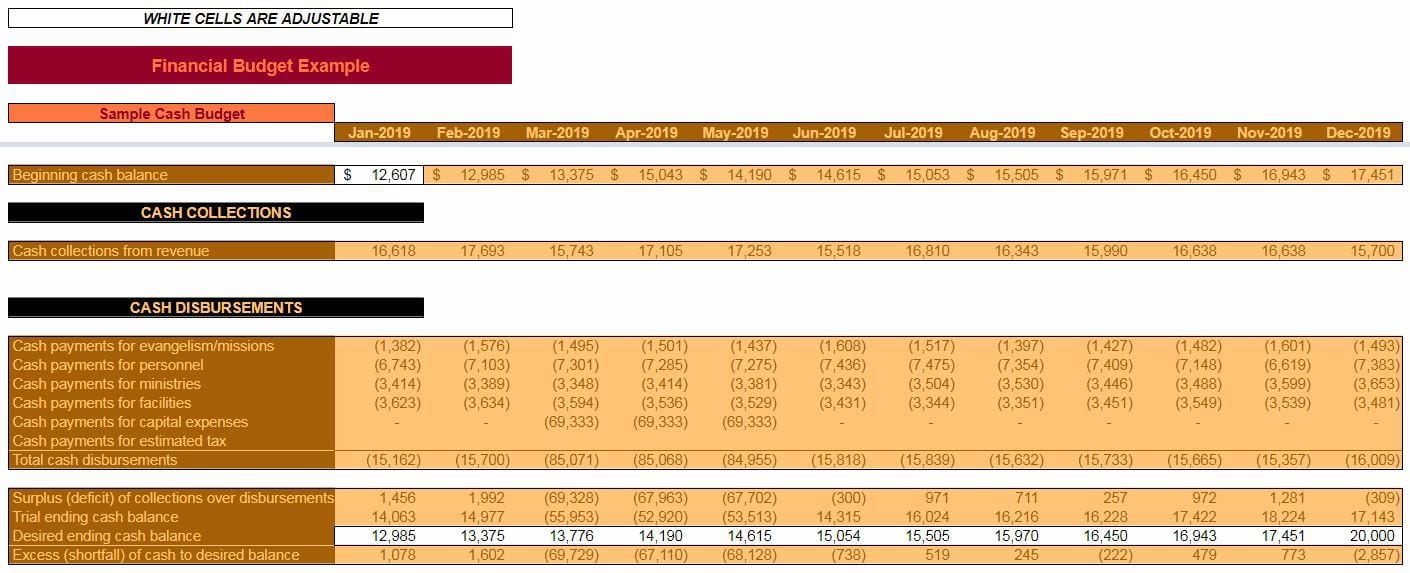

The church’s Cash Collection Schedule and Cash Disbursement Schedule will come together into a Cash Budget. It is here that the church will have the opportunity to adjust the Desired Ending Balance. And to make any tweaks to Short-term or Long-term Financing arrangements.

Everything culminates with Pro Forma (expected) financial statements. Just as with the operating budget. This allows the church to compare where they start the year with where they end it. With this information, Ratios can be calculated. More importantly, needed action can be taken to hedge potential problems.

Also, a chart illustrating the month-to-month changes will be available. Also, your church will have the opportunity to play with best-case and worst-case scenarios.

The importance of a church financial budget

Cash is the lifeblood of a business, and a nonprofit organization is no exception. All strategic planning plays an important role in preparing for the future. However, none of the steps may be more important than the financial budget.

Failure to plan for potential shortfalls in cash could mean shuttering the doors. I could mean forever forgoing the opportunity to lead your congregation to the achievement of its mission.

How does a church’s financial budget differ from an operating budget?

A financial budget forecasts cash flow in and cash flow out. An operating budget, if you’ll remember, forecasts revenue and expenses. The difference might seem negligible, but there are some important distinctions.

Operating at a loss in a particular month (e.g. having more expenses than revenue) won’t necessarily constitute a crisis in your church. It can’t go on forever, but if it’s a short-term problem, you should be able to push through it.

But, having more cash go out than comes in during a given month will obviously deplete your cash on hand. Beyond that, if the difference is big enough, and goes on for long enough, your church will be in real trouble.

Cash is king

You don’t pay your bills, or your employees, with numbers on a spreadsheet. As great as spreadsheets are, they can’t do that for you. You pay expenses with cash. So, even if things look good on a spreadsheet or a financial statement, if the cash isn’t there, problems could start compounding.

Over the long-term, the amount of revenue should equal the amount of cash flow in, more or less. Likewise, the amount of expenses should equal the amount of cash flow out. It’s all a question of timing.

An operating budget is important to make sure that your church stays financially healthy for the upcoming year. A financial budget is important to make sure that your church stays solvent from month to month.

One more important distinction is that a financial budget (specifically the cash budget) takes into account things that the operating budget does not. For example, capital projects, financing, and investments. I’ll illustrate the effects of these sorts of things later in the post.

How does a church financial budget differ from that of a for-profit company?

A financial budget for a church versus a financial budget for a for-profit company will differ in a couple of ways.

On the cash collection side, a lot of a church’s revenue is recognized at the same time the cash is collected. The same is not true for your typical for-profit company. The exception, for a church, might be a facilities use charges, or something similar. The timing of cash receipt and revenue recognition being so close together make the cash collection side of a church’s financial budget a little bit simpler.

The cash disbursement side of things will be similar to a for-profit company. Bills are bills after all. When expenses hit versus when they’re paid could be very different. Additionally, capital expenses, if applicable, will require big chunks of cash to be spent at one time. Just as is the case with for-profit companies. Conversely, though, income taxes are a non-factor for churches.

Other factors will be similar between a for-profit company and a church when it comes to financial budgeting. The church may still require short-term and long-term financing. Also, it may put its money into separate savings or investment account, just as a for-profit company would.

So, it stands to reason, that there are a couple of minor differences between the two. But, all in all, financial budgeting is just as important for churches, and other nonprofit organizations, as it is for their for-profit counterparts.

Why should you have a church financial budget?

The reasons for your church to have a financial budget for the coming year are the same as the reasons for doing any other step in the strategic planning process. These sorts of things are done to force you to think about what the future might hold. That way you can best position your church for success.

If your church runs out of cash midway through the year then its very existence might be at stake. Even if your church just gets into a cash flow crunch, that could start a chain of events that might keep it from realizing its full potential.

Certainly, drafting a financial budget and going through all of the steps of the strategic planning process isn’t going to guarantee that your church won’t fall upon hard times. However, it will probably lessen the length and severity of the hard times. Plus, when the hard times do come, then you’ll at least know you’ve done everything in your power to protect your church and to ensure its ongoing success.

One more benefit is the ability to plan long-term and short-term financing. Since these two factors play a large part in the amount of cash flowing in and out of your church, they should be scrutinized. The financial budget allows you to prepare and make arrangements for financing needs well in advance of the time that they become critical.

How to create a church financial budget

Creating a financial budget starts with a forecast of the timing and amounts of cash inflows from revenue sources. As mentioned earlier, since many of a church’s typical revenue sources are of the sort that collects cash immediately – this could be a pretty easy step in the process.