Financial leverage is simply the act of borrowing money to invest. This is done with the hope of earning a return on that money. A return that is greater than the cost. Often, the potential for gain is disproportionately bigger than the cost. But, the cost is fixed and will be the same regardless of the return earned. Small businesses must learn how to effectively manage their degree of financial leverage. Otherwise, they could find themselves buried under the weight of repayment.

Let’s talk about some of the advantages and disadvantages of financial leverage. Also, how the degree of financial leverage ratio can provide insight into net income.

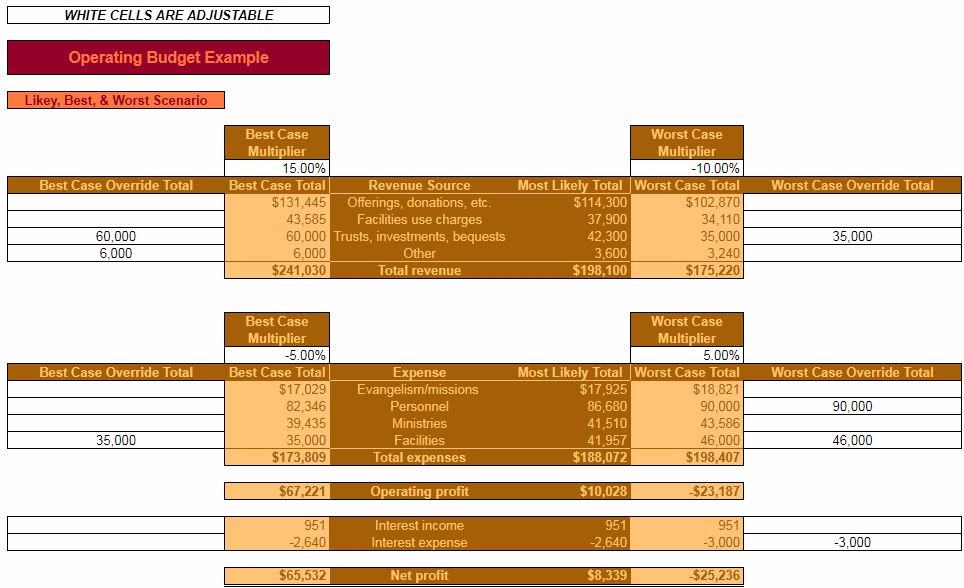

Download your copy of the workbook used in this post

Complete the form below. Upon email confirmation, the workbook will open in a new tab.

Financial leverage advantages

Financial leverage is a strategy that can be employed to boost gains. The cost of borrowed money (typically) doesn’t change. So, if that money can be used in a way that earns returns beyond the cost of borrowing – a small business can end up way better off than it would have otherwise.

I always say that every investment comes down to three things – cash in, cash out, and time. If the cost of leverage (cash out) is low enough and the terms are favorable (time), then the cash in has the best opportunity to be big enough to make financial leverage worthwhile.

High financial leverage helps small businesses avoid dilution of earnings from the issuance of equity. It also gives them the ability to put more money to work than they would have otherwise. Both of these advantages can translate into excess returns.

Additionally, interest is tax-deductible. This lessens the tax burden that a company would realize if the same funds were raised through equity. Keep in mind that interest is a fixed cost. A fixed cost that can negatively affect a small business if operating profits aren’t high enough.

Financial leverage is a better fit for some businesses than others

On my sister site, I’ve written often about the benefits of certain business models. For businesses with the right business model, more financial leverage could be very beneficial. This is if it brings in more long-term customers. These business models are conducive to earning a good ROI on borrowed money.

Handling debt responsibly = the ability to borrow more in the future

If a small business effectively employs financial leverage, their creditworthiness improves. With improved creditworthiness, they will (likely) be able to borrow more in the future. If they continue to execute effectively, they can earn compounded returns.

The cost of borrowing (rate) could drop with a successful history of repayment. This could decrease the cost of future financial leverage. Lower cost should mean lower risk. Lower risk increases the likelihood of employing it in a successful manner.

Financial leverage disadvantages

Just as it has the potential to boost gains, financial leverage can also boost losses. Every dollar borrowed represents a little more risk. Again, that’s why the return from the borrowed monies means so much.

But, the lender doesn’t care if your small business makes 10x the cost of borrowing. Or, if it “only” makes 100% of the cost of borrowing. It expects its money back, plus interest, either way.

Borrowing money will increase your cash flow out. If the cash flow in isn’t enough to offset that, then, sooner or later, insolvency will ensue.

It all depends on the context

A lot of the negative stigma surrounding borrowing stems from the personal sector. In the personal sector, when people borrow, they often do so to buy consumer goods. Things that don’t earn any sort of return. These items actually depreciate in value. For example, cars and technology.

Nobody flinches when somebody borrows an ungodly sum of money to buy a house. This is because a house (for better or worse) is expected to increase in value.

Just as certain business models are conducive to financial leverage, others are not. Consider business models that sell time for money or one-time purchase items. These businesses will have to be confident in their financial modeling to ensure that they can earn an adequate ROI on financial leverage.

Finally, the perception of leverage depends on timing. During boom times, the companies borrowing look like geniuses. Conversely, if the economy turns against a business that has irresponsibly borrowed, then they could look foolish.

Financial leverage + operating leverage?

There are two general types of leverage that a small business can use. Operational leverage (which I plan to write about next) and financial leverage. The degree of operating leverage measures the effect of fixed costs (not interest) on operating income.

Beware compounding leverage by adding operating (fixed costs) to financial, or vice versa. This could sneak up on a small business. It could create a situation where management is caught unprepared. The result is potentially catastrophic. It’s important that scenarios like this be modeled out and planned for.

Most people understand the risks associated with borrowing money (financial leverage). The risks of operating leverage are a little more camouflaged.

Make sure you plan around your company’s (potential) total leverage situation. Annual strategic planning with an operating budget allows you to do just that.

Regulatory authorities might paint an overly rosy picture

When interest rates are kept low, the hurdle rate (minimum ROI to justify investment) is also lower. This incentivizes small businesses to take on projects that they might not otherwise. Less is demanded of investments. The pursuit of extraordinary returns might stop short in favor of quick-and-easy (but “good enough”) returns.

Also, by making interest tax-deductible, the effective cost of leverage is lowered even further. This further incentivizes small businesses to use financial leverage. Doing so could amplify any of the previously mentioned disadvantages.

Financial leverage example

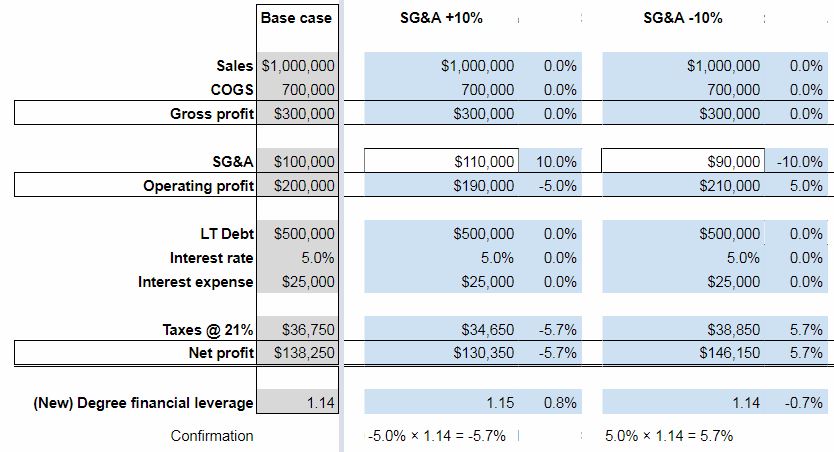

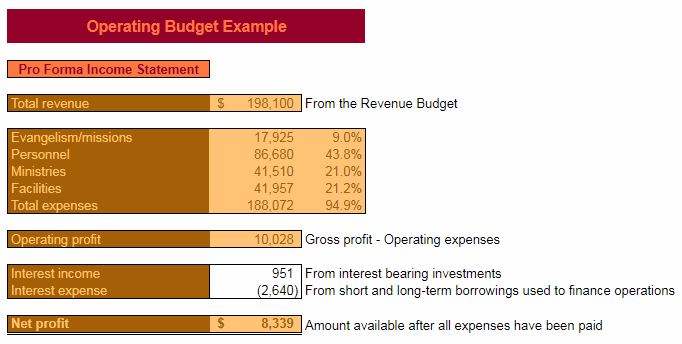

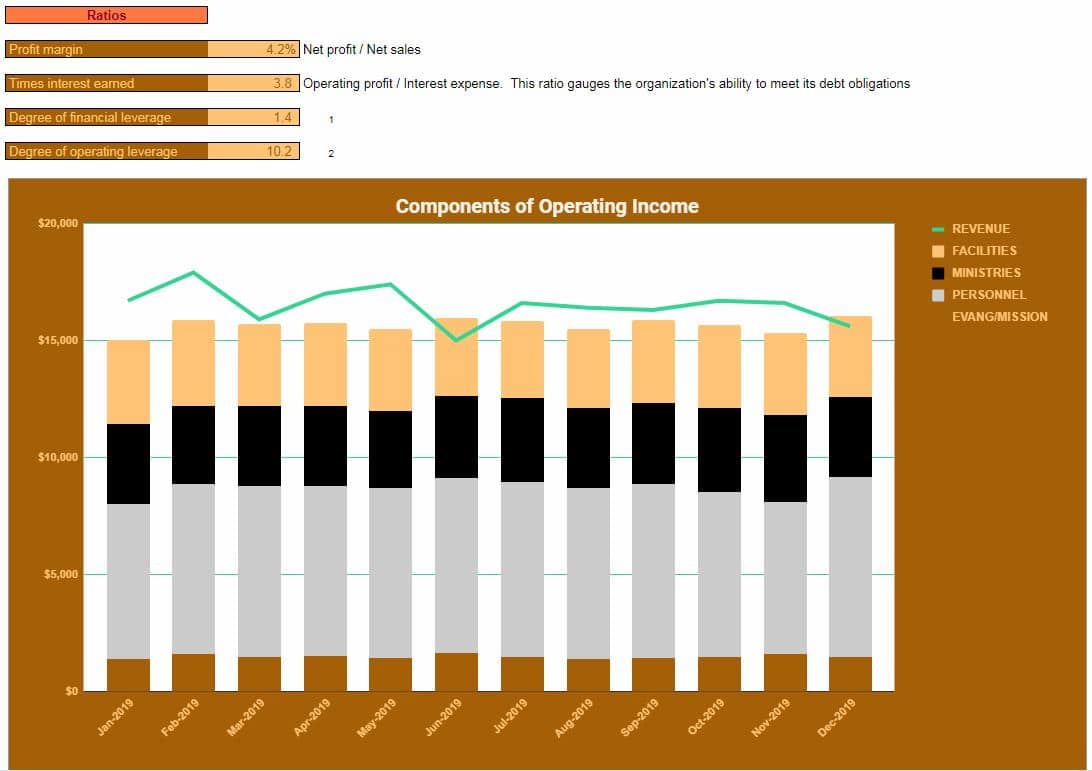

The Degree of Financial Leverage shows the amplification that borrowing money can provide to profits and losses. So, for instance, in the example operating budget, the Degree of Financial Leverage is 1.4. This means, at this level of borrowing, that for every 10% change in Operating Profit, Net profit would increase by 14% (10% × 1.4).

That sounds great, but the opposite is also true. If Operating Profit declined by 10%, then this level of borrowing would cause Net profit to decrease by 14%. That’s the nature of leverage. It amplifies gains and losses.

I created a spreadsheet to model the changes in profit due to changes in other line items. It helps to better understand how the income statement is affected by financial leverage,

I started with a Base case income statement for a small business that has $1 million in sales. This example business also has a 20% operating margin with $500K in debt at a 5% Interest rate. Its Net profit is approximately $138K.

This company’s Degree of financial leverage is 1.14 ($200,000 ÷ [$200,000 – $25,000]).

Only one variable was changed at a time. Here’s what I found:

The effects of an increase or decrease in sales

A 10% increase in Sales translates into a 50% increase in Operating profit – all other things being equal. As expected, this 50% increase in Operating profit translates into a 57.1% increase in Net profit. This is because the Degree of financial leverage is 1.14 (50.0% × 1.14 = 57.1%).

The same thing happens, in the opposite direction. When Sales drop by 10%, Operating profit decreases by 50%. Net profit drops by 57.1%.

The effects of an increase or decrease in COGS and SG&A expenses

Since COGS is less than Sales, a 10% change doesn’t have as big of an effect on Operating profit. The result is a drop in Operating profit of 35%. As expected, the resulting change in Net profit is -40% (-35.0% × 1.14 = -40.0%).

SG&A expenses, being even lower, have less of an impact on Operating profit. A 10% increase only lowers Operating profit by 5% and Net profit by 5.7% (-5.0% × 1.14 = -5.7%).

Of course, things work the same in the opposite direction. A -10% change in COGS increases Operating profit by 35% and Net profit by 40%. A -10% change in SG&A expenses increases Operating profit by 5% and Net profit by 5.7%.

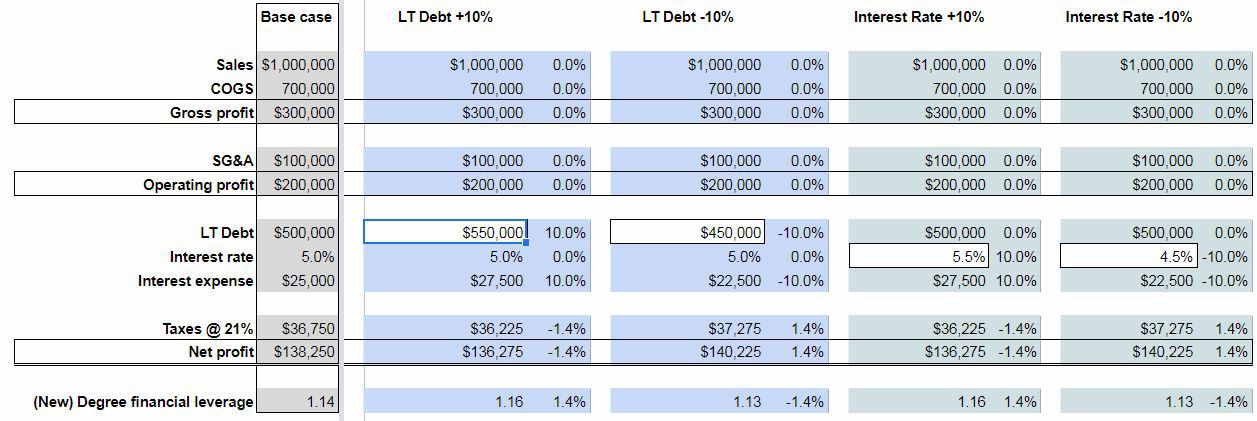

The effects of an increase or decrease in Long-term Debt & Interest rates

As shown above, changes in the income statement that result in increases to Operating profit are amplified in Net profit by the Degree of financial leverage.

But, what about changes below Operating profit? As expected, a 10% change in either the amount of LT Debt or the Interest rate, results in a corresponding 10% change in Interest expense.

This hypothetical small business carries a sizable amount of LT Debt. Still, Interest expense is still a relatively immaterial expense. Thus, the effect of a change in LT Debt and Interest rates is only ±1.4% on Net profit.

Click to enlarge

Going forward with a new Degree of financial leverage

Because of the nature of the Degree of financial leverage calculation (Operating profit ÷ [Operating profit – Interest expense]), when Operating profit increases, the Degree of financial leverage decreases – all other things being equal. The opposite is, of course, true too.

What does this mean?

It means that if your small business increases Operating profit this year, then your Degree of financial leverage is going to go down for next year. Which isn’t catastrophic. But, it means that a similar gain in Operating profit next year won’t translate into the same boost in Net profit.

To get that, your small business would have to borrow more funds.

On the same token, if your company has a decrease in Operating profit this year, then your Degree of financial leverage will increase for next year. This increase will amplify the effects of a gain in Operating profit next year. But, it doesn’t necessarily mean that you’ll end up ahead of where you would have been if you would have increased Operating profit in year 1.

Shortcomings of the Degree of financial leverage ratio

Again, the Degree of financial leverage ratio is calculated as follows:

Big companies typically borrow money through the issuance of bonds. This means that they only pay interest until the bond matures.

Small businesses, like yours, don’t issue bonds. The nature of borrowing can vary, but often, loans are repaid on an installment basis. E.g. payments consist of both principal and interest.

So, a ratio that only measures the effects of Interest expense doesn’t completely capture the impact of financial leverage. For small businesses anyways.

Two extreme examples

First, consider a small business that borrowed 10x their previous year’s revenue. If they did so at a very low interest rate, their Degree of financial leverage would also be relatively low. But, having borrowed a disproportionate amount of money, they would theoretically have the opportunity to boost Sales/Operating profit greatly.

Also, consider the other extreme. What if a company borrowed a very modest amount of money? But, was forced to pay an exorbitant interest rate? In this instance, the Degree of financial leverage would be relatively high. But, the company’s opportunity to use this leverage in a beneficial manner is limited.

Finally, in order for the Degree of financial leverage to accurately predict the change in Net profit, Taxes must remain at a constant percentage. E.g. they can’t be 21% of Operating profit – Interest expense (EBT) one year and 22% the next. The Forecasted Change in Net profit won’t equal what’s calculated in the Confirmation.

The amount of LT Debt and the Interest rate/expense must also remain constant for the “Operating profit × Degree of financial leverage = Change in Net profit” equation to work out.

So, obviously, the Degree of financial leverage has limitations. It is designed for big businesses – not necessarily small ones. It is based on amounts in the income statement, and not the cash flow statement. Thus, no consideration is taken for the effects of principal repayment.

If its limitations are kept in mind, and if reasonable changes are forecasted, then it can provide guidance on the potential benefits or detriments of financial leverage.

How financial leverage affects business decisions

Plug your small business’ information into the Your degree of financial leverage worksheet. It will help you better understand how your borrowing might help or hinder you in the coming year.

Financial leverage, in and of itself, is neither good nor bad. It’s all about how it’s employed. If it’s used to buy (rather than sell) consumable assets that provide little or no return – it’s wasted. If it’s allocated to resources that increase productivity (or earn extraordinary returns) – it’s a valuable tool for small businesses.

What are your thoughts on the use of financial leverage?

What are some of the advantages and disadvantages I neglected to include?

How about some ways that you’ve effectively employed financial leverage in your small business?

Download the free template by filling out the form below

Estimate the amounts and timing of cash inflows

Forecast the amounts and timing of cash outflows for expenses and capital projects

Determine a desired ending cash balance for every month in the planning period

Factor in the effects of short-term and long-term financing

Analyze the most likely, best-case, and worst-case scenarios in your financial statements

Get your copy of the church financial budget template

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

Sample church financial budget to help your congregation reach its goals

All right, we finally made it! This is the third post on church budgeting. It’s also the sixth, and final, post on church strategic planning. Yes…this is long overdue.

Capital budgeting for churches was addressed previously. As was creating an operating budget. The capital budget involved the forecasting of cash inflows and outflows from the installation of a new parking lot. The operating budget involved estimating revenue and expenses to arrive at a pro forma (estimated) income statement.

The financial budget builds off of the operating budget. It allows your church to estimate the timing of cash inflows and cash outflows. Doing so will help ensure that your church doesn’t run up against a cash flow crunch throughout the coming year.

Yes, strategic planning is time-consuming and labor-intensive. Never more so than the first time you do it. For the church that is serious about ensuring the ongoing fulfillment of its mission, it is time well spent.

What is a church‘s financial budget?

A church financial budget walks through the expected timing and amounts of cash receipts and expenditures over the course of the next year. Churches are in a unique (and somewhat enviable) position since most of their revenue comes from donations. They typically receive cash instantly.

One exception, for the church, might be Facilities use charges, or something similar. Revenue like this is often paid in advance to reserve dates and times. Since the cash comes in earlier (typically) than when the service is delivered, there could be a situation where cash flow and revenue recognition are different.

On the cash disbursement side, a church faces a lot of the same issues as a for-profit business. The recognition of expenses could be different from when the actual cash leaves the church’s checking account.

The church’s Cash Collection Schedule and Cash Disbursement Schedule will come together into a Cash Budget. It is here that the church will have the opportunity to adjust the Desired Ending Balance. And to make any tweaks to Short-term or Long-term Financing arrangements.

Everything culminates with Pro Forma (expected) financial statements. Just as with the operating budget. This allows the church to compare where they start the year with where they end it. With this information, Ratios can be calculated. More importantly, needed action can be taken to hedge potential problems.

Also, a chart illustrating the month-to-month changes will be available. Also, your church will have the opportunity to play with best-case and worst-case scenarios.

The importance of a church financial budget

Cash is the lifeblood of a business, and a nonprofit organization is no exception. All strategic planning plays an important role in preparing for the future. However, none of the steps may be more important than the financial budget.

Failure to plan for potential shortfalls in cash could mean shuttering the doors. I could mean forever forgoing the opportunity to lead your congregation to the achievement of its mission.

How does a church’s financial budget differ from an operating budget?

A financial budget forecasts cash flow in and cash flow out. An operating budget, if you’ll remember, forecasts revenue and expenses. The difference might seem negligible, but there are some important distinctions.

Operating at a loss in a particular month (e.g. having more expenses than revenue) won’t necessarily constitute a crisis in your church. It can’t go on forever, but if it’s a short-term problem, you should be able to push through it.

But, having more cash go out than comes in during a given month will obviously deplete your cash on hand. Beyond that, if the difference is big enough, and goes on for long enough, your church will be in real trouble.

Cash is king

You don’t pay your bills, or your employees, with numbers on a spreadsheet. As great as spreadsheets are, they can’t do that for you. You pay expenses with cash. So, even if things look good on a spreadsheet or a financial statement, if the cash isn’t there, problems could start compounding.

Over the long-term, the amount of revenue should equal the amount of cash flow in, more or less. Likewise, the amount of expenses should equal the amount of cash flow out. It’s all a question of timing.

An operating budget is important to make sure that your church stays financially healthy for the upcoming year. A financial budget is important to make sure that your church stays solvent from month to month.

One more important distinction is that a financial budget (specifically the cash budget) takes into account things that the operating budget does not. For example, capital projects, financing, and investments. I’ll illustrate the effects of these sorts of things later in the post.

How does a church financial budget differ from that of a for-profit company?

A financial budget for a church versus a financial budget for a for-profit company will differ in a couple of ways.

On the cash collection side, a lot of a church’s revenue is recognized at the same time the cash is collected. The same is not true for your typical for-profit company. The exception, for a church, might be a facilities use charges, or something similar. The timing of cash receipt and revenue recognition being so close together make the cash collection side of a church’s financial budget a little bit simpler.

The cash disbursement side of things will be similar to a for-profit company. Bills are bills after all. When expenses hit versus when they’re paid could be very different. Additionally, capital expenses, if applicable, will require big chunks of cash to be spent at one time. Just as is the case with for-profit companies. Conversely, though, income taxes are a non-factor for churches.

Other factors will be similar between a for-profit company and a church when it comes to financial budgeting. The church may still require short-term and long-term financing. Also, it may put its money into separate savings or investment account, just as a for-profit company would.

So, it stands to reason, that there are a couple of minor differences between the two. But, all in all, financial budgeting is just as important for churches, and other nonprofit organizations, as it is for their for-profit counterparts.

Why should you have a church financial budget?

The reasons for your church to have a financial budget for the coming year are the same as the reasons for doing any other step in the strategic planning process. These sorts of things are done to force you to think about what the future might hold. That way you can best position your church for success.

If your church runs out of cash midway through the year then its very existence might be at stake. Even if your church just gets into a cash flow crunch, that could start a chain of events that might keep it from realizing its full potential.

Certainly, drafting a financial budget and going through all of the steps of the strategic planning process isn’t going to guarantee that your church won’t fall upon hard times. However, it will probably lessen the length and severity of the hard times. Plus, when the hard times do come, then you’ll at least know you’ve done everything in your power to protect your church and to ensure its ongoing success.

One more benefit is the ability to plan long-term and short-term financing. Since these two factors play a large part in the amount of cash flowing in and out of your church, they should be scrutinized. The financial budget allows you to prepare and make arrangements for financing needs well in advance of the time that they become critical.

How to create a church financial budget

Creating a financial budget starts with a forecast of the timing and amounts of cash inflows from revenue sources. As mentioned earlier, since many of a church’s typical revenue sources are of the sort that collects cash immediately – this could be a pretty easy step in the process.

On the cash outflow side, each expense category from the church operating budget will be looked at separately. Each will be unique in terms of when the cash is expected to leave the church. Additionally, this is where capital expenditures will be entered. If you’ve done a capital budget for your church, then you should know the total amount expected to be spent. It’s just a matter of entering the timing.

The cash budget will bring together the Cash Collections Schedule and the Cash Disbursements Schedule. Also, here, you’ll be able to determine a Desired ending cash balance for every month. Beyond that, information about long and, short-term financing will need to be entered.

Everything entered previously culminates in a Pro Forma Balance Sheet and Cash Flow Statement. Along with the Pro Forma Income Statement from the operating budget, you’ll have a complete set of forecasted financial statements for the coming year. Anytime there are financial statements, you can expect there will be Ratios. The Executive Summary ends, as usual, with a chart illustrating the most relevant information from the workbook.

An opportunity is given to play with the best and worst-case scenarios. Just as was done with the operating budget. Here, you’ll have the opportunity to tweak the amounts on your Pro Forma Balance Sheet, Cash Flow Statement, and Income Statement to the positive and negative side. Accordingly, best case and worst case Ratios will also be calculated.

Timing of cash inflows

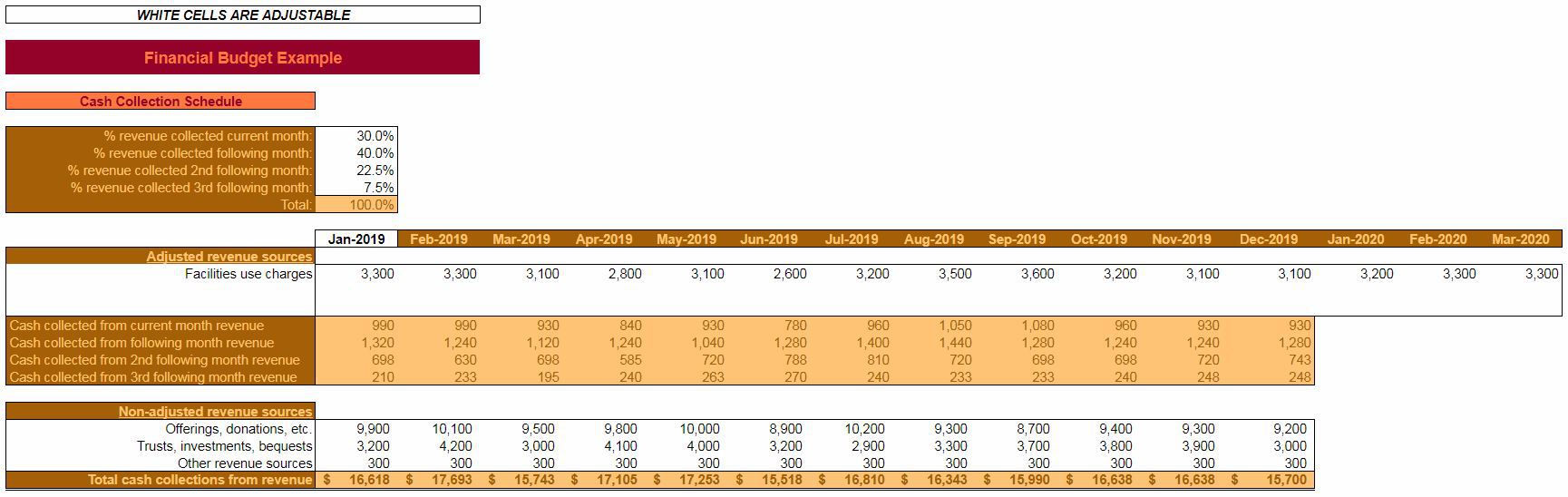

The Cash Collections Schedule is where you’ll enter the pertinent information regarding timing and amounts of cash inflows.

There are three general sections of information to be entered. The first is related to the timing of the receipt of Adjusted revenue sources. Here, you’ll dictate how much, percentage-wise, you expect to receive in the current month, following month, 2nd following month, and 3rd following month from your Adjusted revenue sources.

Click to enlarge

Cash collections examples

If you expect, on average, to receive half of your revenue in cash, from your Adjusted revenue sources during the same month as the “sale,” then you would enter 50% in the % revenue collected current month field. If you expect, on average to receive the other half in the next month after the “sale” then you would enter 50% in the % revenue collected following month field. The other two (2nd following month and 3rd following month) would be 0%. What matters is the Total equals 100%.

Another example – let’s say you only took a 10% deposit for Facility use charges and collected the remainder of the balance three months later. Then, you would enter 10% in the % revenue collected current month field and 90% in the % revenue collected 3rd following month.

Hopefully, this clarifies the purpose of these variables a little bit.

The remainder of the Cash Collections Schedule is where you’ll enter yourAdjusted and Non-adjusted revenue sources. Enter each separately along with the amounts corresponding to the month that the revenue is earned.

Adjusted revenue sources

Adjusted Revenue Sources are those where the cash is collected at a different time than when the revenue is recognized.

For churches, the most practical example I could think of was Facilities Use Charges. Where the church collects cash in advance for rental of its facilities.

Revenue sources such as these, are unique, however. Most organizations recognize revenue first and then the cash is collected afterward. Facilities Use Charges are unique though. The revenue isn’t technically earned until the event for which the facilities were rented takes place. But, cash is collected in advance via deposits or payment plans.

So, the revenue for Facilities Use Charges are forecasted out three months into the following year (2020). This is done because some cash might be collected in Dec-2019 for revenue that will be recognized in Mar-2020.

Below the white cells where you’ll enter the revenue sources and forecasted amounts, you’ll see that the calculations are made based on the % revenue collected from above. The percentages entered there specify how much cash will be collected in a given month from current month revenue, following month revenue, 2nd following month revenue, and 3rd following month revenue. These amounts will change depending on what’s entered in the forecasted fields for Adjusted Revenue Sources.

Non-adjusted revenue sources

Non-adjusted revenue sources are much simpler. All you do is enter your different sources on the left and the forecasted amount for each month in the coming year. Cash is collected at the time of revenue recognition. So, there’s no need to forecast out any further.

At the bottom, the Total cash collections from revenue equal cash collection from Adjusted revenue sources plus the Non-adjusted revenue sources for a given month.

Timing of cash outflow

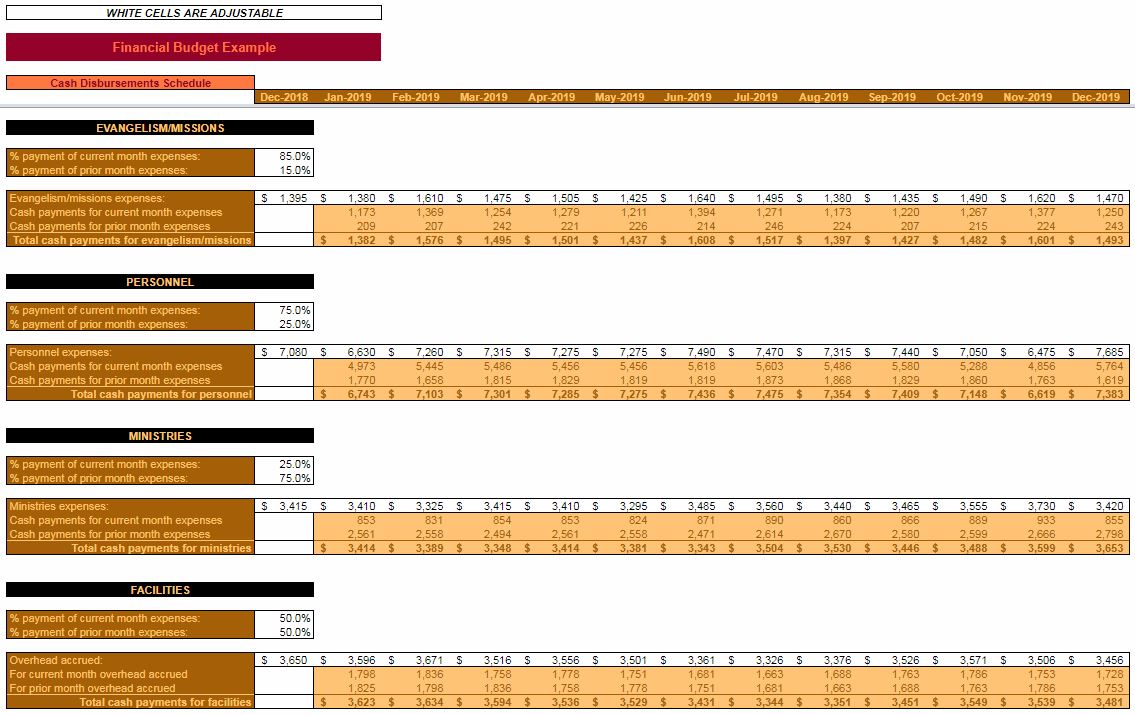

The Cash Disbursements Schedule is where you’ll enter information about the timing and amounts of cash outflows.

As with any organization, cash tends to leave through more avenues than it arrives. Each category of expenses (from the operating budget) is examined individually. Information from the capital budget will also be entered as it pertains to cash leaving the church.

Click to enlarge

The four categories of expenses from the operating budget are looked at independently. Granted, individual expenses within a particular category probably have different timings in terms of cash flow. But, entering each expense separately would needlessly complicate an already intensive endeavor. So, percentages are entered for each category for the % payment of current month expenses and % payment of prior month expenses.

The % payment of current month expenses refers to the percentage of that month’s forecasted expenses which will be paid with cash, in the same month. The % payment of prior month expenses refers to the percentage of the previous month’s forecasted expenses which will be paid with cash this month.

As you might expect, those percentages must add up to 100%. There’s no allocation made for expenses that will be unpaid. Since your church is reputable, and you’ve committed yourself to strategic planning (including all forms of budgeting), you’ll be well prepared for the coming year. Therefore, your church shouldn’t find itself in a situation where it can’t pay its bills.

Each category of expenses is different

The categories are pretty general. Hopefully, they are indicative of the types of expenses that your church faces. Of course, if you were making a financial budget from scratch, you might do things somewhat differently.

Once you’ve settled on the timing of cash flows, it’s time to enter the forecasted expenses for the last month of the current year through the last month of the planning (next) year. The reason that expenses are entered for the last month of the current year is because of the % payment of prior month expenses field. We must know how much cash is going to leave the church in January, because of December expenses.

The relevant cash flow amount is automatically calculated for each month and totaled by category.

Flashback to the capital budget

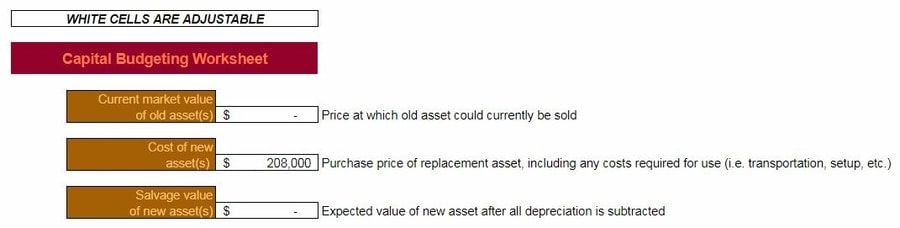

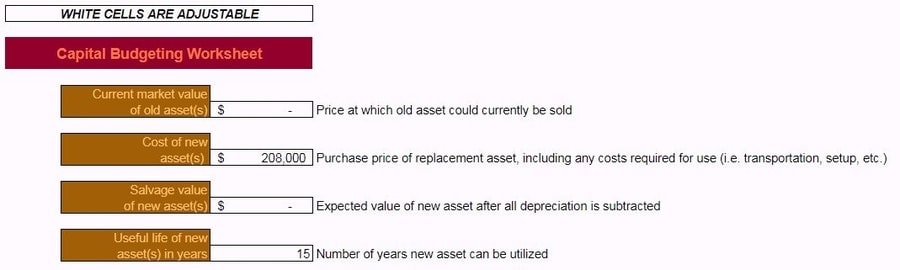

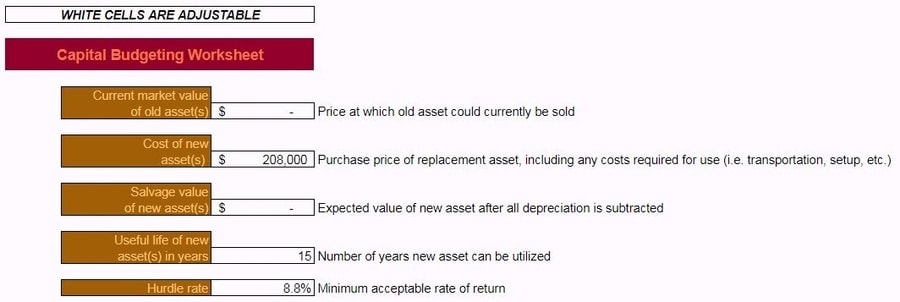

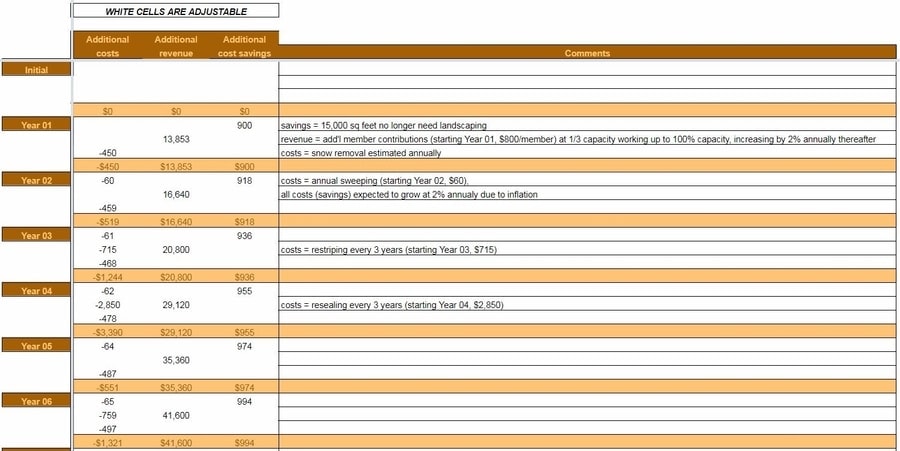

Think back to the capital budgeting for churches post that I wrote a couple of months ago. You might remember that the plan was for our hypothetical church to add 53 parking spots in the coming year. They planned to do this because the congregation was growing and they need additional capacity for parking.

You might also remember at the expected initial cost for this new parking lot was $208,000.

Click to enlarge

As you can see, in accordance with the capital budget, our example church expects to make three payments of $69,333. We’re assuming that, for this construction project, payment will be made in three equal portions over the three months it takes to start and finish the parking lot.

Our hypothetical church isn’t so big that it can disregard the spending of over $200,000. So, obviously, we needed to work that into the financial budget. The capital expenses section of the Cash Disbursements Schedule is where that’s done. This information will now carry over to the Cash Budget. This is where planning can be done for financing, if necessary.

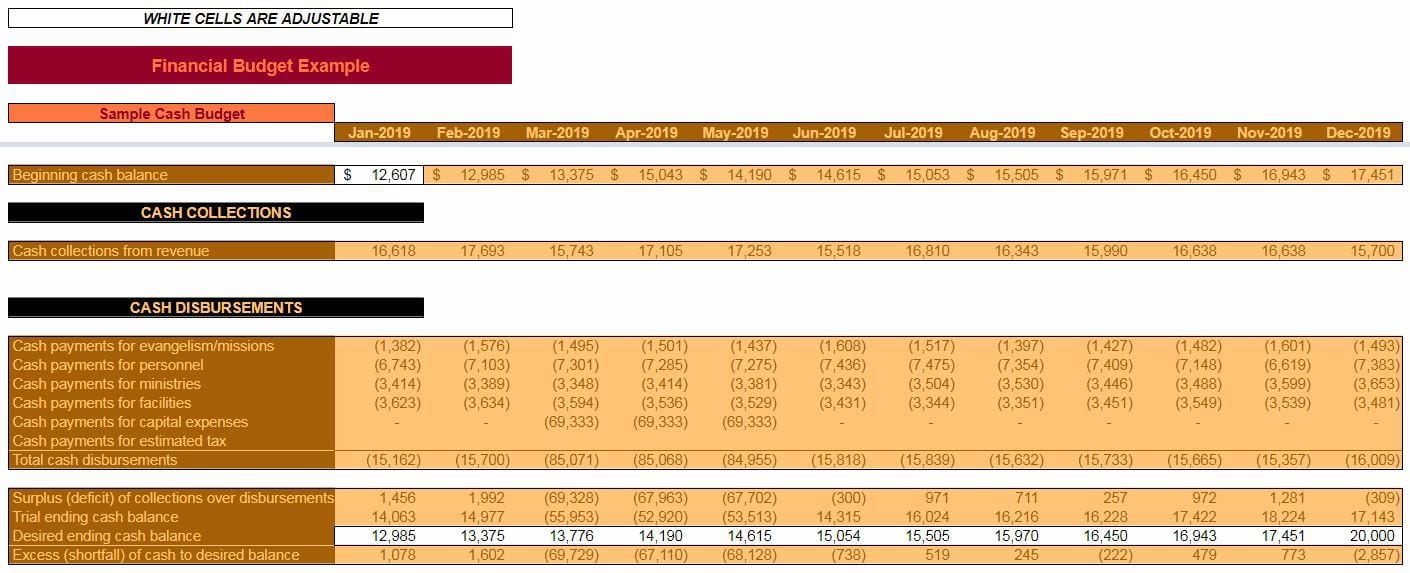

Creating a cash budget

The Cash Budget brings together information entered in the Cash Collections Schedule and the Cash Disbursements Schedule. In addition, financing, both short and long-term are addressed; as are investments.

This is where you will forecast your actual cash balances throughout every month in the planning year. Only a few fields need to be entered. Most of what is analyzed in the Cash Budget is based on the previously entered information.

Click to enlarge

Logically, the first bit of information to be addressed in the Cash Budget is your Beginning cash balance. This will need to be entered for the first month of the planning period. You will probably have to forecast this amount if you are (as you should be) planning several months in advance. Don’t worry, as the time gets closer, this amount can be changed and, just as with any of these planning tools, tweaks can be made

From that point on, the Beginning cash balance is automatically calculated. Because, of course, the Beginning cash balance for any given month is going to be the same as the Ending cash balance for the previous month.

Cash collections and disbursements

The cash collections and cash disbursements sections will each pull from their respective Schedules – with a few exceptions.

Surplus(deficit) of collections over disbursements = Cash collections from revenue – Total cash disbursements

This amount represents the difference between cash collections and cash disbursements in a given month. A positive amount means that more cash was collected than dispersed. A negative amount means the opposite.

Notice that the months where cash payment is made for capital expenses – the deficit is rather large. This is to be expected and will be addressed more in-depth later in the worksheet.

Balancing cash

Trial ending cash balance = Surplus(deficit) of collections over disbursements + Beginning cash balance

The Trial ending cash balance represents the change in your church’s cash balance based on the Beginning cash balance, Cash collections from revenue, and Total cash disbursements. There might be situations where this amount is considerably less than you would like it to be (particularly if it’s negative). On the other hand, there might be situations where this amount is more than you need it to be. Situations where you’re holding more cash than you would like, or is necessary.

The amount of cash you want your church to hold at the end of any given month is specified in the Desired ending cash balance field. An amount will need to be entered for every month of the planning period.

This is the amount that the Cash Budget will force balance to, based on the formulas in the worksheet. Forcing is done by increasing cash with investments, short-term financing, or long-term financing. If you don’t like how the balance was forced, then you will have the opportunity to make changes later in the worksheet that are more to your liking.

Excess (shortfall) of cash to desired balance = Trial ending cash balance – Desired ending cash balance

This amount tells you how close or far away your church is, based on the Trial ending balance, to your Desired ending cash balance.

Positive amounts will either go towards paying down debt, or it will go to an investment account. Conversely, negative amounts will either be covered with debt or will be pulled from investment accounts.

Let’s look more in-depth into financing and investments…

Short-term financing needs for your church

Short-term financing is a fancy term for money borrowed for less than one year. Typically, short-term financing is used for short-term cash flow issues.

In this example, we assume that the short-term financing is a revolving line of credit which allows the church to borrow moderate amounts of cash in order to cover the occasional cash flow shortfall.

Click to enlarge

You’ll also have the opportunity to enter the particulars about any existing short-term loans your church has outstanding. The rate and term entered for existing loans are assumed to be the same for any additional loans taken out through the remainder of the planning period.

Information entered for existing short-term loans is pretty straightforward. Simply enter the Interest rate for the borrowed funds, the Term (in months) for borrowed funds, the Original amount borrowed, and the Original date obtained.

Keep in mind, this is short-term financing. So the Term (in months) for borrowed funds should be less than or equal to twelve. Anything more than twelve months would be considered long-term financing.

If your church has no outstanding short-term loans, then enter $0 in the Original amount borrowed. Also, keep in mind that the Original date obtained for short-term financing needs to be within a year of the first month of the planning period in order to affect cash flow.

When will short-term borrowing take place?

As mentioned earlier, short-term financing is assumed to cover any shortfalls in cash not covered with long-term financing. It’s also not assumed to be covered with cash pulled out of investments.

The formula for Additional borrowings looks at the Excess (shortfall) of cash to desired balance, Repayments for existing short-term financing, Additional borrowings for long-term financing, and Repayments for long-term financing. If these amounts are less than zero, then additional short-term borrowing is needed.

If that’s the case, enough will be borrowed to cover the Excess (shortfall) of cash to desired balance. Repayments for existing short-term financing, and Repayments for long-term financing minus the amount that’s able to be pulled out of investments. In this workbook, it’s preferable to pull money out of investments rather than borrowing additional funds.

The calculation for short-term financing Repayments is too complicated to cover in detail. It’s calculated in a background worksheet. What this field looks at, is the Original amount borrowed, and any Additional borrowings from previous months. The total of the payments for all those short-term borrowings is displayed here. So, if additional short-term borrowings take place in a given month, the following months you will see an increase in negative cash flow due to the increase in payments owed

Net short-term financing = Additional borrowings + Repayments

This is the total effect on cash flow from activity in short-term financing for a given month. If more is borrowed than is repaid then this will be a positive amount. That’s because more cash came into the church than left it. If Repayments are more than Additional borrowings then this will be a negative amount. More money left the church than came in, due to short-term financing.

Whereas short-term financing covers borrowing money for less than one year, long-term financing covers borrowing money for more than one year. Long-term financing is typically used for long-term projects. For example, projects that have been approved during the capital budgeting phase of strategic planning.

In this example, we assume that long-term financing is used sparingly. It is not a revolving line of credit. Loans are repaid on an installment basis. Since loan amounts are typically big, Repayment amounts are also big.

Also, like short-term financing, you’ll have the opportunity to enter information about any existing long-term loans. The interest rate and term for the existing loans are the rate and terms presumed for any Additional borrowings entered throughout the year. This is unlikely to be exactly the case, admittedly, but for sake of this example, it is adequate.

Click to enlarge

For long-term financing currently outstanding, an Interest rate for borrowed funds, Term (in years) for borrowed funds, Original amount borrowed, and Original date of obtained must be entered.

Since this is long-term financing, ensure that the Term (in years) for borrowed funds is greater than or equal to “1.” Anything shorter than a year belongs in short-term financing.

If your church currently has no long-term loans, enter 0 in the Original amount borrowed. If the Original date obtained is further in the past than the Term (in years) for borrowed funds, then the Repayments for the existing loan will not show up in this year’s cash budget. Because… of course, the loan would already be paid off.

Additional borrowings

Additional borrowings for long-term financing are (typically) only done for long-term projects. Therefore, these amounts have to be entered manually. If capital projects are being financed with long-term debt, then you would probably want the Additional borrowings to coincide, roughly with the Cash payments for capital expenses.

Repayments for long-term financing are also calculated in the background. They reflect any existing loans outstanding at the start of the planning period. Plus, any Additional borrowings taken out during the planning period are reflected as increased Repayments in the months that follow.

Net long-term financing = Additional borrowings + Repayments

Net long-term financing is the total effect on cash flow for a given month in regards to long-term borrowings. When money is borrowed, the amount will usually be positive. As money is repaid the amount will be negative.

Using an investment (or savings) account

The investments account, for the purposes of this example, was created to help our hypothetical church always close the month near its Desired ending cash balance. Your church may or may not have a separate investment account, and that’s fine.

In theory, though, it wouldn’t hurt. Many times, on a Balance Sheet, cash and equivalents are grouped together. An investment account such as this might qualify as the “equivalent” to the cash that’s actually in the checking account. It is a place where you could invest excess cash that is relatively risk-free, and liquid (the term liquid, if you’re not familiar, means that it could easily be converted into cash).

Some examples of where you might park your church’s savings or investments are: money market accounts, CDs, short-term treasury bills, or something similar. The amount of return you’re going to earn on those investments isn’t going to be astronomical. But, you’re in the business of running a church, not a hedge fund. So, as long as the money is safe and earning a little bit of a return – that should be adequate.

Click to enlarge

The only field that needs to be entered in the investment section is the Income rate for invested funds. This is the annualized growth rate of monies that are in your investments accounts. The calculation for the balance in the investment account takes place in the background. It does take into account dividends and interest that would be earned in such an account. Income earned from investments is available for future withdrawals.

About the timing deposits and withdrawals from investments

The investments account looks first at the Excess (shortfall) of cash to desired balance. Next, it looks at short-term financing and long-term financing. Any excess cash is entered as a Deposit into the investments account. Conversely, Withdrawals from the investments account are made when the Excess (shortfall) of cash to desired balance and Repayments for both long-term and short-term financing are negative.

Since Withdrawals does not look at Additional borrowings, there might be situations where a Deposit and Withdrawal are made within the same month. A Deposit for excess money borrowed and Withdrawal to cover the Repayments.

Deposits are represented as negative amounts. This is because, technically, they come out of cash. Withdrawals are represented as positive amounts. They represent money put back into the checking account in order to achieve the Desired ending cash balance. Obviously, since the investments account is an asset for the church these negative and positive amounts don’t necessarily represent an increase or decrease in the church’s equity.

Net investments = Deposits + Withdrawals

This is the total amount that the cash balance has changed for a given month.

The ending cash balance

Ending cash balance = Trial ending cash balance + Net short-term financing + Net long-term financing + Net investments

Of course, as mentioned earlier, the Ending cash balance will be the Beginning cash balance for the following month. This is where the church forecasts its cash balance will end up at the end of the month. This amount should approximate the Desired ending cash balance.

“What is the management of cash flow?” Cash management means not only having enough cash on hand to stay solvent but also having enough cash to take advantage of opportunities as they arise.

Cash management can be done in a number of ways. First and foremost, by collecting cash from customers as fast as possible and paying suppliers/vendors as slow as possible.

Also, consider other tactics including using a revolving line of credit, incorporating subscription-based billing, and outsourcing.

Below, you’ll see some practical techniques that your small business can use to better manage cash flow.

Rather than just giving generic advice, I’ll try to give some industry-specific examples. Hopefully, this will better illustrate how these techniques can help and inspire you to do something similar in your small business.

Uncertainty doesn’t jive with cash flow. For every problem, there is a solution. Maybe not an ideal one but there is something that you can do.

Speed up cash coming in from customers

The quicker you can get cash from customers, the better. All the sales in the world don’t mean anything until that cash hits your checking account. Here are some ways to encourage customers to pay faster.

1) Alter your terms

Offering a discount to customers who pay quickly is nothing new. It’s the reason terms like “1/10, Net 30” exist in the first place.

If you’re not familiar, this means that your customer could take a 1% discount if they paid within 10 days. But, even if they elect not to, the invoice is still due in 30 days. Customers who take advantage of this discount will get you your cash up to 20 days quicker!

While a 1% (or 2%, or 3%) discount might not sound like much, it can actually add up to a lot. For instance, not taking advantage of the “1/10, Net 30” terms outlined above would cost your customer over 20% on an annualized basis! Be sure to remind them of that!

This is a particularly good option if your product or service is higher priced. Or, if it doesn’t make sense to get a cash down payment, can you ask your customer to spread the payments out over the course of delivery? These options are especially helpful if you need to expend a considerable amount of cash to get the ball rolling on the project.

Depending on your industry, this might be kind of a hard sell. But, if the amount of the cash down payment is relatively small, your customer may go for it. You’ll never know if you don’t ask. Plus, if it helps to build a better relationship between you and your customer, perhaps they’ll be more receptive.

Computer Repair LLC’s solution

Computer Repair LLC is finding that they’re not getting paid until up to 45 days after services are performed. This has caused cash flow issues in the past since their lease payment, and many other expenses, are due monthly.

In order to better manage cash flow, Computer Repair LLC first decided to start sending out invoices immediately after services are provided. In the past, they had been waiting up to 2 weeks before invoices were mailed. Since several of their customers only cut checks once or twice a month, there could be a considerable time between when services were performed and when payment was received.

They also started including the words “Due upon receipt” on their invoices. They knew full well that not all customers would pay immediately. But, it was an improvement over their old method of making the due date three weeks after the invoice date.

Also, Computer Repair LLC started offering a small discount for payment received within 10 days or less of the invoice date. This provided an incentive for their clients to pay quickly.

Finally, Computer Repair LLC began to routinely monitor the accounts receivable (AR) aging report built into their accounting software. By monitoring this daily, they were unable to keep an eye on clients that were falling behind. When this happened, they followed up immediately to discuss the situation and make arrangements when necessary.

Slow down cash going out to suppliers/vendors

For the same reason it’s good to get paid fast, it’s good to pay out cash slow. Cash that you pay out is no longer in your control – after all! You don’t want to screw anybody over, of course. But, you want to take any fair advantage you can get. Especially if you’re facing a cash crunch.

3) Cut cash expenses

An expense that is eliminated is one that you can delay forever.

Perhaps you can purchase raw materials for less from a different vendor? Or, can you hire part-time or contract employees before committing to a full-time position?

What about overhead and general and administrative expenses? Things like insurance? Can you negotiate better rates? Is there marketing that you can do that’s just as effective, but cost less? How about leases? Can you re-negotiate them, particularly if times are tough?

Finally, and this is a tough one – can you lower your own salary? Would this work if you could lower your own personal expenses?

4) Alter your supplier terms

Just as you can make changes to your customers’ terms, your vendors can make changes to your terms. That is – if they value your business.

Yes, the same principle applies as far as it being beneficial for you to take advantage of discounts. But if cash flow is truly a problem, then it might make sense for you to forgo the discount in favor of sound cash flow management.

Can you get a few more days without sacrificing any sort of discount? That would be tremendously helpful. Every day counts.

Perhaps you’ve tried this with vendors before and have been told “no.” Ask again! The more you ask the more your vendor will understand how important it is to you. Hopefully, once they understand that, they’ll begin to consider it in the name of good customer service.

John Doe’s Restaurant’s solution

Given the nature of his business, John Doe doesn’t have any real problem with cash collection. He does, however, have to deal with a decent number of suppliers. Depending on how good of a day or week he’s had, sometimes the amount he pays his suppliers can cause cash flow crunches.

In order to remedy the situation, John Doe set aside some time to really look at each of his suppliers (and their terms) closely.

In the past, as was his personal habit, John Doe paid his suppliers as soon as he received the invoice. He wanted to be a good customer. He figured that since he was so small, it would keep him in good favor with his suppliers. Also, he knew that if you paid right away, you could take advantage of early payment discounts.

However, because he was interested in improving his cash flow, he decided to do things a little differently. He decided to handle each vendor individually rather than all of them in the same manner.

John Doe discovered that while discounts are always nice, some of them weren’t beneficial enough to offset the advantage of holding on to that cash longer. In instances where that was the case, instead of paying immediately, he made arrangements to make payment as late as possible. For some of his suppliers, this was 45 to 60 days after the statement date.

He also found that some of his suppliers had, what he considered, unnecessarily strict terms. In these cases, he contacted them individually and attempted to renegotiate terms. Not all of the suppliers cooperated. But, some offered bigger discounts for quick payment. Others pushed their terms out further into the future.

Manage cash with financing

5) Get purchase order (PO) financing

If you can’t talk your customer into making a down payment, you may have to finance purchase orders in order to take their business.

Purchase order financing is basically a short term loan for the purpose of paying for products/services so that your small business can complete the sale.

This is typically a somewhat costly option. But if getting this sale is the difference between staying in business and shutting down, then it’s something to consider.

6) Get a merchant cash advance

A merchant cash advance is where your small business gets cash upfront and then you repay that loan with a small percentage of your future sales.

Rather than paying back monthly installments, as with a traditional loan, you’ll likely pay the money back with micropayments over the course of days, weeks, or months. Obviously, as with any type of financing, there will be a cost to do so.

This cash management technique is frequently used by retailers and restaurants.

This technique can be used in conjunction with raising prices because you’re going to need that extra bit of margin in order to pay back the merchant cash advance. Make sure you have a smart plan to invest that cash advance money. It’s going to be costly, so make sure whatever using the cash for has a good ROI.

7) Factoring accounts receivable (AR)

This is another topic touched on in the Understanding Current Assets & Liabilities With Examples post/workbook. Factoring is also known as selling invoices. This is a technique where someone buys your accounts receivable off of you and pays a discount for them. So, you’re obviously not going to get as much for your sales. But, it will push the cash in your pocket right now.

Again, another situation where having high margins pays off.

8) Open a revolving line of credit (LOC)

You’re probably familiar with a revolving line of credit. 2nd mortgages are often lines of credit. As are credit cards.

So, it’s the same principle, just for your business. Borrow what you need, when you need it. As you pay the bank/credit union/financial institution back, you can borrow more.

The risk with any sort of borrowing is two-fold. First, there’s the matter of interest. The cost of money. The higher this is, the more expensive the payments will likely be.

The second risk is the fixed nature of the repayment. If sales go up, those payments are easier to make. If sales go down, they don’t change. They’re still the same fixed amount. This is why I harp on spending for good ROI on this site so often.

Learn more about how financial leverage can hurt or help you by reading this post.

Car Repair, Inc’s solution

Car Repair, Inc. is a one-location auto repair shop with aspirations to expand in the future.

Like John Doe’s Restaurant, Car Repair, Inc doesn’t have any issues collecting from customers. But, the owner has noticed that he often has to hold inventory that’s really expensive for a really long time.

Obviously, some car parts are very pricey. And, since every make/model of car has its own unique parts, it’s can be costly to manage this type of inventory.

He’d also like to be able to advertise more to grow his business. If he were able to do so, he’d like to open up a new location, expand a current location, or purchase a competitor.

While he has enough cash flow to handle typical day-to-day operations, he doesn’t necessarily have enough extra to grow.

At first, he considered getting a term loan to address these issues. But, after investigating further, he found that a line of credit for his auto repair business would make more sense. A line of credit provides him with more flexibility. He only has to borrow what he needs at any given time, rather than having to apply for a new loan every time he wants to borrow more.

Plus, if he should ever find himself in a cash flow crunch because business is a little slower than usual; he has easy access to enough cash to get him by until business picks back up. The flexibility and versatility of a line of credit provide security for his business.

Big business decisions to help with cash management

Beyond the obvious cash management techniques, there are operational decisions you can make to put your small business in a better position going forward.

9) Sell idle fixed assets for cash

This is, of course only an option for assets that are sitting around taking up space. You don’t want to sell assets that are bringing in income. However, if you don’t think that they can be put to good use in the near future, consider selling them. Or, at the very least, leasing them out.

There are pros and cons to this technique. First of all, consider what it would take to buy the asset back if needed. Maybe you’ll be surprised to find it wouldn’t cost much more than what you can sell it for.

Just make sure that you don’t place your small business under further hardship for a quick influx of cash.

10) Turn down work?

This one is also a little counterintuitive. As a small business owner, you know that sales are everything. So you’re probably not in the habit of turning down business. However, depending on your line of work, and the nature of the business, maybe it makes sense to pass on some business. Particularly business that would require an enormous cash payment upfront or financing of purchase orders.

Maybe it doesn’t make sense to turn down the business completely. Perhaps it can just be postponed? If your cash flow forecast says that it would be better to do the work in a couple of weeks/months ask your client if they would be okay with that.

11) Increase prices/margins

Though this won’t necessarily bring in cash faster, there could be more of it when it finally does come in. At that time, more cash could be the difference between paying all of your expenses that are due, and only some of them.

You don’t necessarily have to increase prices across the board. You don’t necessarily have to increase them a lot.

Do you have a product/service that’s in particularly high demand? If so, can you add a couple of percentage points in margin?

Consider what’s unique about your business here. Think about the value you’re adding. When it comes time to pass along a price increase make sure you emphasize those points to your customers.

12) Switching to a subscription-based business model

As a small business owner, you know that it takes cash, time, and effort to make a sale. Probably a little less for a repeat sale. Even less for a loyal customer.

What if you only had to expend that cash, time, and effort once, and then could count on a customer’s cash to keep flowing in month after month? Doesn’t that sound better than starting from scratch after every sale?

There’s a reason that businesses are always pushing you to pay a monthly fee for unlimited products/services (or something similar). It’s because that sort of business model keeps consistent, predictable cash coming in.

Some industries lend themselves better to a subscription-based model, certainly. So, if this is something you’re interested in implementing in your small business, you might have to get creative. Look at your competitors or others in a similar industry. Are any of them offering subscription-based services? Ask yourself how you can tweak their model to make it your own.

Bookkeeper LLC’s solution

Now let’s consider Bookkeeper LLC. Bookkeeper LLC performs routine bookkeeping and some advisory services for other local small businesses.

In its early years, Bookkeeper LLC charged clients by the hour. It seemed, at the time, like a fair way to bill for the services provided. They only paid for what they needed. Most clients were fine with the arrangement.

Bookkeeper LLC noticed, however, that there could be a month or more between when services were performed and payment was received. In addition, as the owner of Bookkeeper LLC has gotten more experience, and more efficient, she’s making less money because she’s billing fewer hours. So, as time’s gone on, sales growth has been lackluster even though hourly rates have been raised.

Another problem that the owner of Bookkeeper LLC foresaw, was this – even if she was able to bring in more clients (to make up for the time she was no longer billing), ultimately there would be a point where she ran out of time. There are only so many hours in the day. As it stood, her business wasn’t scalable.

Also, like any other business that attempts to collect payment after the work is already done, Bookkeeper LLC ran into situations where collections from clients could be downright excruciating.

After struggling with these issues for some time, the owner of Bookkeeper LLC decided to pull the trigger and move to a subscription-based billing arrangement.

Some clients embraced the change.

Other clients pushed back. But, the owner of Bookkeeper LLC explained to them how the change was beneficial. What they paid for her bookkeeping services would be more predictable and easier to budget going forward. In turn, she is indirectly helping her clients to better manage their cash flow.

After switching to a subscription-based billing model, Bookkeeper LLC now, effectively, gets its money in advance rather than after services are provided. Billing and receipts are automatic. Any cash flow problems that Bookkeeper LLC had in the past are now alleviated.

Because her revenue is so predictable, she’s able to manage expenses accordingly. Collections and other accounts receivable headaches are a thing of the past. Now she can focus on working on her business rather than in it.

13) Outsourcing – spend cash to save time

Maybe you’re concerned about your small business’ cash flow situation. But, you’re being pulled in so many different directions that you can’t make time to think on the matter. If so, this may be one of those instances where you have to spend cash to save cash.

Isolate what it is that is eating up most of your attention. Is there someone better qualified to handle this (e.g. bookkeeping or marketing)? Or, is it something where you can easily document your process and hire someone from Upwork or Fiverr?

Getting these sorts of tasks off your back can not only help you focus on the health of your business, it can improve your mental health too.

Jane Doe’s Web Design’s solution

The last business we’ll consider is Jane Doe’s Web Design. Jane’s company creates websites for local small businesses.

Since Jane’s business is a “one-woman show,” so to speak, she’s responsible for every task in the business. This doesn’t leave nearly enough time to do the things she is good at it (and actually gets paid for) – creating websites. Therefore, she doesn’t bring in as much cash as she otherwise could.

When Jane finally decided that she wanted to take control of her cash flow problems, the first thing she did was something that might seem counterintuitive. She spent cash to have other people take care of those things which she wasn’t good (or efficient) at.

One of those things was marketing – specifically lead generation. Since she wouldn’t have to pay until new customers were brought in, the return on the investment was very good.

Also, since Jane isn’t a bookkeeper, she decided to pay for someone else to handle that too. The amount of time that this freed up allowed her to focus on her client’s needs and get websites done sooner. That led to getting paid sooner. It also allowed her to explore new technologies that could provide more value to her clients.

Finally, Jane decided to utilize the services of a virtual assistant. Just as with bookkeeping, doing so freed up an enormous amount of time which translated into more satisfied clients and a more satisfied by owner.

What is the management of cash flow?

Sales are the most important thing for any business. Cash flow is a close second, however. Use the template provided in the previous post to anticipate cash flow issues. Use the tactics mentioned in this post to better position your business for cash flow health.

What other tactics has your small business used to improve cash flow?

What industry-specific challenges does your small business face in terms of cash flow?

“How useful is a cash flow forecast to a small business?” Even a simple, short-term, cash flow forecast can help a small business avoid insolvency. By seeing potential cash flow issues weeks in advance, strategies can be utilized that will allow you to be proactive and help ensure your small business’s survival.

Small business cash flow planning involves calculating the effects of future inflows and outflows. Doing so will allow your small business to plan for problems. Then you can take control of them before they spiral out of control. Below, you can download an easy-to-use spreadsheet to manage your small business’s short-term cash flow.

Most small businesses aren’t “cash cows.” Even the most prudent small business owner can occasionally run into circumstances where cash is flowing out faster than it’s coming in.

Yes, you’re busy running the operations of your business. Maybe you’ve handed the reins of the accounting and finance functions to someone else. But, you’re the owner. You have to ensure that you have the cash available to fill your short-term obligations

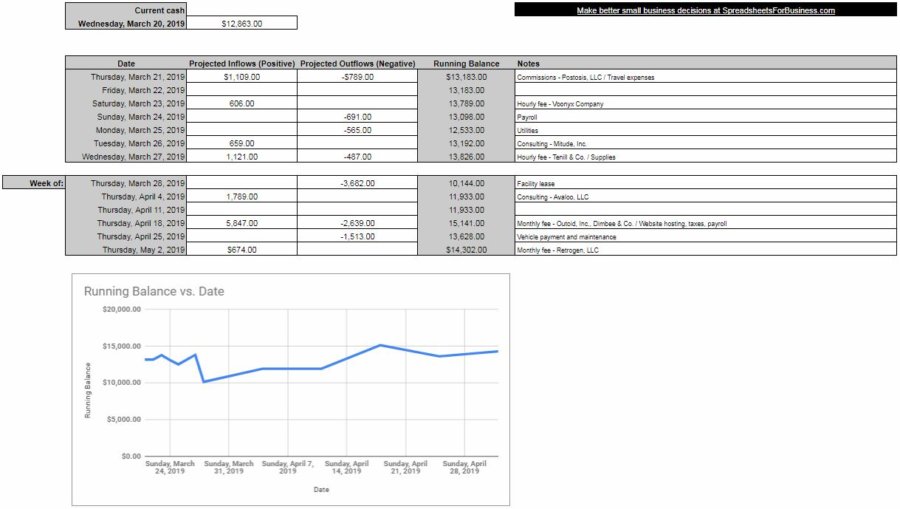

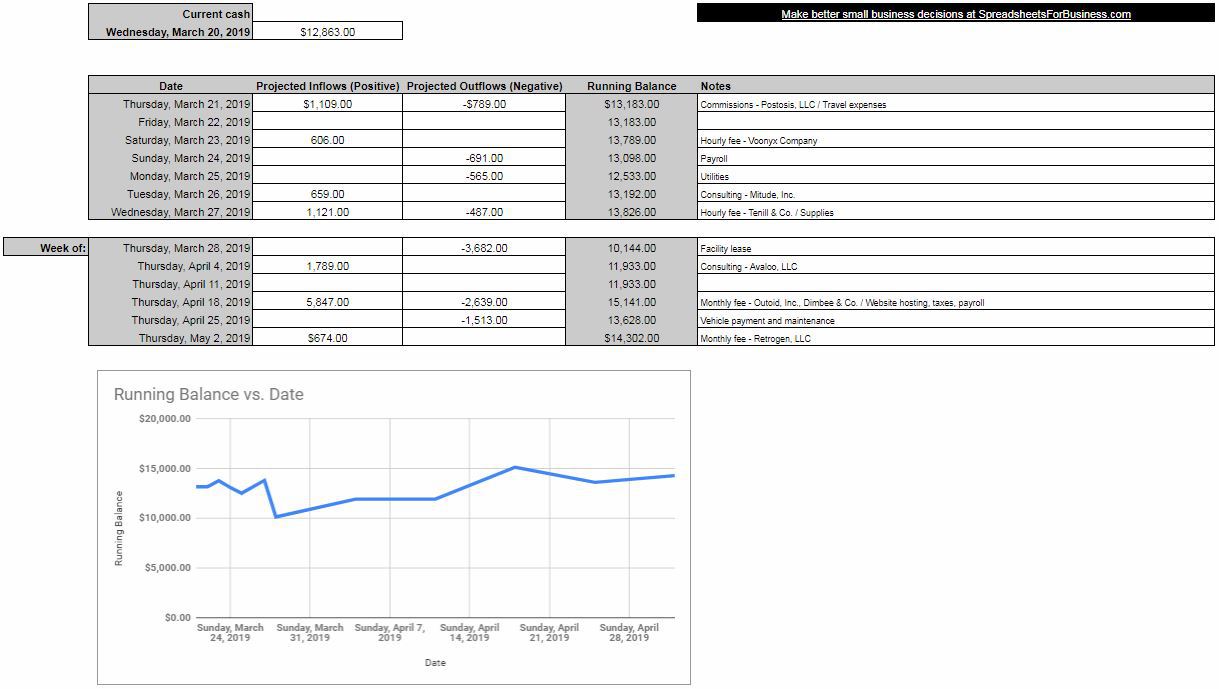

Download a simple small business cash flow template

This site is called Spreadsheets for Business, so this post wouldn’t be complete without an accompanying cash flow template.

Complete the form below and click Submit. Upon email confirmation, the workbook will open in a new tab.

This is a really simple template and it doesn’t require too much in the way of input. As with all other Spreadsheets for Business workbooks, the white cells are the ones that you fill in. The colored cells (gray in this case) have formulas and text in them.

The example data illustrates how the template works. It is for a hypothetical bookkeeping company that has revenue in the form of commissions, hourly fees, monthly fees, and consulting. It also has your typical small business expenses including things such as travel, leases, payroll, and utilities

A quick how-to on this spreadsheet

First of all, delete the example data out of the white cells. Then in cell D3, enter your business’s Current cash Balance.

Next, move down and fill in projected cash inflows and projected cash outflows for each day in the upcoming week. This is done in cells D7 through E13. Remember to enter inflows as positive, and outflows as negative. The Running Balance will update automatically.

For each inflow and/or outflow you enter, you have the option of typing a quick note to explain the transactions taking place.

After you’re done entering cash inflows and cash outflows for the coming week, move below and enter them for the upcoming six weeks. Just as above, notes can be entered to elaborate on the weekly inflows and outflows.

Finally, a simple chart is included at the bottom to illustrate the changing cash balance over the next seven weeks.

It might be that your accounting software already does something similar for you. Perhaps it’s even more robust in its analysis? However, if your accounting software doesn’t do such a thing; or if you don’t know how to use it – this simple template will give you the opportunity to think critically (even if only briefly) about this important aspect of your business.

What is small business cash flow projection?

Cash flow projection means looking into the future. Taking what you know, plus what you guess, to monitor your cash balance.

Some expenses, and possibly some sales, you know are going to flow in or out of your business in a predictable manner. You know what day it’ll happen and you know how much it’ll be.

Other cash inflows or outflows might not be as predictable. An unexpected inflow might come your way, and it’d be a very positive thing. On the other hand, you’ve almost certainly had a situation where a large unexpected outflow is necessary. That’s not quite as positive.

Cash outflows, as I’m sure you’re aware, aren’t all negative, however. Ideally, all of the cash that leaves your business is an investment, of sorts. That investment might be in an employee, it might be in inventory, it might be in an asset, or it might be in anything else that helps you create value for your customers. In other words, something that brings in bigger future inflows.

How sophisticated does cash flow forecasting need to be?

The act of projecting your business’s cash flow can be simple or complex. You can use sophisticated software; or a piece of paper and a pencil. What’s important is that you take the time to perform this important task – not necessarily how you perform it.

If you like to approach things from a simplistic standpoint, then that’s what you should do. On the other hand, if you enjoy diving into the details, then there’s really no limit to how in-depth you can go with your analysis.

When you forecast your small business’s cash flow, you can forecast no further than tomorrow; or you can forecast 10 years into the future. The closer to the present you forecast, the more likely your forecast is to be accurate.

A lot can happen in 1 year; not to mention 10 years. So, if you do decide to forecast long-term, just keep your expectations realistic. Financial budgeting is a part of strategic planning. By its nature, strategic planning is focused on long-term horizons.

That being said, there’s absolutely no reason that you can’t do extremely short term planning when it comes to cash flow. We’ll call that tactical planning. And, tactical cash flow planning could be critical to your small business’s success.

Why should your small business manage cash flow?

A lot of business problems are, of course, caused by costs exceeding revenue. Beyond that, however, it’s the timing of cash flow in and out that is the real root of the problem. Once you come up short on cash to pay your vendors/suppliers, pay your employees, or pay for your other assets, it’s easy to picture how this could start a downward spiral from which your small business can’t escape.

The best time to start managing your cash flow is when you started your business. The next best time is right now.

Just committing a little bit of time, and performing a simplistic analysis is better than nothing. However, with the tools available on SpreadsheetsForBusiness.com and from other bloggers or software providers, this seemingly frustrating task can be made manageable.

By taking ownership of the things you can control, you put yourself in a position to better handle circumstances out of your control.

Tactics for managing cash flow

Forecasting into the future, even if it’s only a few days or weeks, puts your cash flow situation into perspective. With this perspective, you should be able to better understand what you can control. You very well might not be able to change the amounts of cash outflow. But, you might be able to change their timing. For instance, can you push an expense back (even just a few days) in order to have it better coincide with a cash inflow?

Conversely, if you see that you’re going to run up against a cash flow crunch in the not-too-distant future, maybe you can make efforts to upsell current customers? Or, maybe you can make a push to find new customers? Doing these sorts of things might bring in cash flow and keep your checking account in the black.

Likewise, if you forecast cash inflow coming in the near future that you really need sooner, perhaps you can reach out to a customer and ask if they can pay a portion in advance? Maybe it even makes sense to offer a small discount if they do so in order to be able to avoid the threat of insolvency.

Cash flow crunches don’t just happen over the course of days though. They can be a long time coming. So, don’t limit your analysis to the very short-term.

I recommend that you also look out over the course of the coming year and walk through the steps of my small business financial budgeting workbook. It accomplishes the same things as mentioned above, except it allows you to take a couple of steps further back to look at an even bigger picture. The benefits are the same, however. You’ll be armed with the proper perspective in order to be proactive in addressing potential problems for your business.

Every business and industry is different. There is no one-size-fits-all advice for tweaking your cash flow. What I want to make clear though, is that willingly or unwillingly turning a blind eye to what the future holds for your cash flow puts you in a position where you can’t do anything. By simply taking the time to look at the future, you’re empowering yourself to be able to take some sort of control.

How useful is a cash flow forecast for a small business?

Remember, a more sophisticated analysis can provide you with better answers. But, the bulk of the benefit comes from simply thinking through the subject at hand and taking proactive steps to avoid problems.